Daily Updates

Comment by Richard Russell first: Gold — The daily gold chart (I’m using GLD as a proxy for gold) is worth studying. GLD has advanced above its 50-day moving average. It has also carved out a “head-and-shoulders bottom” pattern. Today GLD surged above the blue down-sloping resistant trendline. GLD appears to be in the process of testing its recent (Jan. 11) peak at 112.85. If 112.85 is bettered, GLD (and gold) will probably try for a new high, putting April gold at 1213.

Marc Faber, George Soros agree gold prices set to rise

Is gold in a cyclical bull market that could last for years to come or is it another asset bubble created by loose monetary conditions about to crash? The debate has been raging for some time and shows no signs of abating.

But, the strange thing about this debate is that some of the perceived opponents may actually be more in agreement than they would let us believe.

Renowned billionaire financier George Soros became the latest investor to issue a warning in January that with interest rates low around the world, policymakers are risking generating new bubbles which could cause crashes in the future.

Last month it was revealed that Soros more than doubled his fund’s holding in the biggest gold exchange-traded fund (GLD) in the fourth quarte of 2009r, according to a filing with the US Securities and Exchange Commission.

Soros Fund Management LLC held nearly 6.2 million shares of GLD valued at about US$663 million as of December 31, adding 3.728 million shares valued at US$421 million That’s up from roughly 2.5 million shares at the end September.

Speaking to The Daily Telegraph, on the fringe of the World Economic Forum, Soros said: “When interest rates are low we have conditions for asset bubbles to develop, and they are developing at the moment”. The ultimate asset bubble is gold,” he added…

…..read more HERE

Here we go again. The Canadian dollar is rapidly approaching parity with the US variety.

….read more HERE

It is astounding how many economists, government officials, and Wall Street strategists construe the current economic conditions as evidence of a bona fide recovery. It is a testament to the power of the rose colored glasses handed out by our nation’s leading universities that such a feeling could be widely held despite the clear and present danger that compounds daily. The myopia leads us to enact policies that actually exacerbate our problems. The “remedies” are postponing, perhaps indefinitely, a true recovery.

The oracles who have described the nature of this imminent recovery do so based on their conviction that consumer spending is slowly returning to levels that existed prior to the recession. New data released today seems to support this view, with consumer spending up 0.5% in January.

However, missing from their analysis is any plausible explanation as to why consumers will be able to sustain such spending given the plunge in income and credit, and the lack of available savings. In fact, the same January spending report showed that personal income increased by only 0.1%, while the savings rate slowed to the smallest since 2008.

I would challenge those who fantasize about a consumer-led recovery to describe where the spending money will come from. Most consumers are tapped out, millions are unemployed, and home equity has been wiped out. The only reasonable thing for them to do is to pay down debt and sock away as much money as possible to rebuild their savings.

Beyond the question of “how” the spending could be achieved, is the deeper question of “why” such activity should be sought at all. Excessive spending, fueled by an insane housing bubble and catalyzed by reckless monetary and fiscal policy, was the reason that our current recession became unavoidable. Why would we want to go down that road again?

During the run up to the crash, excess spending had created economic distortions that have yet to be resolved. Too many resources, including land, labor, and capital, were devoted to servicing an unsustainable economic model in which Americans borrowed money to buy homes, products and services they really could not afford. In many cases consumer behavior was influenced by overly optimistic assumptions regarding real estate related riches.

However, now that the real estate bubble has burst, Americans are coming to terms with a more sober reality. Many have cut up their credit cards, dramatically reduced their spending, and have squirreled away as much money as they can. This change in behavior should necessitate a dramatic shift in the labor market as workers move away from jobs associated with consumer spending and toward jobs associated with real production, primarily for exportable goods.

The real problem is that monetary and fiscal policy designed to re-inflate the burst spending bubble is preventing this transition from taking place. As a result we are not creating the jobs we need to replace – the ones we have lost in mortgage servicing, home improvement, and real estate sales (which we never really needed to begin with). As these jobless remain unable to find alternative employment, our economy will continue to languish.

Some will argue that the new jobs created by government stimulus spending will provide the additional purchasing power necessary to revitalize consumer spending. There are two problems with this expectation. First, those jobs being “created” by the government are outnumbered by those being destroyed by government domination of resources. Second, even if it were possible for job growth to return, having hopefully learned from their mistakes, workers will be far more frugal with their paychecks than they were in the past.

Others hope that rising real estate prices will give consumers more confidence to spend. The reality is that housing prices are still too high and will likely fall further. But even if they did rise, consumers will still be reluctant to resume their shopping spree. Home equity extraction loans, which just a few years ago turned houses into ATMs, are now much harder to come by. When it comes to spending, it’s not just about confidence; it’s about cash.

The only possible way consumers can spend is if the government gives them the money. However, since the government cannot legitimately give money to one American without first taking it from another, the most likely means of doling out cash will be to run it off the printing presses.

That, in a nutshell, is our government’s plan for economic recovery. Print a bunch of money and give it to consumers to spend. This is not a plan for recovery but a recipe for disaster. Those betting that this program can succeed in putting together a healthy and sustainable economy simply do not understand the nature of their wager. The smart money is going the other way.

Peter Schiff

Mr. Schiff is one of the few non-biased investment advisors (not committed solely to the short side of the market) to have correctly called the current bear market before it began and to have positioned his clients accordingly. As a result of his accurate forecasts he is becoming increasingly more renowned, and has been quoted in many of the nation’s leading newspapers, including The Wall Street Journal, Barron’s, Investor’s Business Daily, and The Financial Times among others.

His best-selling book, “Crash Proof: How to Profit from the Coming Economic Collapse” was published by Wiley & Sons in February of 2007. His second book, “The Little Book of Bull Moves in Bear Markets: How to Keep your Portfolio Up When the Market is Down” was published by Wiley & Sons in October of 2008.

Mr. Schiff began his investment career as a financial consultant with Shearson Lehman Brothers, after having earned a degree in finance and accounting from U.C. Berkeley in 1987. A financial professional for over twenty years he joined Euro Pacific in 1996 and has served as its President since January 2000. An expert on money, economic theory, and international investing, Peter is a highly recommended broker by many leading financial newsletters and investment advisory services. He is also a contributing commentator for Newsweek International and served as an economic advisor to the 2008 Ron Paul presidential campaign. He holds FINRA Series 4,7,24,27,53,55, & 63 licenses.

I have spent a considerable amount of time discussing how a supply crunch is looming in the gold market. With retail investment demand soaring, and central banks switching from large, net sellers to large net buyers, the world’s gold-shortage will continue to intensify — despite the fact that nearly every ounce of gold ever mined still exists (in some form) around the world.

Of course, countless thousands of tons of this gold are incorporated into some of the world’s most-revered artifacts and religious symbols — and thus (for all intents and purposes) it is gone forever.

Meanwhile, mine production has remained essentially flat — despite a quadrupling of the price of gold over the last decade. While there has been a slight hiccup in supply in 2009, it is difficult to see this as a sign of a changing trend — given that with the exception of China, production of gold for all the world’s major gold producers has been flat or falling.

This comes in a world with both rapid population growth and rapid income growth in many of the world’s “developing economies.” This is of huge significance to the precious metals markets because a) these economies represent the majority of the world’s population; and b) they are cultures with strong, historical attachments to precious metals. With both population growth and income growth exceeding the increase in supply of precious metals, these rare commodities are literally becoming more precious every day.

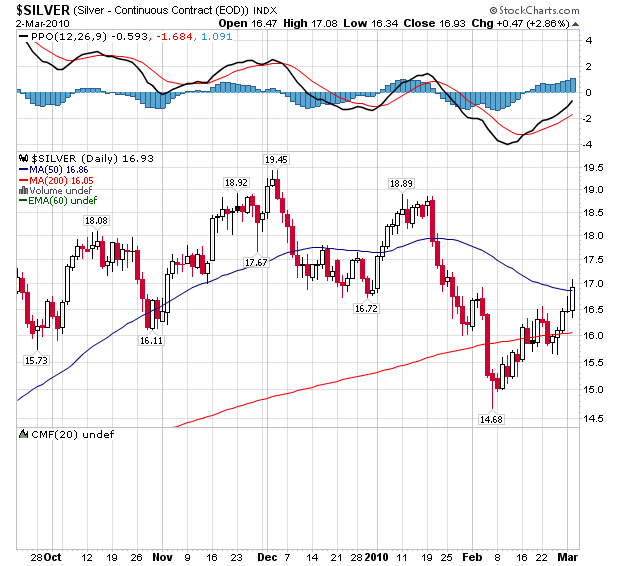

As I have also discussed, the supply/demand dynamics of the silver market are vastly different from the gold market. It is those differences that guarantee that the looming spike in the price of silver will be several multiples greater than the increase in the price of gold.

Regular readers are familiar with the key differences between the gold market and the silver market. First, silver is the world’s most versatile metal. It has been the source of more new patents than for any other metal. This has resulted in many market neanderthals mistakenly concluding that silver is an “industrial metal,” not a precious metal.

There can be no absolutely no doubt that silver is a precious metal, in every respect. It has the same malleability and aesthetic appeal of all other “precious metals,” which is why it has been widely used (equally with gold) for jewelry, and as the best “money” our species has ever devised (see “What Is Money?”. This has been the case for nearly 5,000 years.

…..read more HERE.

“Gold has been about the best investment around for the past decade,” says Eric Coffin, despite having been lukewarm towards the precious metal in the early ’90s. Co-editor along with his brother David of the HRA (Hard Rock Analyst) publications, Eric explains why they’re sticking with the exploration stories that work and how they prefer mining executives who will “swing for the fence for themselves rather than just option everything” in this exclusive interview with The Gold Report.

The Gold Report: Eric, in a recent HRA Journal you have written that you’re not expecting a big gain in the market for 2010. However, you also indicated that it’s not required to have big gains in the market to have the mining sector do well. So, as long as the markets don’t hit the panic button, you’re expecting that metal explorers will continue to be rewarded for their discoveries. Can you expand on that for us? And to what extent do you believe the metals market has decoupled from the major markets?

Eric Coffin: Well, there are indices and there are indices. We have pointed out several times in the last year that if you look at what we call the “creditor countries”—China, India, Brazil—and the “resource supplier” countries—Australia and Canada—none of those country’s bourses are technically in secular bear markets, although plenty of people assume they are. On long-term charts those markets didn’t break their 2000-2001 lows which New York and most European bourses did. We don’t think that is a minor point. It basically reinforces the story about the separation that has been going on in the world economy over the last decade, with developing high growth countries increasingly being the price setters for resources.

Metals prices, in general, are strong enough that companies making and growing real discoveries are going to get rewarded by the market, and we’ve seen that on our own HRA lists. Some of the companies aren’t getting beaten back the way people thought they would. The companies that have succeeded are making discoveries and rapidly increasing their asset values, which the market has been paying up for. We’re actually pretty pleased with the Venture Exchange Index (S&P/TSX Venture Composite Index (CDNX: ^SPCDNX)). It’s got its issues like a lack of large profitable companies to underpin it, but it’s the closest thing to a proxy for exploration stocks we can come up with. You would expect the Venture Index to be the worst performing index in a bear market but it was actually one of the best gainers in the world in 2009 in percentage terms.

Granted, the Venture Index got slaughtered in 2008. At the start of 2009 we said, “Strange as it may seem, we expect the junior market to outperform the senior ones, at least in percentage terms,” which it did to the tune of about 60%. People thought we were nuts, but if you start with the assumption that we are still in a secular commodity bull market, it makes sense that a resource stock index would have a big bounce, especially after being pummeled so badly. If you go back 10, 15 or 20 years, you could expect the Venture Index to drop by two or three times the percentage amount of the senior indices and to take much, much longer to come back.

One of the most interesting aspects of last year’s resource sector performance was that trading volumes remained strong through the year and the overall amount of financings were high. That was surprising and quite encouraging. New money was scarcer in other sectors and most major indices were plagued by light volume, even the ones with good gains themselves. Exploration is a negative cash flow business so it’s imperative that companies are able to raise money.

TGR: Let’s talk base metals. What’s your outlook on copper?

EC: Dave and I were more bullish about copper than just about anybody a year ago, but we weren’t expecting to see the price go up to $3.50 so rapidly. That was a little bit shocking. That’s a measure of demand, but it almost seems like it’s a “copper-as-money” story too. Dave has said that for years, and he’s only half joking. His point is that everybody thinks of gold as the obvious contender as a currency, but you can make a similar argument for a lot of hard asset commodities and it certainly looks like money is being parked in many metals, not just gold. Copper is an obvious choice for traders because it does high volume.

A lot of the metals are not a bad place to hide and hedge against U.S. dollar weakness, but we’ve gotten a bit cautious about base metals again partially because the relationship you’re seeing right now between pricing and inventory levels doesn’t seem to make a lot of sense. It defies logic.

TGR: Isn’t copper sending out a lot of mixed signals out there?

EC: It’s very mixed; if you look at three, or five, or ten-year copper charts, there’s a very strong inverse correlation between the copper price and warehouse inventories for copper. When copper warehouse inventories go up to a certain level, the price will start to drop and vice versa. That relationship reversed itself about the middle of last year. Copper inventories were drawn down fairly significantly from the middle of 2008 to the middle of 2009. It was part of the reason we weren’t bearish. Everybody else was on base metals. We did point out given the depth of this recession, a 500,000 tonne inventory in early 2009 was not extreme; it was well over a million tonnes at the start of the decade. The inventory fell rapidly for several months, getting down to 250,000 tonnes but then reversed again and climbed back to the 550,000 tonne level. The copper price continued to climb right along with inventory levels and has only backed off about 10% in the past couple of months. Dave and I are sitting there scratching our heads, thinking this is bizarre; the price is awfully strong given the fact that the inventories seem to be climbing fairly quickly again. Because of that we got cautious, though we are still bullish long term.

TGR: So, how do you play the copper market now given that we have all these mixed signals?

EC: We stepped back a little bit. We haven’t added any copper deals; we are looking at a few of them, and we’re hoping to add a couple more to the HRA list. But we want to see if there’s going to be more of a pullback. We were really expecting the price to come back to $2.50; it hasn’t done that and may not. Shy of that, we may add a couple of copper deals, but I think if we do, it will be deals where we see big exploration upside and we’re comfortable the market can give the company some mark-up based on discovery, not just market based on the copper price moving up and down. We tend to stick a little bit more to the exploration end, anyway. We’re recommending people just let that stuff sit for now, and if there’s really a big dump, then yes, maybe we can accumulate some. But we’re not comfortable telling people to buy producers right now. We want to see if there’s more of a drop, because although we’re not seeing inventory climb any more, we’re not seeing it come down either. As part of that process we suggested people sell First Quantum (TSX:FM), which we were up about 4000% on and take profits on Teck Resources Ltd. (NYSE:TCK) at $45, which we originally started talking about at $5.50.

TGR: Let’s talk gold. What’s your latest take on that?

EC: In the ’90s, when we were first doing the newsletter, we were only lukewarm to gold, partially because of the amount of forward hedging and gold forward sales being used as a financing vehicle by the mining sector. In the ’90s, major mining producers were moaning about how much selling there was in the gold market. Dave and I were responding with “What the hell are you talking about? You’re the sells. You’re forward selling gold left, right and center to finance mine construction.” That came to an end when gold prices got so low that it simply made no sense to start production on many projects and the low interest rate regime last decade made the forward sales less attractive relative to straight debt deals. That and the fact that gold miner’s shareholders were telling them in no uncertain terms that the idea of effectively shorting gold to finance gold production was crazy. The combination of industry de-hedging, an end to central bank sales and secular equities bear market after the Internet bubble turned things around. We thought when NASDAQ collapsed, the U.S. dollar had probably topped out for all time, and that got us a lot more bullish about gold.

It’s had a great run, and we’ve gotten a little bit more neutral about it in the last little while, but only neutral. You’re seeing a run in the dollar right now, but I think the jury is still out as to whether the dollar has actually turned around or we’re just looking at a bear market rally. There is no such thing as trading a single currency really; you always trade pairs. So if you sell the dollar what do you buy? The saving grace for the dollar is that the other high volume trading currencies (the euro and the yen) have their own issues. It’s a question of how relatively bad a particular currency is at a given time. Politically, I don’t see any way out for most of the G-7 frankly, other than printing their way out of this problem, which implies a continued race to the bottom for fiat currencies.

As long as you get a bunch of governments trying to print their way out of the problem I think that there’s going to be a place for gold in people’s portfolios. I sense that there are many, many people who are not gold bugs but who saw that gold performed very well as a safe haven. Nothing succeeds like success in the investment business and gold has been about the best investment around for the past decade. That gets noticed. Gold prices are going to be strong enough where discovery is going to get rewarded, and that is the important thing for Dave and me. I won’t be at all surprised if gold sees new highs this year— $1350, $1250, or whatever. The main question we ask ourselves is whether the price will be strong enough so that companies that make discoveries will get rewarded. As long as the price is good enough for that, we’re happy campers.

TGR: When you look at companies making a discovery, what price of gold do you use to see if it’s going to be economically viable?

EC: We tend to be a bit conservative about it. We view a mining scenario as one where you’ve got to look out 10 or 15 years, and especially when you’re looking at juniors. Let’s face it, for most of these companies, the end game is—and should be—getting taken out by a major. Finding deposits is what the juniors are good at and the best exit is often selling the discovery for a good price then moving on to try and find the next one. When you’re trying to wrap your head around the value for these companies, you’ve got to look at those companies’ potential acquirers. What are they thinking and what are they using as a base price.

I think you’re going to see M&A activity increasing because companies that have sat on the sidelines waiting for the perfect number before they bid on a company are finding out that they’re just not going to get it, and the company they’ve got their sights on, somebody else gets there first. So, I think you’re going to see improving takeover prices, and in some cases I think these majors are probably gritting their teeth and using a $900 or $950 long-term gold price to value things. A lot of them must be using that high a price at least to explain some of the recent bids.

TGR: Right. So, you’re looking for juniors who have some type of scale potential with an end-game of selling to majors. Do you have some companies that you’re following that you can share with us that fit those criteria?

EC: One company that we’re quite high on, and have been for a while, is East Asia Minerals Corporation (TSX.V:EAS). They have a series of projects in Indonesia. It’s an interesting company; they started out looking for uranium in Mongolia—Mongolia has not been the friendliest place to be for companies. Interestingly, they’re one of the few companies that really got out of Mongolia unscathed, to put it mildly. They actually sold a uranium project to AREVA (ARVCF:OTO) for $83 million and divvied up the money to their shareholders, and then moved on to Indonesia.

The guys that run it are very experienced guys out of the majors; they went into Aceh Province, which your readers may recognize as one of the areas that was hardest hit by the tsunami, and it was an area that was a real political sore point. There had been a lot of local unrest; they don’t like the guys in Jakarta very much. It seems like the tsunami just turned things around in the sense that everybody said, “You know what? We’ve got bigger things to worry about than political machinations.” These guys went in there not too long after that in 2005, 2006, and staked a lot of stuff that had been left from previous exploration companies and picked up a really great set of projects.

The one that really caught our eye—and we wrote them up last March at about 43 cents—is called Miwah. Miwah is basically a ridge that contains a large, flat-lying zone of disseminated epithermal gold. We became really interested in it because East Asia had gone in and done several kilometers, literally, of cut channel samples where they go in with diamond saws and get nice composite, very comparable samples across this large area, and the average value was over a gram. There was an Australian company in there 20 years ago that drilled a few holes and got some decent numbers, good but not great. East Asia’s theory was that there were vertical structures that carried up and were controlling a lot of the gold deposition. You would need to drill it in several directions, and it looked like the better grades would be near the top of the zone. I won’t go into more detail on the geology, but it turns out they’ve been right so far.

TGR: Wow.

EC: When we first looked at it, we got pretty excited about it, and were banging the table pretty hard with our readers on this one. A lot of them bought it, and they’re happy about it. We were the only guys following it for six months, which again, is one of those “scratch your head” situations—we couldn’t figure out why no one else seemed interested.

But East Asia has started to pick up more of an institutional following lately. They’ve added a second drill. A lot of people, including us, are going to keep prodding them to keep adding drills which I think they will do as they get more areas on the project drill ready. They expect to have enough drilling for an initial 43-101 calculation just on the ridge zone itself, probably by the middle of the year. Right now, they’re valued to 3 to 4 million ounces, and we think there’s a lot more than that; there are large prospective areas near the Miwah ridge that have not even been drilled yet.

Another one that I’ll mention is Riverstone Resources Inc. (TSX.V:RVS), which we have followed for a couple of years. It’s gone through its trials and tribulations, but really got hot in the last month and a half. All their projects are in Burkina Faso, West Africa. It’s part of the Ghanaian Shield that’s always been a great gold region. Burkina Faso seemed to have the same potential as better known countries in the region like Ghana and Mali, but for whatever reason it just didn’t seem to get any headlines.

Riverstone has been at work there for several years and has proven up a resource of about a million ounces in four separate zones on their main project, Karma. Last year, a local gold rush developed on the eastern portion of the Karma project, about four kilometers north of Riverstone’s Rambo zone. This new area, which they are calling Nami, has had thousands of artisanal miners working it, digging hundred of shafts by hand and concentrating the gold in crude sluices. Riverstone went there in December and quickly sampled 30 different shafts and 20 waste piles. The average grade of those 50 samples is 10 grams, which is amazingly high in this kind of situation. The market got pretty excited when it heard about that; the stock went from 23 cents to around 80 cents before settling back in the 60 cent range last week, with a lot of volume. They have raised some more money and have had crews sampling 200 shafts and a couple of hundred waste piles from the hand dug workings. Results should be in and compiled during the next few weeks and RVS plans to follow up immediately with a 3,000 meter drill program.

While we do not expect the actual grade to average anything like ten grams, Nami has a large enough footprint to contain a lot of ounces. The combination of that sort of potential plus the fact there should be a good flow and results for several months makes Nami a target that can hold the market’s attention. It’s the one component they have always lacked; they have good management, good projects, but there was never anything with that sort of “ooomph” to get people excited, and this seems to be that key factor.

TGR: Are there some other companies that you’re following?

EC: Mirasol Resources Ltd. (TSX.V:MRZ) is another company run by very strong professional exploration people in Argentina. We’ve always considered Argentina to be an area that is going to generate a lot of great deposits in the next 10 years. And much of Argentina is still pretty lightly explored.

Mirasol went down there several years ago and they picked up a very large land package and a very strong one. They are project developers; their forte is applying geological models to areas that have seen very little work. They really get going on large structures and geology. They focus on the very basic, early stage work to see if they can generate discoveries. And then, they winnow things down. They have 30 or 40 projects in early development at any given time. They have made several quite high-grade silver vein discoveries; one of those discoveries, the Joaquin Project, was optioned to Coeur d’Alene Mines Corporation (NYSE:CDE).

Coeur d’Alene started drilling Joaquin in 2008. They did another program last year and got some quite strong results towards the end of it. We wrote them up in the early fall because of the combination of good early drill results at Joaquin that were about to be followed up on and a strong project pipeline, giving them real discovery potential. Coeur D’Alene started drilling again in October and released some pretty spectacular numbers in November. The first set of drill holes that Coeur put out—the best hole was a ridiculous number. It was around 25 meters with 1,100 grams.

So far, MRZ has stuck to their knitting, being a project developer and a project generator, and Dave and I tend to prefer guys who will swing for the fence for themselves rather than just option everything. One thing that was holding them back—and rightly so—was the market wasn’t that great. They’ve made another high-grade discovery on a nearby property that looks like it’s very similar to this and they, in fact, have several other properties that have strong potential. Again, this really got the market’s attention; this stock was 50 cents when we wrote it up and it’s trading now at about $2.70.

TGR: Any others?

EC: I’ll update a couple of the other companies we talked about last time. Evolving Gold (TSX.V:EVG, FSE:EV7) drilled a large number of good holes at its Rattlesnake Hills project in Wyoming. The company will report an initial gold resource this spring and will be back as soon as weather allows with a big follow-up drill program and all the zones remain open. EVG also just reported a high-grade discovery hole from its Carlin project in Nevada. Follow-up drilling is required but it looks like the company may have another important discovery on its hands.

Underworld Resources Ltd. (TSX.V:UW) also had a lot of drilling success at its White Gold project in the Yukon. They reported an initial resource estimate of 1.4 million ounces for White Gold, close to what we expected. They too will be busy again this year. Several of the zones remain open and there are some good targets on the main project and in the regional area still to be tested. We are following another company in the area as well and will be watching it closely.

Minefinders Corporation (TSX:MFL, NYSE.A:MFN) continues to see improvement as it brings the Dolores project up to its full commercial production level. Cash costs have been dropping and the company is now stripping and starting to mine a higher-grade area of the deposit so the numbers should continue to improve. They will also be working on a preliminary economic study of adding a full mill to the project. We are very interested to see how that turns out since we have always liked the deeper high-grade zones at Dolores. Higher-grade zones are the main beneficiary when a sulphide milling system that has higher recoveries is added and the deeper zones at Dolores are still open to expansion. We’ve been watching to see how the recoveries come in on the heap leach operation and they do seem to be still improving.

One important aspect to heap leach operations that traders need to be aware of is that it takes two or three or even four quarters to get to steady state production levels and really see what the recoveries percentages are for gold and silver with this type of mining. MFL also has a couple of exploration projects they have been assembling for the past few years and once Dolores is generating the cash flows projected for it, we would not be surprised to see Minefinders on the hunt for acquisitions.

TGR: Great, thanks Eric. Lastly, we understand that you have a new free report to offer our Gold Report subscribers, as well as an HRA subscription deal. Can you please let us know the details?

EC: Yes, we have just put together an extensive report for your readers, which highlight some of the companies that I mentioned above, plus a few others that we think have significant potential for 2010. It also showcases the power of the Alert service, which we think has been particularly valuable for subscribers since it allows them to quickly get our input and opinion when important, trend-changing results are released.

Simply go to: www.hraadvisory.com/aureport.html for all the details on this offer. If you enter your valid email address on that page we will immediately send you our latest special report for free. Also, we’re offering savings of up to $1000 off HRA Alert subscription rates until March 15th! For more details on these different HRA services, please go to: www.hraadvisory.com/subscriptions.html.

Remember, to receive the special discount, use the ‘subscribe’ links in the following jump page only: www.hraadvisory.com/aureport.html. The 20% off pricing cannot be accessed via our website.

TGR: Eric, we appreciate your time.

Eric Coffin and his brother David are the co-editors of the HRA (Hard Rock Analyst) family of publications. David is the “rocks side” of HRA, and has been active in mining exploration for over 30 years in roles spanning prospecting through feasibility studies, and now markets commentary. Responsible for the “financial analysis” side of HRA, Eric has a degree in Corporate and Investment Finance. He has extensive experience in merger and acquisitions and small company financing and promotion. For many years he tracked the financial performance and funding of all exchange listed Canadian mining companies and has helped with the formation of several successful exploration ventures.

Eric was one of the first analysts (along with David) to point out the disastrous effects of gold hedging and gold loan capital financing (1997) and to predict the start of the current secular bull market in commodities based on the movement of the U.S. dollar (2001) and the acceleration of growth in Asia and India.

David logs, literally, hundreds of thousands of miles every year, visiting exploration sites on six continents in order to bring back the real goods for HRA subscribers. Eric and David can be reached at hra@publishers-mgmt.com or through their website at www.hraadvisory.com.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair