Daily Updates

This brief comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

THE EUR VS. THE US$: A “Reversal” Of Fortune?: Note then the fact that the EUR “reversed” to the downside yesterday; that is, having made new high vs. the US$ the EUR traded lower and below the previous day’s low, grabbing our attention. However, the case for a weaker EUR is not truly made until this well defined trend line is well and truly broken.

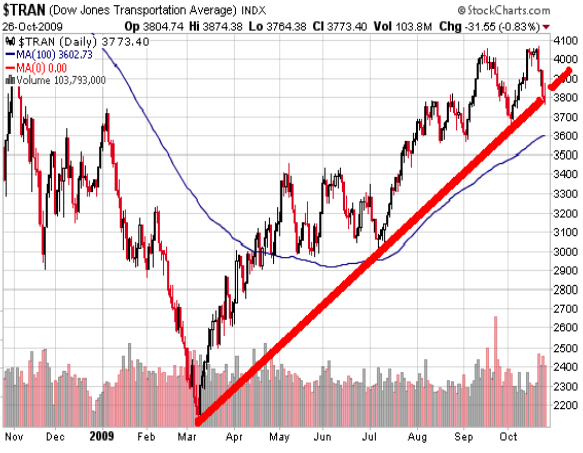

THE TRANSPORTS: A Trend Line Under Duress: Depending upon the thickness of one’s pencil when this trend line is drawn, it has either been broken or is in danger of being broken, and this follows Friday’s reversal to the downside! Technically, for the broad market, this is ominous. Attention must be paid. So pay it!

Here in the US, yesterday’s “action” in the market was perhaps some of the worst we can recall seeing in a very long while. The market opened higher; it rose sharply higher, sufficiently so that the Dow was 110 points higher very early in the session; and it closed hard upon its lows. Had we not had a series of “reversals” to the downside last week that take precedence, we’d be reporting yesterday’s action as near classic “reversal” to the downside. One by one lesser lights in the market were taken out behind the proverbial barn and shot, although the greater lights… the Apples, the Goldmans, and now the Amazons et al held well compared to the rest of the market. We fear they too may be taken out and shot sooner rather than later, for the margin clerks are now sharpening their pencils and when they do they are merciless. As we like to say, and as we have said time and time again, “When they raid the house of ill repute, the good girls and the piano player too go to jail.”

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

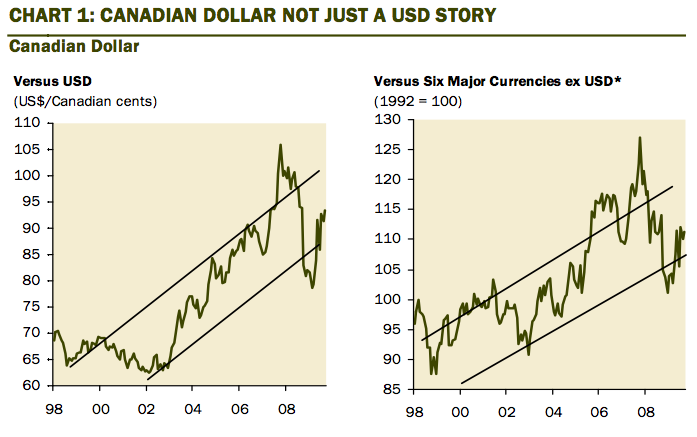

If there is one thing that Canadians are never happy with it is the Canadian dollar. When it was flirting near that record low of 62 cents nearly a decade ago, everyone lamented the future of the Loonie and closer ties to the U.S. were being recommended from various corners of Bay Street. It was too expensive to buy anything that was imported, it was too costly to make that annual trip to Florida, and tickets to a Broadway play were prohibitive. We felt poorer. We must have been doing something wrong.

But we did nothing wrong back in those days because it was 100% a U.S. dollar story. The U.S. was home to the Internet mania and all the global capital flow that came with it and Robert Rubin, Treasury Secretary at the time, was carrying out an overtly strong dollar policy partly to keep inflation at bay in what was an overheating U.S. economy. Moreover, commodities were in a bear market, and since the U.S. is a net raw material importer, this too provided impetus to the U.S. dollar rally. I recall all to well telling clients that the Loonie was actually either holding its own or appreciating against the global basket of non-U.S. dollar currencies. People would just roll their eyes because who cares about other currencies when most of our trade and travel is with the U.S. That, of course, is true, but it misses the point; the weakness in the CAD was the flip-side of the strength in the U.S. dollar. The fact that we were outperforming the other major currencies was a reflection that we were not doing anything wrong.

*A weighted average of bilateral exchange rates for the Canadian dollar against the currencies of Canada’s major trading partners. The six foreign currencies in the basketare the U.S. dollar, the Euro, the Japanese Yen, the U.K. Pound, the Chinese Yuan, and the Mexican Peso.

Source: Haver Analytics, Gluskin Sheff

…..read more HERE.

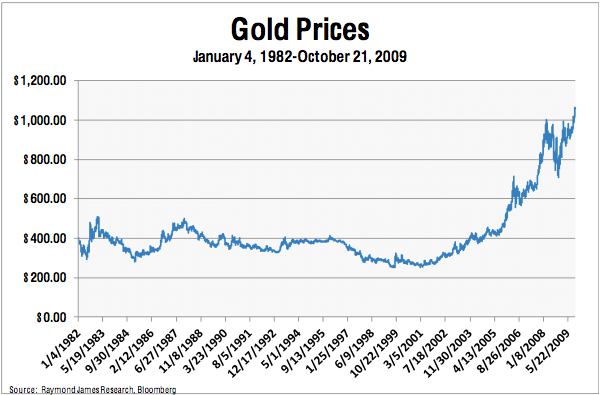

“Baruch liked gold mines. There is always a market, he pointed out, for their product, and at a satisfactory price. Gold, he insisted, is one of the very few things in the world that approaches the status of a permanent investment”……read more HERE.

Ed Note: Price perceptions via Victor Adair and graciously allowed to publish by Bill Gary, Author.

Governments throughout the world have pumped trillions of dollars into banking systems in an effort to offset the financial crisis of 2008. They have also bailed out ailing industries, initiated protectionist moves, and blatantly promoted competitive devaluations in an effort to escape deflationary economic forces. These unprecedented actions are viewed as having saved the global financial system.

However, economic growth is lagging well behind progress in financial markets. Because economic growth has not fully responded to massive liquidity injections, governments are looking at additional stimulus measures. Some recent measures appear excessive and are re-igniting speculative fever and rebuilding bubbles. The following items point to bubble building:

…..read more HERE.

Commodity Information Systems, Inc.

3030 N.W. Expressway, Suite 725

Oklahoma City, OK 73112

Toll Free Phone: (800)231-0477

Local Phone: (405)604-8726

Fax: (405)604-9696

Bill majored in Financial Management at Southern Illinois University and has attended advanced seminars on linear programming and econometrics as they relate to commodity pricing. He began his commodity career as a corn buyer in 1959 for a large milling firm in central Illinois. In four years as a corn buyer and two years as Director of Hedging Operations, he gained invaluable experience in both the cash and futures markets.

Following six years experience in the cash and futures markets, Bill joined the internationally respected research firm, Longstreet, Abbott & Company as a feed grain analyst. As a market researcher, he studied the LACO method of market analysis, designed hedging programs for some of America’s top milling firms, and authored feed grain columns for two major farm publications.

Bill moved to Dallas in 1967 and became partner in a regional brokerage firm. In 1968, he developed Commodity Information Systems (CIS), as an advisory service for the agricultural and brokerage industries. Over the years, CIS has gained an international reputation for long term commodity price forecasting.

In 1978, Bill became Regional Commodity Manager and Vice-President of E.F. Hutton & Company. He was elected to E. F. Hutton’s Director’s Advisory Council in 1980, 1981, and 1982. Bill devoted full time to developing new research methods and expanding services of CIS from the mid-Eighties until the early Nineties. In 1991, he joined Prudential Securities Inc. as a Senior Vice President and was elected to the Chairman’s Council in 1995, 1996 and 1997. Since 1999, Bill has devoted his time to expanding CIS market research.

Bill has been featured in Barrons, The Wall Street Journal, Forbes, Pro-Farmer, The Farm Journal, Business Week, US News and World Report and other publications. He has also been featured in books such as Crisis Investing by Doug Casey, Schwager on Futures by Jack Schwager, and Master Brokers by John Walsh.

“I personally invite you to find out for yourself why so many serious traders depend on CIS for their technical and fundamental research.”

-Bill Gary

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair