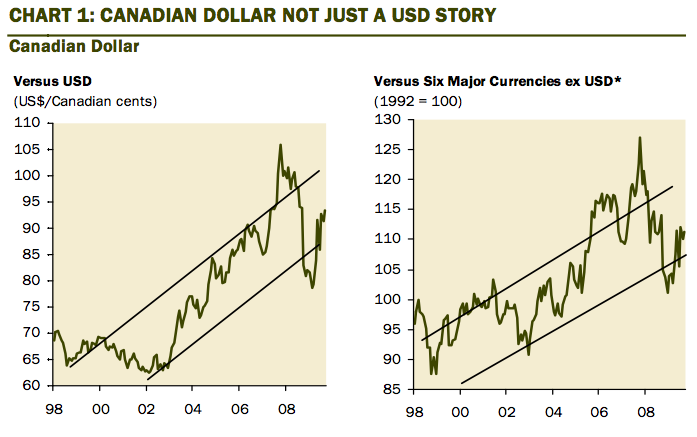

If there is one thing that Canadians are never happy with it is the Canadian dollar. When it was flirting near that record low of 62 cents nearly a decade ago, everyone lamented the future of the Loonie and closer ties to the U.S. were being recommended from various corners of Bay Street. It was too expensive to buy anything that was imported, it was too costly to make that annual trip to Florida, and tickets to a Broadway play were prohibitive. We felt poorer. We must have been doing something wrong.

But we did nothing wrong back in those days because it was 100% a U.S. dollar story. The U.S. was home to the Internet mania and all the global capital flow that came with it and Robert Rubin, Treasury Secretary at the time, was carrying out an overtly strong dollar policy partly to keep inflation at bay in what was an overheating U.S. economy. Moreover, commodities were in a bear market, and since the U.S. is a net raw material importer, this too provided impetus to the U.S. dollar rally. I recall all to well telling clients that the Loonie was actually either holding its own or appreciating against the global basket of non-U.S. dollar currencies. People would just roll their eyes because who cares about other currencies when most of our trade and travel is with the U.S. That, of course, is true, but it misses the point; the weakness in the CAD was the flip-side of the strength in the U.S. dollar. The fact that we were outperforming the other major currencies was a reflection that we were not doing anything wrong.

*A weighted average of bilateral exchange rates for the Canadian dollar against the currencies of Canada’s major trading partners. The six foreign currencies in the basketare the U.S. dollar, the Euro, the Japanese Yen, the U.K. Pound, the Chinese Yuan, and the Mexican Peso.

Source: Haver Analytics, Gluskin Sheff

…..read more HERE.