Daily Updates

“Right how we are seeing a major catch up going for undervalued asset based companies in the precious metals space. This part of the up tick could surprise even rabid bulls. Some more speculative companies that had been strong gainers appear to be flagging because of this, but that won’t be permanent. Speculative gains should be moved to companies with more solid outlines, but as the asset based companies get closer to full price funds will flow back to specs.”

Gold’s New Friends

Press rumors of planning meetings to shift crude pricing away from the US$, plus a 0.25% increase in Australia’s bank rate, has put some serious bounce in gold and silver prices. The yellow metal has convincingly moved past its old high, in US$ terms, and we expect that move to continue. Whether the details of the meetings reported in London’s The Independent are accurate in every detail or not, markets have had no problem accepting the basic point that the greenback cannot expect long term support as the globe’s reserve currency.

Commodity prices, especially gold and silver, are very much currency stories. The US Dollar continues to lose face for a variety of reasons, with more rapid growth in the creditor and resource producing nations being the latest. This, not inflation concerns, has been our focus. Australia’s increase in its bank rate may be duplicated in a number of other economies before Washington gets around to it. This would continue the downtrend in the Dollar and uptrend in precious metals no matter what inflation looks like.

Lack of high yield alternatives, plenty of frustrated money on the sidelines and the potential for “good” earnings (at least by comparison with the past 12 months) may drive the major bourses higher yet. This will add more strength to the already outperforming metals sector.

The biggest potential short term risk is that Dollar Distaste reaches the bond market and drives yields higher. That could turn the Dollar and the stock markets around quickly. Be happy, but keep an eye on those Treasury yields.

Copper stocks continue to pile up while the red metal sustains price against US$ weakness. Over half the stockpile taken down earlier in the year has now come back into the market. Some of the stock on offer would likely disappear on a price decline, or if the current Dollar weakness turns into a rout. But that has to happen before we are comfortable with this year’s price gains. The message since mid July has clearly that users think the price move has been “too far—too fast”.

That remains the case for most commodities. Traders are playing musical chairs to a tune of weak Dollar fundamentals against a melody of uncertainty for demand sustainability. Notwithstanding our belief that the greenback’s decline is a longer term phenomenon, we don’t look for anything to trade in one direction permanently and this move will be to a new trading level. We doubt the guy in the last chair of this round will celebrate for very long before shifting direction with the herd.

We should note again the continuing calls by the government for closure of Chinese smelters. This is due to both inefficiency and overcapacity. Current stockpiles aside, excess smelting capacity is not the same as excess metal producing capacity. The two roughly equate for some metals, such as aluminum for which there is a ready supply of input minerals in coastal regions that could use development funding.

Foundry capacity, or overcapacity, will not govern iron ore supply for the time being. Most prospective ore regions need infrastructure to coastal shipping ahead of any expansion. Longer term iron ore supply will come from regions that put that infrastructure, and longer term contracts, in place. We do still see opportunity in iron ore, partially because of the politics that surrounds it.

Medium and longer term copper capacity will be governed by mine supply, and the long time frames for large copper mines to come on stream. Smelters can’t process concentrates unless mine supply is sustained. The same holds for zinc and to a lesser extent nickel. We don’t view China’s push to reduce smelting capacity as a sign the metals bull has run out of steam. It simply makes sense for China to shut in costly, polluting smelters when there is capacity next door in more efficient Korea and Japan.

Japan’s new government has referenced abandoning the weak Yen policies of its predecessor several times now. Given it is supposed to be part of the talks cited by The Independent and that the Yen (along with gold and the Yuan) are supposed to be part of a new “basket” for oil settlement, that stance is making more sense.

More importantly, Japan’s new leadership has stated it favors stimulating domestic spending in order to end a deflationary malaise the country has lived with for most of the past two decades. Cheaper inputs for its resource poor citizens are therefore more important to it than cheapening the exports market of its high end producers by devaluing its currency.

These pronouncements have aided the cause of price support for Dollar denominated global goods. But, markets are and will continue to have a tough time with deflation’s poster child righting itself in the current environment. That is entirely reasonable given deflation’s shadow slowly creeps over the western landscape. However, PM Hatoyama is quite deliberately shifting sentiment away from a western focus of the past half century.

At worst this is pragmatic recognition that the customer base for Japan’s goods has ended its buying spree. The real message is that Japan is wealthy and able to chart its own course, once it has detoxified its bureaucracy from spinning funds into their retirement companies. There will be no quick fix from this policy shift, but it makes more sense than a failed policy requiring western sales points for its goods.

We can’t overstate the potential importance of these moves in Japan. This is the second largest economy on the planet in nominal terms, and yet one for which concern that a lack of raw materials supply could hamper its growth spurt is very much a living memory. It has also seen a massive growth in ore processing to meet this concern overtaken in large measure by neighboring South Korea. We believe a shift is building in Japan to a much greater emphasis on its domestic economy, and equally to more focus on its regional economy. That should mark a major shift in the geography of country risk, and a greater acceptance that “Asia rising” is the global boon we perceive it to be.

So, how does that impact the current gold boom? It should simply give it a greater head of steam. Missing from the weakening Dollar equation was how the other side of that equation shapes up. Much of Europe was happy to jump on the cheap debt = housing boom bandwagon, and so is in no better shape than the US. So the Euro can sustain only so much upward pressure. Currencies in the less weakened industrialized “west” — AUS, CDN, NZ— simply don’t have the scale for the job. There has been only one sensible answer.

We have said in the past that the only equation that made sense was Yen strength as a proxy for Asian growth economies. Most wrote off the notion because of Japan’s export model. Now that Japan has a government that is willing to play that card, the pieces are truly in place for quick shifts in the FX market. Gold and silver will benefit smartly from that, and no the world is going to end as part of the process.

Right how we are seeing a major catch up going for undervalued asset based companies in the precious metals space. This part of the up tick could surprise even rabid bulls. Some more speculative companies that had been strong gainers appear to be flagging because of this, but that won’t be permanent. Speculative gains should be moved to companies with more solid outlines, but as the asset based companies get closer to full price funds will flow back to specs.

If you are a trader, the shift from one play to the next could get dizzying. If you aren’t, then view this as a “stay the course” moment for precious metals. Expect some significant pull backs as traders take gains, but these will be in the context of a rising market for some while yet.

David Coffin and Eric Coffin

*****

David Coffin and Eric Coffin produce the Hard Rock Analyst publications, newsletters that focus on metals explorers, developers and producers as well as metals and equity markets in general. If you would like to be learn more about HRA publications, please visit us HERE to view our track record, see sample publications and other articles of interest. You can also add yourself to the HRA FREE MAILING LIST to get notifications about articles like this and other free analyses and reports.

The HRA – Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-base expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

Before the Oil Derrick

Did you know that workers were extracting oil out of the ground before the oil derrick made its first appearance?

But it was a small industry made up of small companies and serving a small market. What changed it?

Technology. Before an enterprising oil worker saw derricks operating in a salt flat and thought that just maybe it could work for oil, digging for oil was a long and difficult endeavor. Up until that point oil was used to light lamps plus some other small uses.

The oil was always there in the ground. The industry was held back from growing beyond those modest applications because oilmen could only tap into a small percentage of the underground oil.

The introduction of derricks into the oil industry changed everything. It allowed the oil industry to grow into a major business. In fact, the growth of modern industry and the growth of oil went hand in hand.

Still About Change

The oil industry has gone back to its roots. For the first time in about 100 years, it’s seeing limits on its growth for the very same reason as a century ago. Oilmen can only tap into a limited portion of the oil in the ground.

That’s about to change. Once again technology is about to spark another oil boom.

How would you like to be an oil baron? When derricks first came on the oil scene, nobody believed in them. Derricks were just a lucky thing the oil industry stumbled on. They were too good to be true. An accident.

Don’t be one of those disbelievers. Technology transformed the industry once. And it’s about to do it again.

Left-Over Oil

Oil companies typically abandon their fields with a lot of oil left in the ground…around 60% it’s estimated. Why so much?

In most oil reservoirs, the oil resides in porous rock that are tens of meters thick but stretch for miles. A conventional oil well is a vertical shaft. It’s in contact with only a narrow cross section of the reservoir. Such a well depends on oil percolating through microscopic pores over long distances. A lot of the oil is stranded inside the irregular geometry of the oil field.

Fire in the Hole

Water flooding and carbon dioxide injection can force some of this trapped oil out. But IDE’s Dr. Rusty McDougal has found a technology which does much better than water flooding. It actually creates a controlled fire down the oil hole. The fire produces steam and heat, creating a wall of unbelievable pressure which drives the remaining oil out of the hole.

This could change the whole calculus of oil field development and production. Schlumberger, for example, has recently been making most of its money from improving existing wells (instead of developing wells), such as fracturing rock underground to improve oil production. Dynamite is last century’s technology. Forcing water and steam down a hole is also 20-year old technology.

Oil companies are also beginning to use “smart wells” with sophisticated sensors that can detect, for example, when water (instead of oil) is being pulled into the well. But the upfront costs are high and sensors only provide more information. They don’t directly increase oil production.

The company’s “controlled fire” technology promises to enhance oil recovery at a time when the oil majors are having trouble increasing their output. The need for this technology has never been greater than it is right now.

Rusty says the technology is perfectly safe… “The process is established sufficiently to pose no safety issues (it is being done in California, no less). The fire continually burns and more and more oxygen is injected for continued production. You put out the fire by ceasing to inject oxygen.”

Some estimates say that this technology can double or triple the output of a field and extend the life of a field for several more years. This technology is clearly a game changer.

Rusty recommends the company offering this technology in his last issue of The Resource Speculator. He also says that this recommendation “has moonshot written all over it.” If you want more information on Rusty’s resource picks, click here.

Keeping Your Eyes on the Road

Imagine getting on the highway as you drive to work and traffic is brutal. But as you weave in and out of traffic, your attention is drawn to the big 18-wheeler which is trailing you. You keep looking behind you to see where it is, what it’s doing, if it’s getting closer. In fact, you spend more time looking out your rear window than you do looking ahead. The inevitable then happens. You hit the car that had just cut in front of you. You curse. You should’ve seen it coming, but you took your eyes off the road.

The most common mistake investors make? Taking their eyes off the road. Investors are the most distracted group of people I know. They’re constantly looking backwards, trying to figure out why the market acted the way it did yesterday or last month or last year. But to drive your investments to their most profitable gains, you should be looking ahead and not backwards.

Case in point: Instead of trying to figure out how we got into our current crisis, you should be trying to figure out how we’re getting out. On the highway to profits, it’s not what exit you got on but what exit you’re getting off which matters. For example, if you think that housing will lead us out, then you should consider getting into housing assets, like REITs, early.

But housing isn’t leading us out. The banks aren’t leading us out. High-tech isn’t leading us out. And energy isn’t leading us out.

Brave New World

What was successful in the past won’t be successful in the future. In today’s investment world you have to clear your head of the belief system that drove your investments during the past two decades. It’s a different world with different opportunities and different risks.

If you have trouble understanding that, just think of Florida, one of our rich states where the housing bubble blew the hottest. Housing prices are expected to fall further by 27% in Orlando and 26.8% in Naples by June 2010. You really think Florida will be one of the first states in America to get healthy?

Wells Fargo’s commercial loan group doesn’t. They just hired five more guys and still can’t keep up with the volume of defaults. One of the worst hit areas? “Southeast Florida and Tampa are serious trouble spots,” they say.

Now imagine poor and scrappy Alaska. It doesn’t exactly conjure up images of suntanned 30-somethings driving around Lamborghinis, does it? But Alaska’s oil revenues are keeping the state from racking up debt. And its Alaska Production Tax passed in 2007 is squeezing even more money from oil producers.

In contrast to Florida, housing prices are expected to rise 2.5% in Fairbanks and 2.1% in Anchorage by the middle of next year.

I’d much rather buy Alaskan than Floridian bonds these days.

IDE’s Steve McDonald has been talking about this new brave world of investing for years now. His investments cover the gamut of stocks, bonds, covered calls, and global opportunities. If you want to invest safely and opportunistically, check out Steve’s Sound Profits right here.

Invest Safely,

Bob Irish

Investment Director

Investor’s Daily Edge

Sign up for the FREE INVESTMENT NEWSLETTER (Ed Note: top right)

Investor’s Daily Edge is a free investment newsletter that’s delivered by email before the market opens. In each weekday issue you’ll receive clear recommendations and practical strategies for protecting your portfolio and multiplying your money – whether the market is rising or falling.

This is not a “news” publication, so don’t count on a recap of the biggest stories of the week. Instead, you’ll get a to-the-point analysis of what “the news” means to you – and how you should act TODAY to make the most money with the least risk.

Investor’s Daily Edge is written by a select group of market experts, each with their own style of investing. So whether you are a long-term investor, a short term trader, or a prudent speculator, you can count on useful advice you can take to the bank.

The market is constantly changing… that’s why you need an edge. And that is precisely what you’ll get with Investor’s Daily Edge.

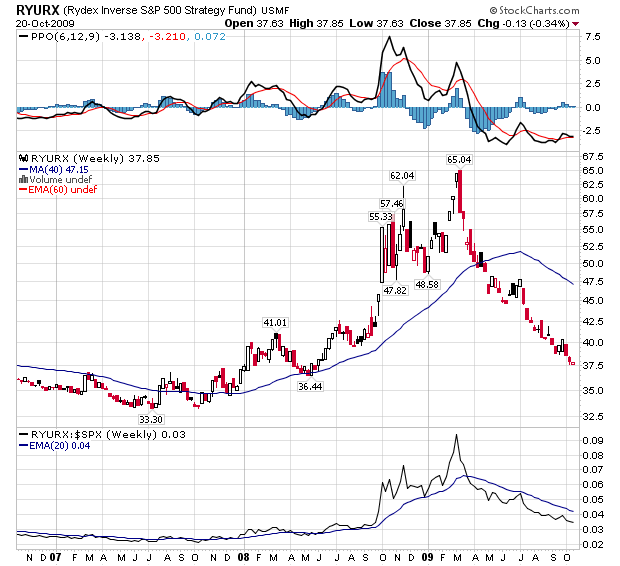

The stock market has had a spectacular short-term run, based on unjustified optimism. Most commentators are claiming the economy is beginning to recover. The stock market has been reflecting their optimism for several months. As the optimism has finally begun to be tinged with pessimism, the stock market has topped out.

You can now bet against the stock market. I don’t usually make “short-term” calls like this, but the stock market has made such a big, unsustainable rally, it will cave in big time.

If you carefully read the history of the Great Depression of the ‘30s, you will see that at least twice during the Depression the stock market had a rally equal to the one we just had in the last few months. If you are a short-term trader, which I am not, you could probably make a lot of money. But those rallies were transitory, and the Depression wasn’t over until WWII brought us out of it.

Buy Rydex Inverse S&P 500 Strategy (RYURX). It’s cheap right now because of the rallying stock market and Rydex Inverse goes the opposite direction of the stock market. How much should you buy? At least as much Rydex Inverse as you have in stocks or other mutual funds, if only to offset the losses you will take in your portfolio over the next little while.

If you really want to profit big time, cut way back on your stock-market holdings and increase your Rydex Inverse holdings. There are two ways to bet against the stock market: 1) sell stocks; and 2) use Rydex Inverse Strategy as a contrarian bet.

Gold and Silver

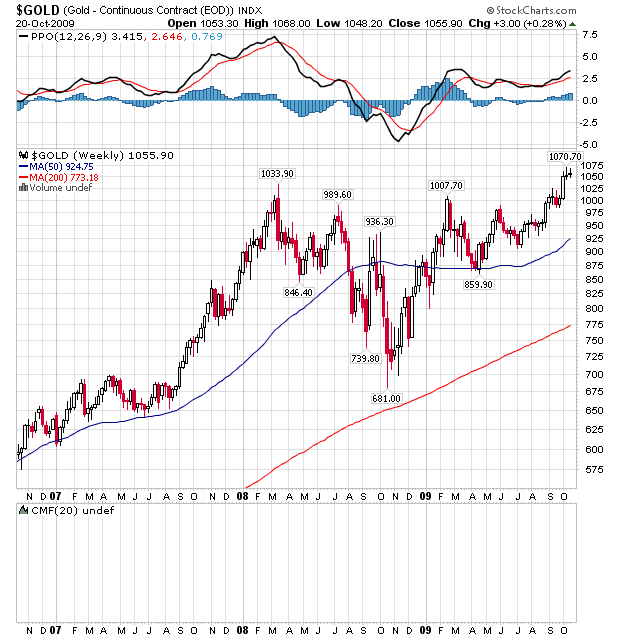

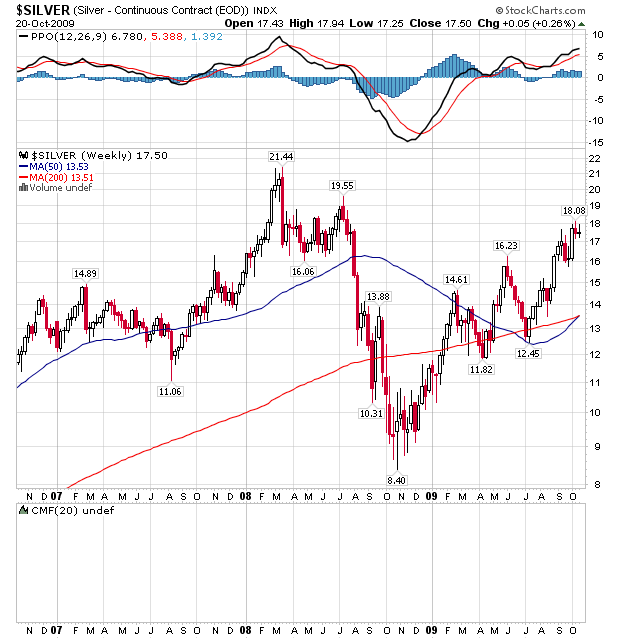

Gold and silver have been rallying, and gold seems to want to hold above 1,000 and silver above $17. They have performed at least as well as the stock market, even during this rally. Increase your bullion holdings.

Jim Raby, my stock broker, believes the bankers will try to hold gold below 1,000, and he makes a pretty good case for it. However, it doesn’t seem to be working that way, so I would increase my bet on the metals, especially silver, because a big new player has entered the game – China.

China is now a big buyer of gold and silver for their banks. Chinese TV has been recommending that everyone should go to the bank to buy gold and silver. That’s 1.3 billion people getting propagandized. This is a major bullish factor for gold. Perhaps the bankers have met their match.

Increase your holdings of gold and silver bullion or coins. Take a whirl at the mining stocks as outlined in The Ruff Times.

TIPS

TIPS are inflation-adjusted bonds, and would seem to be useful in my Investment Menu. But there is a downside.

I will write about this in the next Ruff times, after I’ve completed my homework. Although there are profits to be made, be cautious. They won’t be as dependable against inflation as gold and silver coins and bullion. More later!

My New Book is About a Month Away

My new book How to Prosper in the Age of Obamanomics is in the final stages. We will accept a printer’s bid this week. We will feature it in our revised website as a free gift for new subscribers.

If this book is widely distributed, it will put a target on my back. I have learned the hard way that Presidents will retaliate when under attack, and this book certainly attacks Obama.

With any new subscription (www.rufftimes.com) you will get a free copy (delivered as soon we get it from the printer). Why did I write a new book? It was written to prepare new subscribers to understand the basics of Ruffonomics so that when they read The Ruff Times it is not like coming into the middle of a movie.

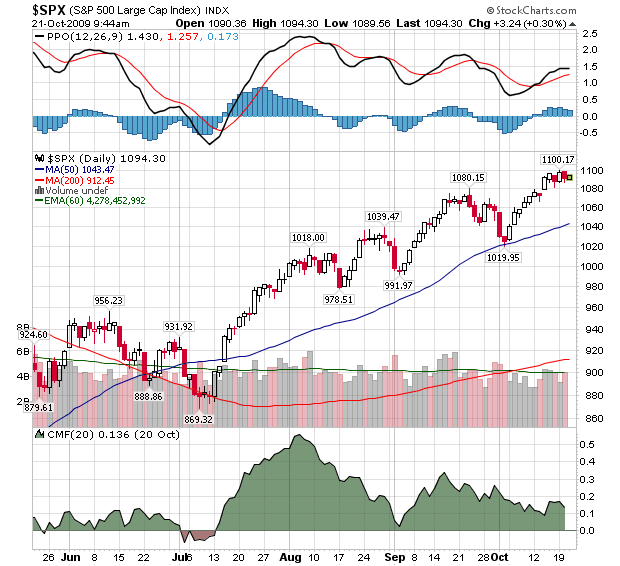

MarketRemains In A Topping Pattern

Michael Campbell will be hosting and I will be presenting at the ‘All-Star Trading Super Summit’ on Saturday, October 24, at the Sheraton Wall Centre in Vancouver, British Columbia. Below is his formal invitation. Vancouver is always fun and I get all the salmon I can eat. Hope to see you there. Sign up today!

http://www.vrtrader.com/files/MichaelCampbellinvitation-Oct09.pdf MarketRemains In A Topping Pattern – Looking To Buy? – Wait!

STOCKS

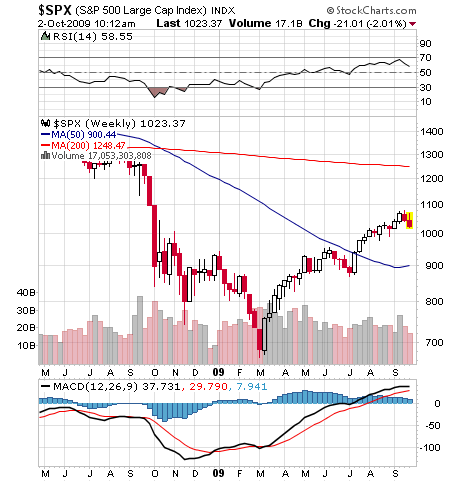

It was another ‘Turnaround Tuesday’ and Monday’s optimism turnend into a Tuesday correction – all despite the antics and fireworks of Apple Computer. Indexes, with the exception of Nasdaq due to Apple, held Monday’s highs on Tuesday.

Though the intermediate trend (into mid 2010) is likely higher (Dow 11,300 or greater?), short-term it is my opinion that time has run out on this rally. Next week hosts potential end of the month ‘window dressing’ which should be bullish for the market, so if we see further weakness over the next three or four trading sessions it might be wise to lighten up on short positions or reverse ETF positions.

We certainly did not see a ‘Turkey Melt-Up’ yesterday – the headline of my morning commentary. As I’ve been reporting for quite some time, a 50% retracement of the bear market decline translates into 1120-1130 in the S&P 500 and we barely saw 1100 while the equivalent in the Dow Industrials is 10,300 and we traded only at 10,098. So, I suppose there is more ‘room’ to the upside should the PPT decide to charge ahead to the upside next week. At this juncture I am not inclined to be playing the long side in any extensive manner, except for very short-term trading intra-day or perhaps overnight.

I am on a TIMER DIGEST ‘Sell’ signal looking to capitalize on a retracement with a view to reverse back to a ‘Buy’ signal sometime.

The earnings bulls got solid earnings reports from Apple (+4.69%), Caterpillar (+3.04%), Texas Instruments (+0.60%), and Pfizer (-0.28%), but were unable to get a rally going as so-so economic data trumped their aspirations. For the session the Dow was off 50.71 to 1041.48, the S&P 500 was off 6.85 to 1091.06, and the Nasdaq Composite was off 12.85 to 2163.47. Volume increased over Monday and breadth was weak.

The government reported that housing starts have been flat for four straight months. (See the Economic News section below) The tide seems to be turning with regard to housing data as the euphoric rallies that were generated by the slightest bit of positive or even less negative news are now being replaced with the somber reality that any announced real estate recoveries were probably nothing more than wishful thinking.

Once again, however, a weak start was met with a steady inflow of buyers to push the indices well off of their lows. The ‘buy the dips’ crowd is still at work, but their resolve is being tested more and more these days. Even with so many companies beating artfully lowered expectations, this market is having a tough time rallying.

Apple’s strength did help the Nasdaq 100 to a loss of only 0.03%. Another bright spot was the performance of the Dow Transports, which gained 0.18%.

Technology stocks performed relatively well (XLK -0.33%) thanks to the good earnings reports from Apple and Texas Instruments. On the other hand, Energy (XLE) fell 0.64% and Materials (XLB) dropped 1.05% as commodity prices fell on a bounce in the Dollar and concerns over economic growth and demand for natural resources.

Homebuilders (XHB -2.26%) and real estate (IYR -1.86%) bore the brunt of the selling. Market Vectors Gold Miners (GDX -2.12%) also saw traders head for the exits as the dollar firmed.

The market certainly looks like it is topping again and another test of the 50 day moving average (currently at 1041 on the S&P) could occur in the next few weeks. Three weeks ago, the 50 day moving average provided the market with strong support and a launching pad for another rally.

AFTER HOURS NEWS:

SanDisk swung to a third-quarter profit as revenue surged from the year-ago period. The Milpitas, Calif.-based company earned $231.3 million, or 99 cents a share. Last year, it lost $165.9 million, or 74 cents a share. Adjusted net income, which excludes one-time charges, was 75 cents a share for the most recent period. Revenue rose 14% to $935.2 million. Analysts were looking for earnings of 26 cents a share on revenue of $790.9 million. SNDK rose 9.6% in after hours trading.

Yahoo said cost cuts helped its third-quarter net income more than triple to $187 million, or 13 cents a share, from $54.3 million, or 4 cents a share, in the same period last year. Earnings on an adjusted basis were 15 cents a share. Net revenue came in at $1.13 billion. Analysts expected earnings of 7 cents a share on $1.12 billion in net revenue. Yahoo also forecast fourth-quarter revenue of $1.6 billion to $1.7 billion. The company’s performance during the third quarter indicates that its “major businesses have stabilized,” Yahoo Chief Executive Carol Bartz said in a statement. YHOO gained 5.2% after the market closed.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

During the past six weeks gold has broken above two very important resistance lines thus giving clear buy signals. And I presented several more arguments calling for much higher gold prices in my Money and Markets columns of September 9 and October 14.

But Now Another Important Market

Has Given a Clear Buying Signal …

As you can see on the following chart, crude oil prices have been hovering between $60 and $75 for roughly four months. At the same time the Price Momentum Oscillator (PMO), which signals the strength of a price trend, has corrected its overbought readings by coming back down to the zero line.

While the price of oil was going sideways, this momentum indicator was creating an interesting bottoming formation.

Then, last week, an important event occurred: The price of oil broke above its upper boundary, and the PMO finished its consolidation. Both lines on the chart, price and momentum, were thus giving key buying signals.

My analysis tells me that the next price target stemming from this four-month consolidation formation is approximately $100 per barrel.

That’s not particularly good news for you or me as consumers. After all, we’ll have to pay more to fill up our gas tanks, heat our homes, and more.

So it’s difficult for me to understand how some pundits can claim that rising oil prices might be a good thing for the economy …

The way I see it, higher prices are like an additional tax for American and European consumers and businesses alike. They’ll dampen the still-nascent economic recovery before it gets real traction.

What’s more, rising oil prices are in step with the message coming from gold’s price advance. Here’s why I say that …

Rising Prices Are Caused By

Governments’ Policies …

Rising gold and oil prices are symptoms of the inflationary monetary and fiscal policies that have been implemented. These were without doubt global governments’ absurd and counterproductive answers to the popped real estate bubble.

My basis for this conclusion is very straightforward: If governments continue printing boatloads of money, the prices for goods and services have to rise sooner or later. There’s no way they won’t!

And whether it happens sooner or later depends on certain circumstances, such as changes in the velocity of money or money demand.

The breakouts in gold and crude oil are like early warning indicators. And the commodity markets are clearly telling us that inflation will rise sooner rather than later and will become a major problem for the world economy.

Fortunately as investors, we can turn that problem into a tremendous opportunity. And my colleagues and I will continue to show you how to do that every chance we get.

Best wishes,

Claus

Claus Vogt is the editor of Sicheres Geld, the first and largest-circulation contrarian investment letter in Europe. Although the publication is based on Martin Weiss’ Safe Money, Mr. Vogt has provided new, independent insights and amazingly accurate forecasts that, in turn, have contributed great value to Safe Money itself.

Mr. Vogt is the co-author of the German bestseller, Das Greenspan Dossier, where he predicted, well ahead of time, the sequence of events that have unfolded since, including the U.S. housing bust, the U.S. recession, the demise of Fannie Mae and Freddie Mac, as well as the financial system crisis.

He is also the editor of the German edition of Weiss Research’s International ETF Trader, which has delivered overall gains (including losers) in the high double digits even while the U.S. stock market suffered its worst year since 1932.

His analysis and insights will be appearing regularly in Money and Markets.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair