Daily Updates

“Even the most adamantly bullish amongst us has to admit that the NASDAQ’s performance over the past several days has been anything other than bullish and that the trend line drawn here has clearly been broken… clearly!”

“At the moment, we fear that we are only now seeing the beginning of this selling; that the public has only just gotten long after remaining out; and that they’ll not begin liquidating until prices are lower and their hopes have been dashed yet again.”

Finally, we wish to keep things as simple as possible, for all too often complexity breeds confusion. The advance here in the US has been led by what we’ve referred to as “The Generals:” Apple and Goldman Sachs.

They were, and they are, the very best of breed, and their leadership rallied the lesser troops around them to move higher; to charge high; to rise to greater heights in the bull run from the March lows. But yesterday, the Generals were, if not killed, seriously wounded. GS left an “island reversal” to the downside two weeks ago, and yesterday, the uptrend line that defined the bull run was unequivocally broken. One General dead.

This brief comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

“Even the most adamantly bullish amongst us has to admit that the NASDAQ’s performance over the past several days has been anything other than bullish and that the trend line drawn here has clearly been broken… clearly!”

“At the moment, we fear that we are only now seeing the beginning of this selling; that the public has only just gotten long after remaining out; and that they’ll not begin liquidating until prices are lower and their hopes have been dashed yet again.”

Finally, we wish to keep things as simple as possible, for all too often complexity breeds confusion. The advance here in the US has been led by what we’ve referred to as “The Generals:” Apple and Goldman Sachs.

They were, and they are, the very best of breed, and their leadership rallied the lesser troops around them to move higher; to charge high; to rise to greater heights in the bull run from the March lows. But yesterday, the Generals were, if not killed, seriously wounded. GS left an “island reversal” to the downside two weeks ago, and yesterday, the uptrend line that defined the bull run was unequivocally broken. One General dead.

This brief comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

Todd Market Forecast for 6pm Wednesday October 28, 2009

DOW – 119 on 2400 net declines

NASDAQ COMP. – 56 on 1800 net declines

SHORT TERM TREND Bearish

INTERMEDIATE TERM TREND Bullish

In the early going, the giant German software firm SAP had some lowered guidance going forward. That got the European markets off to a poor start and it got worse from there.

In this country, new home sales were worse than expected and the dollar again rallied. The latter was probably the main driver behind the decline on Wednesday.

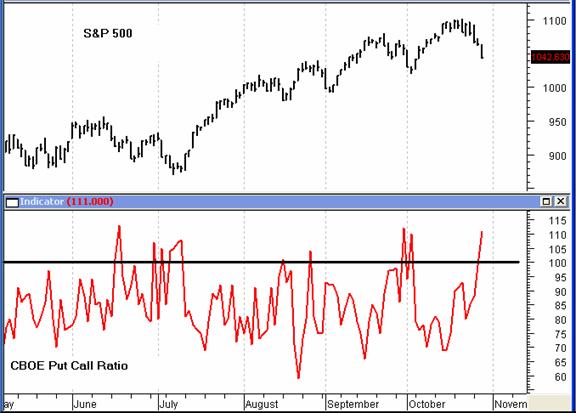

The path of least resistance appears to be down, but we could be close to a bounce. The CBOE put call ratio has been a bit too low during this drop, indicating that option buyers were looking for a buying opportunity, but that seems to have changed today. The put call ratio moved up sharply indicating that fear is finally taking hold among traders.

In the recent past, when this ratio has spiked above 1.0, there has been a tendency to bottom. That happened today. A related indicator, the VIX also had a sharp one day spike.

The rising dollar pushed gold, silver, copper and crude oil down again today. Bonds managed a rally.

BOTTOM LINE:

Our intermediate term systems are on a buy signal.

NEWS AND FUNDAMENTALS:

New home sales came in at 402,000 annualized. This was worse than the expected 440,000. Crude oil inventories increased by 800,000 barrels, less than last week’s 1.3 million. Durable goods orders rose 1.0%, better than the drop of 2.4% reported previously. On Thursday we get employment claims and GDP for the third quarter.

OTHER MARKETS

We’re on a sell for bonds as of October 8.

We’re on a buy for the dollar and a sell for the Euro as of October 26.

We’re on a sell for gold as of October 26.

We’re on a sell for silver as of October 26.

We’re on a sell for copper as of October 26.

We’ll move to a sell for Crude oil as of today October 28.

We are long term bullish for all major world markets, including those of the U.S., Britain, Canada, Germany, France and Japan.

The stock market is a lot like a teenage girl. It follows fads. In the 1960s, a primary focus was auto sales. In the 1980s, the money supply was of great concern, but now it is almost never mentioned. Currently the dollar is a significant influence.

Part of this is logical. For a number of years, there was something called the yen carry trade. Hedge funds and others would take advantage of the extremely low rates in Japan to finance higher yielding investments elsewhere.

That has now been largely replaced by the dollar carry trade since rates in the U.S. are extremely low. If the dollar rallies, it puts pressure on speculators to pay it back, thus liquidating their investments. A dollar decline increases the profits and encourages more borrowing and investment. Once the Fed starts raising rates, this will end or at least be greatly diminished.

To learn more about the Todd Market Forecast go HERE.

Stephen Todd – A Short Biography

Since 1984, the editor and publisher of the Todd Market Forecast, a monthly newsletter with emphasis on the stock market, but also with sections about gold, oil, currencies and bonds.

Steve spent a number of years as an engineer in a steel mill before becoming a stock broker with a number of Firms, including E.F. Hutton, Bache and Paine Webber.

He has published articles on the economy and the stock market in the following publications: Barron’s, Stock Market Magazine, Futures Magazine, The National Educator and others.

His stock market commentary is heard on CNBC, Bloomberg, Associated Press Radio, Business Radio Network, CKNW in Vancouver, British Columbia, KFWB, Los Angeles and ROBTV in Toronto, Ontario.

We should expect a global oil shock by 2012…at the latest. But an oil shock doesn’t have to be completely shocking. Why not beat the rush and get ready for the shock now. You might even make a few dollars in the process.

Our story begins with “Peak Oil” – the belief that conventional production of crude has already peaked, and has already slipped into an irreversible decline. As “Peak Oil” moves from mere theory to indisputable fact, the global economy will face wrenching changes. But the vigilant investor will gain an opportunity to profit along the way.

As I discussed in yesterday’s edition of The Daily Reckoning, oil production seems all-but-certain to decline, despite the huge new discoveries off the coasts of Brazil, Africa and elsewhere. In fact, production is already declining rapidly from some of the world’s largest fields. Mexico’s “Catarell” Field, like a kind of Peak Oil poster child, was producing more than 2 million barrels a day as recently as 2005. But production from this field is plummeting irreversibly toward 500,000 barrels a day, as the chart below illustrates.

The recent discoveries of deep offshore oil will certainly help slow the decline of conventional crude oil production, but theses discoveries will not come on line for many, many years.

But what about alternative energy sources? Won’t they make up for the shortfall of crude oil? No chance. Alternative energies might offset a tiny sliver of falling crude oil production. But solar panels can’t lift a fully loaded Boeing 777 off a runway…nor even lift an empty Piper Cub.

So what about the many sources of “unconventional” oil and gas? Won’t these compensate for declining production from conventional sources? The short answer is no.

Geologist Art Berman, for example, offers a decidedly negative view of the latest “big thing” – obtaining large volumes of natural gas from “tight shales.” In a comprehensive review of production and flow rates from several thousand wells drilled in the past decade in the Barnett Shale of Texas, Mr. Berman presents a gloomy forecast.

Looking at a large sampling of Barnett wells, the overall data reveal that initial gas flows decline rapidly. With some wells, the drop-off is as much as 70% in the first year, with further declines of 20% in the second year.

This hardly dovetails with the happy talk about how “shale gas” will supply US energy requirements for the next several decades, if not a couple of centuries. It appears that most Barnett wells are short-term money losers, with a few prolific wells carrying the bulk of capital expenditure.

According to Mr. Berman, the picture is not much better in other shale plays, such as the Fayetteville and Haynesville shales. And similar gloomy data are just now starting to come in on the embryonic gas play in the giant Marcellus formation of Pennsylvania.

But this bad news does need to be ALL bad. As the world’s mature and aging oil fields slip into an irreversible decline, production from the world’s new offshore discoveries will become increasingly important.

Therefore, forward-looking investors can begin TODAY to make selective investments in those sectors of the oil industry that will flourish during the coming oil shock. I am particularly fond of the “deepwater” sector…and have been urging my subscribers for several months to focus on the companies that facilitate deepwater oil production.

Marcio Mello, the former “explorationist” from Petrobras and now independent petroleum consultant, electrified the Denver meeting of the Association for the Study of Peak Oil & Gas (ASPO) with his analysis of several high-profile deepwater discoveries.

In a riveting talk that lasted well over an hour, Marcio detailed the immense petroleum potential of offshore Brazil, as well as the Amazon Basin. If Marcio’s estimates are correct, Brazil may be the location of nearly 200 billion barrels of additional petroleum resources. That’s well within the range of current resource estimates for Saudi Arabia.

For good measure, Marcio described the petroleum potential of offshore West Africa — another 130 billion barrels — as well as the Congo region, with 50 billion barrels or more.

Finally, Marcio described the “unknown potential of the US back yard, the Gulf of Mexico (GOM).” Marcio offered remarkable insight into the deep regions of the GOM, 100 miles and more offshore Texas and Louisiana. He showed early work he performed on a number of GOM areas, including the site of BP’s (BP: NYSE) recent billion-plus barrel find at the Tiber site.

If his analyses of the South American, African and GOM petroleum systems are correct, the world has access to much more conventional oil than people previously believed. But accessing and producing this oil will require a trillion-dollar level of offshore, deepwater investment. It’s a 30- to 50-year project.

“Deepwater” will be a BIG business.

Some of the companies that are well-positioned for the deepwater era of crude oil production include Petrobras, Repsol (REP: NYSE), BP (BP: NYSE) and StatoilHydro (STO: NYSE). I am also a fan of subsea equipment builders like Cameron Intl. (CAM: NYSE) and FMC Technologies (FTI: NYSE), plus service companies like Halliburton (HAL: NYSE) and Baker Hughes (BHI: NYSE).

These are a few of my favorite long-term plays for the long-term era of deep-water development.

Regards,

Byron King,

for The Daily Reckoning

Byron King

Prior to joining Whiskey and Gunpowder, Byron received his Juris Doctor from the University of Pittsburgh School of Law, was a cum laude graduate of Harvard University, served on the staff of the Chief of Naval Operations and as a field historian with the Navy. Our resident energy and oil expert, Byron is the editor of Outstanding Investments and Energy and Scarcity Investor .

Special Report – “Why Oil will Hit $200 a Barrel! What to Do to Protect Yourself Financially“

A brief excerpt of the lengthy daily internet comment by Richard Russell of Dow theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

(Ed Note: Richards comments today refer to the Dow Theory, explained below)

“Consumer sentiment — In today’s WSJ (page A5) there’s an article with the headline, “Gloom Spreads on Economy, but GOP Doesn’t Gain”. The (WSJ/NBC News) survey found the country in a decidedly negative mood, nearly a year after the election of President Obama. For the first time during the Obama presidency, a majority of Americans sees the country as being on the wrong track.”

Russell Comment –– And this gloom has occurred with the Dow rallying since March and now near 10,000. What will the mood be if this rally falls apart? What the market does coming up will be absolutely critical in shaping consumer sentiment. I believe a reaction here will turn consumers dead-bearish.

Transports — Today the D-J Transports delivered a bearish signal. Today the Transports closed below their preceding decline low (October 2) of 3692.73. This technical breakdown of the Transports will make it very difficult for the Transports to confirm any new highs in the Industrials. Note the increase in volume as the Transports plunged.

There are seven items that I don’t like about this market.

(1) Far too many distribution days.

(2) The bullish percentage of stocks on the NYSE is declining.

(3) The percentage of stocks trading above their 50-day MA is declining.

(4) The Transportation Average continues to decline (even on days when the Dow is up).

(5) The Transport Average broke below a preceding decline low today.

(6) Sentiment is too bullish about the market. Nobody expects this rally to top out and fall apart.

(7) My PTI is now barely above its MA and therefore very close to a sell signal.

Stock Recap — Percentage changes for the year (as of yesterday’s closing).

Dow…..+ 12.60%

Dow Transports……+4.73%

Dow Utilities……- 0.10%

NYSE Comp…..+20.41%

NASDAQ…..+34.18%

S&P 500…..+17.73%

S&P 400…..+27.41%

Wilshire 5000…..+20.72%

Russell 2000…..+17.53%

In all, an ominous picture, and those stocks you’re not in love with should be jettisoned.

Ed Note: The Dow Theory Explained by Richard Russell

The following piece is for serious market students. What I wrote below is information that you will rarely see anywhere else. I hope it will dispel some of the misconceptions and utter nonsense that has circulated about Dow Theory. Read on.

DOW’S THEORY: From the very beginning (July 1958) I called my report Dow Theory Letters, and there are obvious reasons for that. The reasons are (1) I truly believe in the basic tenets of Dow Theory, and (2) I wanted to teach Dow Theory and I wanted to insure that the Dow Theory tenets, rules and observations were passed on to future generations.

Before I start this section let me say that there are hundreds of predictive and trend-following techniques that are now used (some very worthwhile, others less so) by market students. I follow dozens of these techniques and devices, but none of them will ever replace or negate the basic tenets of Dow Theory.

I’ve been writing these reports for 41 years and never a month goes by that someone doesn’t announce that the Dow Theory is antiquated and that it no longer works. The detractors, almost to a man, do not know their subject and have, in almost all cases, never studied Dow Theory. The Dow Theory (actually it is a set of observations) has basically to do with buying great values and selling those values when they become overpriced.

Value is the operative word in Dow Theory. All other Dow Theory considerations are secondary to the value thesis. Therefore, price action, support lines, resistance, confirmations, divergence — all are of much less importance than value considerations, although critics of the Theory seem totally unaware of that fact.

I’ve spent two-thirds of my life studying and writing about the markets. And I’d say that without a shadow of a doubt the material which has served me best are the books and papers written by the great Dow Theorists — Charles H. Dow, William P. Hamilton, Robert Rhea and E. George Schaefer.

First, let’s talk about Charles Dow, a man who, by any reckoning, must be considered a brilliant market observer and theorist. Dow started his career as an investigative reporter, specializing in business and finance. In 1885 (and few people are aware of this), Dow became a member of the New York Stock Exchange, and this provided him with an intimate knowledge of how the market works. In 1889 Dow began publishing a little newspaper which he called The Wall Street Journal. Between 1899 and 1902 Dow wrote a series of editorials for his Journal, editorials that many consider among the finest ever to come out of Wall Street. Written almost 100 years ago, these editorials are as pertinent and valuable today as they were the day they were written.

Dow was a very modest man, and although his admirers begged him to write a book explaining his theories, Dow stubbornly refused. However, Dow’s good friend, S.A. Nelson, published 15 of Dow’s Wall Street Journal editorials in a little volume entitled, “The ABC of Stock Speculation.” A footnote at the bottom of each chapter refers to the editorial as “Dow’s Theory.” But Dow himself never once used the term.

Following Dow’s death, two other men took over editorship of the Journal for brief periods. They were followed by William P. Hamilton, who was the fourth editor of the WSJ. Hamilton wrote a brilliant series of 252 editorials. These pieces appeared in the Journal between 1903 and 1929, and in Barron’s (the Journal’s sister publication) during 1922 to 1929. As time passed, Hamilton’s writing attracted a wide and devoted following. In 1926 Hamilton wrote his landmark book entitled, “The Stock Market Barometer,” in which he presented his own version of Dow Theory.

Hamilton had been Dow’s understudy at the Journal, and in his book he included much of Dow’s market observations and philosophy. But Hamilton also presented his own views on Dow Theory, and it was Hamilton who first defined the confirmation principle of the Averages. Hamilton died in 1930 soon after writing his most famous editorial, “The Turn of the Tide” (written on October 25, 1929). This fateful forecast served as the obituary for the amazing and hugely speculative 1921-’29 bull market.

The next great writer in the Dow Theory chain was Robert Rhea. Rhea was a devoted student of Hamilton’s, and Rhea adhered closely to Hamilton’s version of Dow Theory. Over a period of many years, Rhea codified and refined Dow Theory, always deferring to Hamilton in his explanations. I’ve studied every work and sentence that Rhea ever wrote, and in my opinion, Rhea was the greatest market trader of his time.

Rhea possessed a marvelous, instinctive gift for reading the Averages. He had an uncanny ability to identify and trade on the secondary as well as the primary trend of the market. Rhea was bed-ridden with TB, and he relied on his remarkable trading ability to support himself and pay his costly medical bills.

On November 12, 1932, Rhea started a stock market service which he titled, “Dow Theory Comment.” The service was successful from the start. Rhea called the exact bottom of the bear market on July 8, 1932, a feat which I consider one of the most remarkable in the history of stock market analyses. Rhea’s early letters were written during the depths of the greatest depression in American history, and you can imagine the skepticism with which his almost shocking bullish reports were greeted. Rhea also called the turn (to the downside) in the bear market of 1937, and this feat, even more than his 1932 bull market call, made Rhea a household name on Wall Street.

Sadly, Rhea’s disease took its toll. Only seven years after he started his advisory service, Rhea died (1939). Following Rhea’s death, the Dow Theory lay dormant for the many years during WWII and afterwards.

The next major figure in Dow Theory was E. George Schaefer of Indianapolis. Schaefer started his career as a stock broker with Goodbody & Co. He spent many years studying the writing of the great Dow Theorists who preceded him. But Schaefer concentrated his studies on the brilliant and seminal writings of Charles Dow. Schaefer was a firm believer in VALUES. One of Schaefer’s favorite quotes from Dow was, “An investor who will study values and market conditions, and then exercise enough patience for six men will likely make money in stocks.”

Another Dow quote used by Schaefer states, “It is always safer to assume that values determine prices in the long run. Values have nothing to do with current fluctuations. A worthless stock can go up 5 points just as easily as the best, but as a result of continuous fluctuations the good stock will gradually work up to its investment value.”

Schaefer believed that both Hamilton and Rhea placed too much emphasis on the pattern of the Averages and not enough emphasis on the principle of buying great values and holding those values throughout the life of a bull market. Schaefer wrote, “It has always been of interest to me that Hamilton and Rhea . . . both steered away from Dow’s thinking in many respects. Hamilton was very reluctant to give Dow the full credit he deserved. And Rhea, in turn, disregarded the works of Dow almost entirely and specialized in trying to improve the Hamilton version of Dow Theory.”

In 1948 Schaefer started his own advisory service which he called, “Schaefer’s Dow Theory Trader.” Schaefer’s timing was fortunate but more probably brilliant. On June 13, 1949, with the Dow at a multi-year low of 161.60, one of history’s great bull markets began. Exactly five days from that low, on June 18, 1949, Schaefer wrote what I consider an advisory masterpiece (I still have that report). In that piece Schaefer stated his reasons for believing that a great buying area was at hand and that a major bull market had begun.

In that June 18, 1949 report Schaefer wrote, “The philosophy of Charles Dow always gave first consideration to values, then to economic conditions and third to the action of both the Industrial and Rail Averages. When the low point of a bear market is reached, values will be the first indication of a change in trend. In the past 17 years only three opportunities have presented themselves to buy stocks at great values. Now the fourth opportunity is making its appearance.”

Schaefer’s June ’49 forecast turned out to be uncannily accurate. In June the Dow turned up from its 161.60 low, and a great bull market began. Schaefer stayed with the bull market through thick and thin until 1966. On February 9, 1966, 17 years later, the Dow topped out at a value of 995.15. Those who followed Schaefer’s Dow Theory interpretations and investment procedures (i.e., those who held their stocks throughout the bull market as Schaefer repeatedly advised) made fortunes.

One of the reasons Schaefer started his advisory service was to present what he terms his “New Dow Theory,” a set of principles which he insisted “could be applied profitably to present-day markets.” Schaefer wrote in 1960, “A study of the Averages themselves can be highly rewarding. But in my opinion, a forecast based on past movements of the Averages cannot be conclusive. Predictions of events to come are more reliable if they can be reinforced by analysis of other technical and more conclusive factors.”

What were the “other factors” which Schaefer referred to? Some of them were values (and again I emphasize values), the 200-day moving average of the Dow, the short interest ratio, the advances and declines, Dow’s 50% Principle, market sentiment, market phases, and the yield cycle. Remember, prior to Schaefer, orthodox Dow Theorists tended to avoid all “extraneous” items other than the pattern of the Averages and volume, claiming that other items only interfered with pure, basic, Dow Theory studies. Schaefer disagreed vehemently.

Schaefer possessed great market intuition, and he used his market instincts plus his new tools to ride the great 1949-’66 bull market all the way from the bottom in 1949 to the top in 1966. Through reactions, corrections, panics and dips, Schaefer insisted that his subscribers hold their shares and buy more during all periods of weakness.

That may sound easy, but believe me it is not. The number of people who hold stocks from the beginning to the end of a bull market can probably be counted in the hundreds. In early-1966, Schaefer turned bearish on the market (based on third phase considerations and overvaluation of stocks), and he advised his followers to “sell out.” Schaefer remained bearish until the time of his tragic and untimely death (suicide) in 1974.

Although Hamilton and Rhea took careful note of the secondary reactions in bull and bear markets, Schaefer advised his subscribers to ignore these “temporary reactions,” and to remain invested in harmony with the primary trend of the market. In his historic report of June 18, 1949, Schaefer wrote, “Once stocks are purchased, both the minor and secondary movements in the market should be completely disregarded. A new period of prosperity will follow, once the present recession has run its full course.” We now know how prophetic those words were (words which were written during a time of extreme fear and gloom) .

Later Schaefer wrote, “So far as I can ascertain from his original writings, Dow had an open mind, and there was a great deal of flexibility in his thinking regarding the price movements.”

The following is extremely important, and subscribers should take careful note of this: Schaefer believed that mass emotions were changing the character of the stock market. He realized that Wall Street was gathering a much larger following year after year, and that the American public was becoming much more involved with investments (today, of course, Wall Street has gone both electronic and global). This relatively new phenomenon of mass emotions, Schaefer believed, had to be taken into consideration as far as classic Dow Theory was concerned.

Wrote Schaefer, “My new Dow Theory involves a broad, balanced manner of thinking about the market and your own emotions. It is a far cry from the narrow ‘system’ that places a complete reliance upon what the Averages do. Yes, we who study the new Dow Theory watch the Averages. But along with any such observations we realize and understand that the market is composed of people of all types, and that all people are born emotional.”

So what was the result of Schaefer’s emphasis on the emotions of an enormous and growing investment public? It was this — Schaefer allowed for secondary reactions to far overshoot the restrictions which were laid out by orthodox Dow Theory. Years earlier Rhea had written that in a bull market, secondary reactions tend to retrace one-third to two-thirds of the preceding uncorrected primary advance while tending to last three weeks to three months.

Schaefer dismissed Rhea’s “out-dated concepts.” Schaefer believed that mass psychology and the intense emotions of the public could take the Averages well beyond the “normal bounds” outlined by Hamilton and Rhea. Wrote Schaefer, “Today our new Dow Theory allows the crowd to get as emotional in its selling or buying as it will — with no restrictions whatever on the duration or extent of the secondary or intermediate trend. In primary bull markets, when things get scary, we simply wait for the fearful to sell out, and then we assume that the main primary trend will resume as expected. In primary bear markets, just the opposite is true.”

This “new Dow Theory” thinking proved extremely valuable in late-1957 when a severe secondary reaction hit Wall Street. When the Averages broke through their preceding secondary lows, many orthodox Dow Theorists, who relied almost totally (as most do today) on the pattern of the Averages, proclaimed that a bear market had started. These bears ignored such critical factors as the phases, length of the bull market, values, Dow yield, etc.

Schaefer differed totally (as I did in 1957) with the prevailing Wall Street opinion. Both of us insisted that the bull market had not yet experienced a classic speculative third phase and that the late-1957 cave-in was not a bear market but a severe secondary reaction. We held that the reaction had been intensified by extraordinary public fear, fear that was triggered by the violent breakdown in the Averages.

In fact, I was so certain during 1957-’58 that we were witnessing a bull market correction rather than a primary bear market that I started Dow Theory Letters at that time. Furthermore, in December 1958, I wrote my first article for Barron’s (entitled “Dow Theory Revisited”). That Barron’s article drew a tremendous response and was instrumental in putting me in business (in the years that followed I wrote about 30 additional articles for Barron’s).

Basic to both Schaefer’s and my thinking during 1957-’58 was the fact that we had not yet experienced a bull market third speculative phase. Also, during the drastic 1957 decline the 50% Principle remained bullish.

Let me explain because this is important. The Dow had risen from a 1953 low of 255.49 to a record high in 1956 of 521.05. The halfway or 50% level of that three-year rise was 388.27. On the vicious 1957 decline the Dow collapsed to a low of 419.79, a level which was well above the 388.27 or the 50% level of its preceding rise. The fact that on the decline the Dow could retain better than half the gains of the 1953-’56 rise was a powerful bull argument, particularly since this phenomenon occurred in the face of such universally black pessimism (by the way, I have never, before or since, seen gloom to match that which existed during the 1957-’58 recession and market collapse).

Back to George Schaefer. Schaefer used the 200-day moving average of the Dow to advantage in his work. But he warned “that as with other technical studies, the 200-day moving average should never be considered alone. My experience has been that interpretations under the 200-day moving average rule must always be correlated with other studies.”

The experience during the 1949-’66 bull market served me well. The 200-day MA turned down in 1953 (during a secondary correction), and it turned down again in 1956 (during another secondary). Neither of these downturns in the MA indicated that the primary trend of the market had turned bearish, and each of the downturns in the MA was followed by a major rise as the bull market reasserted itself. Thus, those who say that the direction of the 200-day MA identifies the direction of the primary trend would do well to study history. But Schaefer noted, “the 200-day MA should never be used alone and to do so can cause expensive mistakes.”

I wrote the foregoing because I wanted to give subscribers an accurate (even though brief) view of Dow Theory and its evolution over the past 90 years. Few, very few, market practitioners have ever made a serious study of Dow’s Theory, although many analysts mouth meaningless Dow Theory platitudes. I know of only a handful of people who have ever read the works of Dow, Rhea, Hamilton or Schaefer. Yet, the Dow Theory remains the basis of all technical analysis. The Theory also constitutes the basis for much intelligent and profitable investing. I have shown how the Theory has evolved through the years. I have also attempted to show how the Theory has been improved with each Dow Theorist and how each practitioner has worked with the Theory and applied it to the particular markets of his time.

I’ve tried to carry on the work of Dow, Hamilton, Rhea and Schaefer. I believe, however, that the stock market is far more difficult today than ever before, mainly because so many analysts, professionals, money managers, arbitrageurs, speculators and serious individuals are involved, and competing for profits (and increasingly, for short term and even intra-day profits). Furthermore, trading has been speeded up and broadened tremendously through the use of computers and the Internet. Finally, the arrival on the scene of “derivatives,” options, futures, puts, calls, etc., makes the market game bigger, faster, more manipulative, more hazardous — and far more deceptive than ever before.

In the end, however, the “hidden ingredient” for market success is the practitioner’s own instincts or intuition. Market analysis, as some many have observed, is an art, not a science.

I guess every Dow Theorist (and every market practitioner) has added or latched on to a few devices which he feels will help him with his market studies. I’ve developed my Primary Trend Index. This composite Index has been a huge help to me in my own trading. As a matter of fact, many of my own subscribers base their market position strictly on the trend of the PTI.

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold.

There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974. He loaded up on bonds in the early 80’s when US Treasuries where yielding 18%.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair