Daily Updates

I first wrote about the Muddle Through Economy in 2002, and the term has more or less become a theme we have returned to from time to time. In 2007 I wrote that we would indeed get back to a Muddle Through Economy after the end of the coming recession. If you Google the term, at least for the first four pages more than half the references are to this e-letter. I get a lot of flak from both bulls and bears about being either too optimistic or too pessimistic. Being in the muddle through middle is comfortable to me.

Last week I expressed my concern that we as a country are taking actions that could indeed “Kill the Goose” of our free-market economy. I rightly got letters asking me how I could maintain Muddle Through in the face of that letter. I have given it a lot of thought and research. How likely are we to muddle through in the face of $1.5 trillion and larger deficits? Today we take another look at Muddle Through. It should be interesting.

But first, two housekeeping items. I want to welcome the 150,000 members of the National Association of the Self-Employed to this letter. They have asked me to be a special consulting economist to their group, and they will send this letter each week to their members. Since its beginning in 1981, the National Association for the Self-Employed has pioneered support for micro-businesses and the self-employed, and been a forceful advocate for small business in this country. (www.nase.org) I am honored. I am pleased to add you to my 1 million closest friends. I hope you find it useful.

Second, I will be going to South America at the end of next week, to Buenos Aires, Montevideo, Sao Paulo and Rio. I will be speaking in those cities and traveling with my new Latin American partner, Enrique Fynn of Fynn Capital (based in Uruguay). If you would like to find out about this tour or what services he can help you with, you can go to www.accreditedinvestor.ws and sign up and Enrique will get in touch with you. And as always, if you are an accredited investor, you can go to that website and one of my partners in the world will get back to you. (In this regard, I am president of and a registered representative of Millennium Wave Securities, LLC, member FINRA.) And now to the letter.

Muddle Through, R.I.P.?

I defined a Muddle Through Economy in the past as one of slow growth (in the area of 1-2%) and a slack employment environment, such as we had in 2002 and the early part of 2003. In early 2007, I suggested we would return at some point to such an environment at the end of the recession I was predicting.

I am not surprised about the response of the Fed to the current recession and credit crisis, whether it’s the large monetization of debt or the low interest rates. Assuming they more or less remove the monetary easing in a reasonable manner, there is nothing that would make me think we do not eventually recover, albeit at a very slow Muddle Through pace, with a jobless recovery that lasts for several years. It will not be pleasant, but we’ll survive.

…..read more HERE

Higher stock prices; fewer jobs…

And don’t forget the foreclosures. They’re running 23% ahead of last year…even though they weren’t as bad last month as last month.

Associated Press:

“The number of households caught up in the foreclosure crisis rose more than 5 percent from summer to fall as a federal effort to assist struggling borrowers was overwhelmed by a flood of defaults among people who lost their jobs.

“The foreclosure crisis affected nearly 938,000 properties in the July-September quarter, compared with about 890,000 in the prior three months, according to a report released Thursday by RealtyTrac Inc. That puts foreclosure-related filings on a pace to hit about 3.5 million this year, up from more than 2.3 million last year.”

What an economy!

The Dow is now back over the 10,000 mark…just where it was in March 1999 – 10 years ago. Is that progress…or what?

During that time, the dollar has lost about a quarter of its purchasing power. That means stock market investors have lost only about 25% or their money over the decade. Not too bad, huh?

And, oh yes…they’ve lost their jobs too…

AP continues:

…..read more HERE.

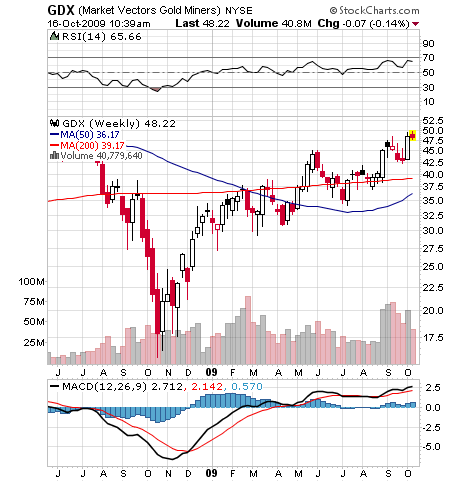

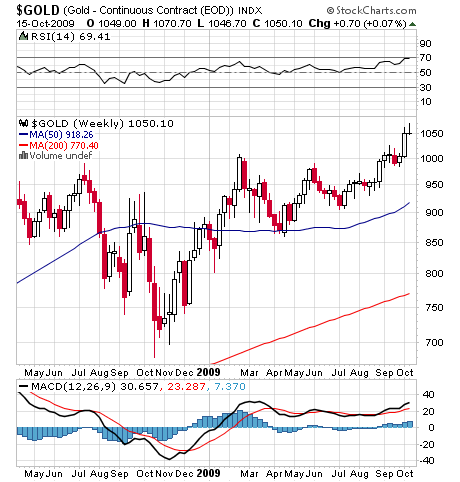

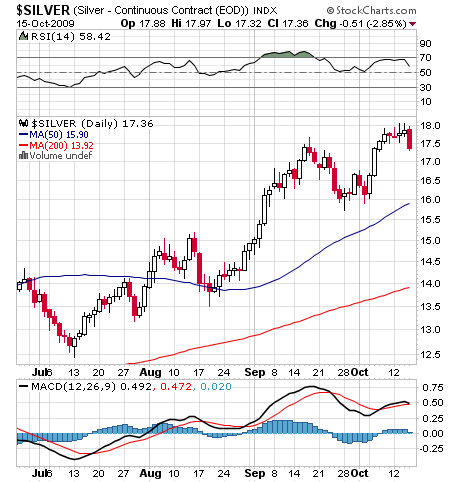

This week, the price of gold touched $1,040 per ounce while silver took a ride to now over $17 per ounce. It seems like the gold and silver run-up caught the politicians and monetary authorities by surprise. The lookouts were napping up in the crows’-nest. Then the golden alarm clock started buzzing, and it was a shock.

Lately, the politicians and monetary bubbas have all been focused on big-picture stuff, like saving the world financial system. Dressed in their superhero suits, they’ve lost sight of issues like the fundamental soundness of the dollar. They’re just too busy admiring themselves in the mirror and patting their own backs about how smart they are.

Meanwhile, a single headline set the metals markets on fire. It was about how a group of Arab nations plus Russia, China, Japan and France are plotting to replace the dollar for trading oil. Sound plausible. Will that happen? Eventually, I’ll bet, but not overnight.

$1,000 Is the New $900

The point is the dollar replacement story is a monetary rumor, and we’ve heard it a zillion times before. This week, for some reason, the rumor gained traction. Why? Well, sometimes the rubber meets the right spot on the road. It’s just “time” for something to happen. And this week, it was time for $1,000 gold to become the new $900.

It’s not hard to understand why. For many years, American politicians have overspent the resources of the nation. It was one of the few bipartisan things that national leadership could agree on. Spend, spend, spend. No issue was too small for federal intervention and funding.

The U.S. dodged the monetary bullet because a) the U.S. economy was big and resilient and it appeared like the economy could deal with the hit, b) the rest of the world didn’t have an alternative to the dollar and c) most of the world wasn’t really on to the monetary con job of the U.S. writing checks that never got cashed.

The politicians spent money like it didn’t matter. Except… it did. We’ve been approaching some sort of monetary tipping point. Now it seems like we’re there. Information flows around the world in microseconds. So there’s no big con job anymore. People across the world are tired of getting jerked around by the U.S. dollar.

Thus, now we’re watching the dollar melt down before our eyes, like the Wicked Witch at the end of The Wizard of Oz.

Off to See the Wizard

Let me digress for a moment. Author Lyman Frank Baum wrote the original book, The Wonderful Wizard of Oz. The book, published in 1900, was whimsical. But among other things, it poked fun and caricatured the gold and silver debate in the U.S. in the 1890s. More broadly, Wizard was an allegory about life and political populism in the U.S. in the 1890s.

Author Baum had a keen eye for the gold-silver debate because he knew something about the subject. Baum was wealthy, and heir to serious family money that came from the 19th-century oil fields of Pennsylvania. So he took the idea of debased currency and ran with it.

Just look at just the title, The Wonderful Wizard of… Oz, where “Oz” stands for “ounces.” I’ve heard that in the real story, the “Emerald City” of Oz was a city of gold. (It became emerald when MGM Studios made the famous Depression-era movie in 1939.) The yellow brick road was a metaphor for gold. Dorothy’s slippers were silver in the book, and changed to ruby in the movie.

The Tin Woodman stood for the urban workers of America, who were left out in the cold and rain by the forces of banker capitalism. The Scarecrow stood for the farmers — and recall that he had no brain, because many East Coast snobs thought farmers were dumb hicks, ripe for the picking. The Cowardly Lion was a dead ringer for William Jennings Bryan, who made good speeches, but could not stand up to the entrenched big guys.

The Wizard was all smoke and mirrors, reflecting the political classes as a bunch of charlatans who promised much and delivered little.

Hey, Wizard is a children’s story. It’s not a cookbook for what ails us today. If there are any real answers in the Wizard book, it’s along the lines that things aren’t what they may at first appear. And the common people — workers and farmers — are smarter and nobler than the elites think.

The only thing that’ll begin to save us is if the elites realize that they’re not as smart as they think. Of course, then they have to admit it and pursue other policies that work — like not spending so much money at the federal level. That, and create conditions to rebuild the basic economy and maintain a stable dollar.

But these are politicians we speak of so I wouldn’t count on that anytime soon. Instead of hitching your cart to political salvation, you should be counting on gold, silver and oil to pull you and your portfolio through.

Until we meet again,

Byron King

BYRON KING

Prior to joining Whiskey and Gunpowder, Byron received his Juris Doctor from the University of Pittsburgh School of Law, was a cum laude graduate of Harvard University, served on the staff of the Chief of Naval Operations and as a field historian with the Navy. Our resident energy and oil expert, Byron is the editor of Outstanding Investments and Energy and Scarcity Investor.

Sign Up FREE to Whiskey and Gunpowder HERE.

Protect Your Freedom and Your Investments — Absolutely FREE!!!

Whiskey & Gunpowder — A FREE E-letter Is Your Source for Energy, Oil, Gold, and Commodity News and Analysis

We’re in a troubling time for our economy. The U.S. dollar is having trouble staying afloat, while our financial banking system may need a complete overhaul. It seems like everywhere you look, things are getting worse.

That’s why people are looking elsewhere when it comes to their investments. Wise investors know there’s always a bull market somewhere.

Just when you thought the future of finance was really here, more traditional investments have resurfaced as the most profitable plays you can make. Investments in commodities like gold, oil, silver, wheat and other grains, and natural energy sources have become life jackets for many distressed investors.

That’s where we come in to help. At Whiskey & Gunpowder , we’ll give you up-to-date commodity news and analysis from some of the leading names in the field. Whiskey & Gunpowder , a free e-letter, gives you this insight in a straightforward and informative way five days a week. And we’ll even attempt to entertain you in the process.

Get Whiskey & Gunpowder delivered to your inbox daily… sign up for a free subscription today!

A brief excerpt of the lengthy daily internet comment by Richard Russell of Dow theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

Saturday Oct. 17th

Since 2002, the Dollar Index has been down 38%. That means that you’re losing purchasing power by holding your Treasury bonds. What good is 4% a year (or 16% over seven years) if you’ve lost 38% of your purchasing power during the same time period? So as the dollar heads down, you sell your bonds. Which is what is happening now in many quarters.

The chart below traces the tragic path of the US dollar since 2008 (courtesy of the Chart Store).

Friday Oct. 16th

“Two things are infinite — space and human stupidity.” – Albert Einstein

I’m one of those weird birds who watches the count of consecutive months of advances or declines. I do it for overbought or oversold purposes. For instance, on the bear leg down from the Dow 2007 high to the Dow 2009 low, the count was down an incredible 14 out of 16 months. That series rendered the Dow severely oversold. Then we got the V bottom, as seen on the monthly chart below. In all the years I’ve been studying markets, I’ve never seen a bear market end in a V bottom. Compression on the downside leads to compression on the upside. Following the March 2009 low, the Dow advanced seven out of eight months to October, which is where we are now.

Below, a monthly chart of the Dow, which illustrates what I’ve written above.

Gold bull market. Gold has closed higher for nine consecutive years. And yet, the great majority of investors continue either to ignore or be sceptical of gold. (Ed Note – Richard has been buying gold since it was below $300 in the late 1990’s and still continues to buy Gold and Gold related items such as Gold Share ETF’s)

Despite a host of concerns (weak economy, high unemployment, mounting foreclosures, geopolitical issues, etc.), the Dow made another post-crash high today. While the recent string of new rally highs is significant (especially coming on the heels of a major stock market plunge), it should be noted that the Dow is currently testing resistance (see red line).

Chart above by ChartoftheDay.com. Click HERE for FREE Subscription

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold.

There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974. He loaded up on bonds in the early 80’s when US Treasuries where yielding 18%.

· The Obama administration said on Thursday that it had “serious concerns” about the value of the renminbi, but stopped short of accusing China of manipulating its currency in a closely watched report to Congress. (FT)

· Key Reports today:

Treasury International Capital Data (or are they still buying the Treasuries)

Quotable

![]() Horatio:

Horatio:

He waxes desperate with imagination.

Marcellus:

Let’s follow. ‘Tis not fit thus to obey him.

Horatio:

Have after. To what issue will this come?

Marcellus:

Something is rotten in the state of Denmark.

Horatio:

Heaven will direct it.

Marcellus:

Nay, let’s follow him. [Exeunt.]

![]() FX Trading – Weak dollar good or bad…depends on your time frame I guess

FX Trading – Weak dollar good or bad…depends on your time frame I guess

Richard Berner is an economist from Morgan Stanley—I think he is very good. He made these comments in a research note recently regarding the US dollar [our emphasis]:

“The dollar’s recent slide is only reversing a substantial rise that began in mid-2008; on a broad, trade-weighted basis the dollar is actually 8% stronger than it was at that time and now stands about where it was two years ago. Moreover, the depreciation has been orderly and has been accompanied by falling, not rising, risk premiums. And one key driver – the US current account deficit, which is a measure of US external financing needs – has shrunk to less than 3% of GDP, or half its peak value.

“Disinflationary forces dominate inflation for now. There is broad agreement that a weaker dollar can contribute to higher inflation, both through its direct influence on import and commodity prices and via its indirect impact on inflation expectations. The interplay among them is important: While a weaker dollar and rising commodity prices will primarily change relative prices, like those of imports and energy goods and services, they can nonetheless influence both inflation expectations and inflation itself.

“In our view, a weaker dollar and rising commodity prices are tangible evidence of the Fed’s reflationary thrust. Since the Fed stepped up its quantitative easing at the March 18 FOMC meeting, the dollar has declined on a broad, trade-weighted basis by 8.7%, crude oil quotes have jumped by 46%, and broad commodity price indexes have risen by 18-26%. To be sure, the dollar’s recent decline reflects greatly reduced risk-aversion, and rising commodity prices also are a sign of investors’ increased appetite for risk amid hopes for global recovery. But they are all part of the policy transmission process. Although exchange rate ‘pass-through’ has weakened in recent years, it isn’t zero. A weaker dollar will help to limit inflation downside through import prices, commodity prices and inflation expectations.”

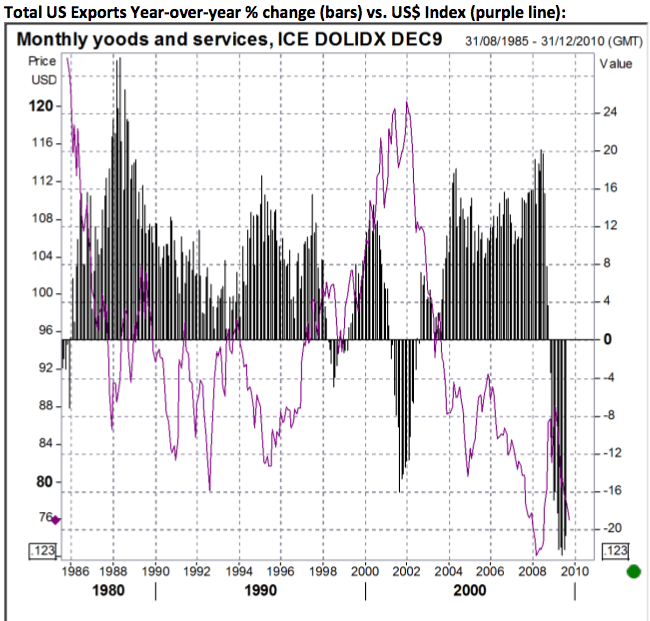

Mr. Berner is of the view that a weak dollar does significantly help US exports, with an admitted lag. We don’t deny there is benefit on the export front from a weakening dollar…as the chart tends to support that view….

Total US Exports Year-over-year % change (bars) vs. US$ Index (purple line):

There will be cyclical bounces higher along the way for the dollar, as the US economic growth relative to its competitors recovers and US interest rates rise. But we are concerned until there is a major policy shift, which has capital formation at its core, the dollar will continue to fade as the US dollar index continues the long-term pattern of lower highs and lower lows despite any cyclical rebound in exports thanks to lower US goods prices.

Today, the dollar is bouncing higher against the pack. Have the fundamentals changed? Not really. Three factors we see in play at the moment:

1) Negative dollar sentiment extreme and technically extended

2) Concern of correction in the stock market, which may lead to a strong dollar bounce if correlations hold

3) Though minor, a bit of fear the Fed may put some risk back into the one-way dollar bet

Three guesses indeed. But why we decided to take some profit on our short USD-Norwegian Krone position yesterday, and add long USDJPY long (JY futures short).

Stay tuned.

Jack Crooks

Black Swan Capital

Triffin’s Dilemma and why the dollar is in long-term trouble?

David here …

Jack and JR are putting the finishing touches on our monthly Currency ETF Investor newsletter, which will be sent to our subscribers today. And I think this month’s topic is interesting and timely, given the concern we all have about the potential for long-term decline in the US dollar and loss of the dollar’s world reserve currency status.

If this is an area of interest to you too, and you’d like to see our latest recommendations to take best advantage of the dollar trend with the ease of exchange traded fund investing, I urge you to subscribe to our Currency ETF Investor HERE.

For $39 per year I doubt you will find a better bargain for you potential return anywhere else.

Remember, your subscription comes with a 30-day risk-free money back guarantee, no questions asked, if you determine it’s not the right fit for you.

Thanks for reading,

David Newman

Black Swan Capital LLC

P.S. If you might be interesting in our more aggressive forex and currency futures trading service, please send me an email at info@blackswantrading.com for information, or you can subscribe at our website. Jack and JR are finding some excellent trade setups lately.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair