Daily Updates

Bill Murphy had this chart in his daily message today. It shows how the U.S. Dollar has been in a series of self-correcting oversold periods that have grown shorter each time. It’s interesting to note that the 50-Day M.A. has held almost the entire time. The dollar continues to be a key factor in most markets and nothing appears on the horizon that can change that.

Company Alert – 3:08 PM on Tuesday, November 3rd, 2009

In previous articles I have told you about the leverage that you will get from emerging producers. Gold hit an all time high today of $1089. Timmins Gold is so close to pouring gold you can taste it.

….read more HERE.

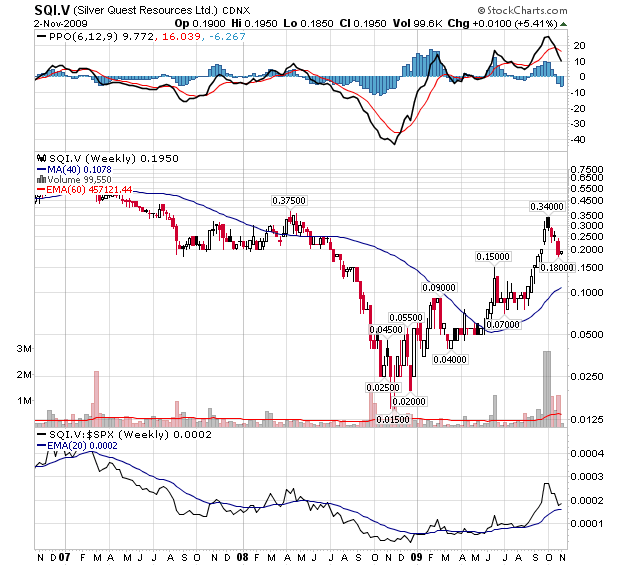

I am pleased to have been engaged by Silver Quest Resources. Silver Quest and it’s predecessors have a long history in the mining industry as one of the first junior mining companies to list on the Venture Exchange. Silver Quest is an exploration company filling a niche in British Columbia, Yukon, and Ontario by advancing and developing silver and gold resources. I like this company for three main reasons. The company’s president, Randy Turner, is committed to the success of the company, as proven by his more than 15 years of involvement in various roles. Second and third, I like the two main assets, the Capoose –Silver Trend property and the Davidson Property, both silver and gold properties with vast upside potential located in central BC.

Great Leadership

Mr. Randy Turner, the new President and CEO of Silver Quest, is a skilled and qualified professional geologist with over thirty-eight years of mineral exploration, business and financing experience to draw from. Mr. Turner has spent the majority of his career working for Canadian mineral companies. As president of Winspear Diamonds Inc., Mr. Turner guided the company from the discovery of the Snap Lake diamond deposit in northern Canada through its sale to De Beers Mining for C$305 million.

Prior to his position at Winspear, Mr. Turner was president of Trimin Resources Ltd. where he was involved in the development and sale of the McIlvenna Bay copper/zinc deposit in Saskatchewan. Mr. Turner also spent many years working on property acquisitions and joint ventures for Esso Minerals in Canada and AGIP Mining in the US and Australia. Mr. Turner’s knowledge, contacts and experience in the exploration industry are an invaluable asset to Silver Quest, and one of the reasons, I believe, that this company is truly one to watch as they have great potential knocking at their door.

BC Properties

….read more HERE.

To HERE Peter speak and others speak on Trading go HERE:

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.

Since March there has been a massive rally in all sorts of risky assets – equities, oil, energy and commodity prices – a narrowing of high-yield and high-grade credit spreads, and an even bigger rally in emerging market asset classes (their stocks, bonds and currencies). At the same time…..

the dollar has weakened sharply , while government bond yields have gently increased but stayed low and stable.

This recovery in risky assets is in part driven by better economic fundamentals. We avoided a near depression and financial sector meltdown with a massive monetary, fiscal stimulus and bank bail-outs. Whether the recovery is V-shaped, as consensus believes, or U-shaped and anaemic as I have argued, asset prices should be moving gradually higher.

But while the US and global economy have begun a modest recovery, asset prices have gone through the roof since March in a major and synchronised rally. While asset prices were falling sharply in 2008, when the dollar was rallying, they have recovered sharply since March while the dollar is tanking. Risky asset prices have risen too much, too soon and too fast compared with macroeconomic fundamentals.

So what is behind this massive rally? Certainly it has been helped by a wave of liquidity from near-zero interest rates and quantitative easing. But a more important factor fuelling this asset bubble is the weakness of the US dollar, driven by the mother of all carry trades. The US dollar has become the major funding currency of carry trades as the Fed has kept interest rates on hold and is expected to do so for a long time. Investors who are shorting the US dollar to buy on a highly leveraged basis higher-yielding assets and other global assets are not just borrowing at zero interest rates in dollar terms; they are borrowing at very negative interest rates – as low as negative 10 or 20 per cent annualised – as the fall in the US dollar leads to massive capital gains on short dollar positions.

…..read more HERE.

My position in my email last week was that although October 28th is still a good entry date, there may be value in delaying an entry into the market. As November, December and January have on average been the best three contiguous months of the year, investors should make sure that they do not sit on the sidelines too long. A good seasonal strategy is to start entering the market as of November 2nd and finish allocating funds to the market by November 13th.

….read more HERE.

Editor Note: I highly recommend a regular monday visit to this Don Vialoux report. Today he analyses an astonishing 50 plus Stocks, Commodities and Indexes.

Buy in October and go away

History shows that the best time to “buy the equity market” each year is near the end of October. When is the best time to “buy the equity market” this year?

….read more of Don Vialoux’s National Post article HERE.

S&P 500 futures were up 6 points in pre-opening trade. Futures are responding to weakness in the U.S. Dollar as well as encouraging news from China and from the semiconductor industry. China’s Purchasing Manager’s Index rose again last month to reach an 18 month high implying accelerated economic growth. The Semiconductor Association announced that world wide semiconductor sales in the third quarter rose 19.7% on a year over year basis.

Commodities priced in U.S. Dollars moved higher including gold, copper and crude oil.

CIT Group moved into Chapter 11 bankruptcy over the weekend. The stock has fallen to $0.38 this morning from a close at $0.72 on Friday. The move had been anticipated and did not influence equity index futures.

Analysts are starting to take a more positive stance on the North American forest product industry. Credit Suisse upgraded Weyerhaeuser this morning and boosted its target price from $34 to $37. Domtar is up 5% after RBC Capital upgraded the stock from Outperform to Top Pick. Target was raised to $70. Also, Raymond James upgraded Domtar from Market Perform to Outperform. Demand for lumber and fine papers is increasing. Lumber prices broke to a two month high on Friday. ‘Tis the season for forest product stocks to move higher!

Target goes from $100 U.S. to $50 U.S. Citigroup suggests that new competition will reduce growth prospects.

Ford gained 9% after reporting better than expected third quarter earnings. Consensus was a loss of $0.12 per share. Actual was an operating profit of $0.26 per share.

Yum! Brands added 2% after RBC Capital raised its rating from Sector Perform to Outperform.

Cott Corp. was upgraded by Bank of America/Merrill to Outperform from Sector Perform.

Economic News This Week

The economic focuses this week are on the FOMC meeting on Wednesday and the October employment report on Friday.

September Construction Spending to be released at 10:00 AM EST on Monday is expected to decline 0.2% versus a gain of 0.8% in August.

October ISM to be released at 10:00 AM EST on Monday is expected to improve to 53.0 from 52.6.

September Factory Orders to be released at 10:00 AM EST on Tuesday are expected to improve 0.9% versus -0.8% in August.

October ADP report to be released at 8:15 AM EST on Wednesday is expected to fall 190,000 versus a fall of 254,000 in September.

October ISM Services to be released at 10:00 AM EST on Wednesday are expected to improve to 51.5 versus 50.9 in September.

Meeting minutes from the FOMC meeting to be released at 2:15 PM EST on Wednesday are expected to maintain the Fed Fund rate at 0.25%.

Preliminary third quarter Production to be released at 8:30 AM EST on Thursday is expected to improve 6.5% versus a gain of 6.6% in the second quarter.

October Non-farm Payrolls to be released at 8:30 AM EST on Friday are expected to decline by 175,000 versus a decline of 263,000 in September. The October Unemployment Rate is expected to increase to 9.9% from 9.8% in September. October Hourly Earnings are expected to improve 0.1% versus 0.1% in September.

September Wholesale Inventories to be released at 10:00 AM EST on Friday are expected to decline 1.0% versus a 1.3% decline in August.

Earnings News

This week is the busiest week for third quarter earnings reports on both sides of the border.

Monday sees Cameco, FNX Mining, Ford, Humana, Kinross, Magna International, Power Corp. and West Fraser.

Tuesday sees Archer Daniels, Emerson Electric, Hudbay Mining, Kraft, Pitney Bowes, Russell Metals, Saputo, Talisman, Viacom and Yamana.

Wednesday sees Aecon, Agrium, Baker Hughes, Cisco, Comcast, Enbridge, Fannie Mae, Goldcorp, IAMGold, Pulte Homes, Time Warner, TransCanada and Yellow Pages.

Thursday sees Biovail, Cdn. Natural Resources, Fortis, Gerdau AmeriSteel, Great West Life, Linamar, Manitoba Telecom, ManuLife, Sun Life, Thomson Reuters and Wendy’s

Friday sees Brookfield Asset Management and Suncor.

Equity Index Trends

The ratio of S&P 500 stocks in an uptrend to a downtrend (i.e. the Up/Down ratio) plunged last week from 5.91 to (289/131=) 2.21 (including 22 stocks that broke support on Friday). The Up/Down ratio continues to trend lower from an intermediate overbought level.

Bullish Percent Index for S&P 500 stocks dropped last week from 84.40% to 74.8% and fell below its 15 day moving average. The Index remains intermediate overbought and has established a downtrend. .

……view the analysis of more than 50 Charts HERE

Over the last few weeks,we talked about the process of mining and mining feasibility studies to help us better understand the basics of investing in resource-based companies. As a follow up to last week’s newsletter on mining feasibilities, I said that we would go into more depth about the principles of these studies.

But this week, I am skipping that because I want to bring your attention to an incredible opportunity that is slowly, yet rapidly, beginning to show itself.

We all know the world is beginning to doubt the US dollar. We’ve all heard the rumours of talks amongst powerful nations to remove the US dollar as the main currency for trading oil. We know inflation will eventually follow.

But there is shocking proof that even the US is beginning to doubt the Dollar.

Hidden from the media over the past few weeks, the U.S. Treasury has been liquidating billions of U.S. dollars and trading it for a special currency you may have NEVER heard of – the same currency that China, Russia, oil-bearing Gulf countries, the UN, the IMF (International Monetary Fund), the World Bank, and many others have already suggested to replace the greenback as the world’s main reserve currency.

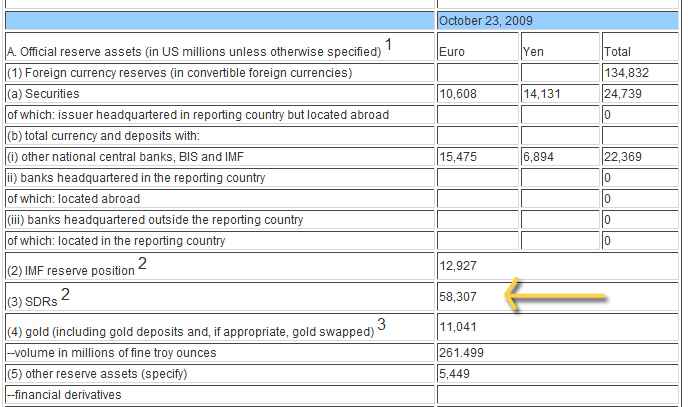

It’s called the Special Drawing Rights (SDR).

The SDR is an international reserve asset, created by the IMF in 1969 to supplement its member countries’ official reserves. Its value is based on a basket of four key international currencies (currently the U.S. dollar, Euro, Japanese Yen, and the British pound), and SDRs can be exchanged for freely usable currencies.

General SDR allocation took effect on August 28, 2009 and a special allocation took place on September 9, 2009, which increased the amount of SDRs from SDR 21.4 billion to SDR 204.1 billion (currently equivalent to about $317 billion). And guess who took a large chunk of that?

Current SDR holdings in the U.S. Treasury now account for nearly 30% of the U.S. total foreign currency reserves.

Ed Note: larger image HERE

We’re not telling you to go out there and pick up this currency – you can’t.

But this is a clear sign that the U.S. government is making moves to hedge against its own falling Dollar.

And if ever there is an actual changeover in reserve currency dominance by the US (which many powerful people are discussing) it would send the value of the U.S. dollar plummeting. Combine that with the inflationary woes that everyone has been talking about, we could see the U.S. dollar at all-time lows.

The U.S. national debt is crossing $12 trillion – about $40,000 for each citizen – and doesn’t include other future financial obligations, like Social Security and government-sponsored health care under Obama’s rule. Analysts estimate that these future obligations could cost the United States up to $100 trillion!

With an exploding budget deficit and thinning credit, the federal government will be forced to create a plethora of new U.S. dollars to help finance the country and repay debt.

Although this inflationary conundrum has yet to place, the smartest and richest all know that it will happen eventually – including the US. Before this happens, we need to prepare for the upswing in the right markets.

Fortunately, there’s still some time before this strong inflationary period will start to have a negative effect on the dollar. This means good news for us because it gives us enough time to prepare ourselves for the bang.

One of the best ways to hedge against a falling U.S. dollar and inflation is, of course, by investing in precious metals such as gold and silver. Other commodities – such as energies, grains, softs, and meats – also do well during times of a falling U.S. dollar.

There are plenty of easy ways to invest in these commodities, including ETFs, stocks, futures, and options. Exposure to other foreign currencies, such as the Euro and Japanese Yen, can also provide a good hedge against a devaluing dollar.

For us, we like to stick with the resource junior stocks.

They have the ability to indirectly take advantage of climbing commodity prices and have the ability, at any given moment, to give you a significant return on your investment – more so than buying bullion or ETF’s themselves.

The most powerful governments, central banks, and investment groups in the world continue to hoard their gold reserves in anticipation of a significant rally in prices. Over the past few weeks, our mailboxes have been littered with comments and suggestions requesting us to focus more on gold and gold company editorials.

It’s no surprise that gold has become the hottest topic in 2009. Next week, we’ll talk about why it has everyone’s attention and how we can profit from this apparent opportunity.

Until next week…

See more great Equedia.com articles and videos HERE.

Equedia is an investor relations firm, a dedicated social media platform for business, and a financial broadcaster of syndicated stock market content.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair