Daily Updates

John Kaiser: PDAC-Too Much of a Good Thing?

Perhaps something akin to prospectors rushing from around the world in the grips of gold fever to California in the middle of the 19th century, thousands flock to the annual PDAC (Prospectors & Developers Association of Canada International Trade Show & Investors Exchange) to pan for nuggets for their organizations or for themselves. For this exclusive interview, The Gold Report caught up with Kaiser Bottom-Fish Report editor John Kaiser on the last day of the 2010 PDAC last week in Toronto. John finds that the bigger the event gets, the more patience and effort it seems to take, but those who are persistent and willing to dig can still cart away useful information and insights. Read on as he shares his takeaways.

The Gold Report: You’re a long-time participant in the annual PDAC convention. Everybody who wasn’t able to be there wants to know about any compelling stories or particularly interesting tidbits that you learned this year, when the event brought people into Toronto from more than 100 countries around the world.

John Kaiser: In the past few of the 20 years I’ve been going to this conference—and this year is no exception—it has become increasing difficult to pick up any prominent buzz, be it about a sector being red hot or be it about a major new discovery.

TGR: Why do you suppose that’s happening?

JK: The reason is simple; this conference has become so big, so global. What in 1994 would have been the big Voisey’s Bay’s buzz that everybody was talking about or Bre-X in the following year, even if something like this did come along now, the collective size of 400 companies exhibiting would dwarf it. There are several hundred trade show exhibitors; numerous talks covering everything from country-focused issues to deposit models to new discoveries and so on. It’s very difficult for any single thing to stick out.

Even worse, because it is now so large and dispersed, you do not have that intensity of networking of the past, the random networking where you would bump into people you hadn’t seen for a long time and hear about this or that. By the end of the conference you had all these bits and pieces gelling in your head and you could say, “Oh, yeah, this was what was interesting.” No, now it’s the more you know in advance what you’re looking for; you make the sessions; you track down those companies, and you have the face-to-face you planned with these. So, the old aspect of serendipity of bumping into stuff and stuff floating to the surface just does not happen in this environment.

TGR: Did you have any specific goals for your newsletter or your personal business that you were able to accomplish at the conference?

JK: I always take in the commodity talks on Sunday. This year I found that very helpful, and one theme that did emerge is the growing role of hard assets as a target for managed money. Martin Murenbeeld (Commodities and Market Outlook, Gold/Silver; DundeeWealth Economics) emphasized that $40 trillion of about $117 trillion worth of financial assets in the world is so-called managed money. In other words, fund managers are running it. Of this $40 trillion, about $200 billion is in what you would call hard assets such as gold, silver, copper, ETFs, futures; these sorts of instruments linked to raw materials. Martin suggests that the trend is going from this relatively small sum to nearly $1.3 trillion; in other words, 3% of the managed money going into this category. Should this happen, there’s nowhere near enough gold at the current prices.

In another talk on copper, a similar theme was raised. When you look at a 50-year chart, copper has historically followed this pattern when inventories in the warehouses build up—which is usually during a business cycle downturn such as we’ve just been in—the price of the commodity collapses along with it until all the inventories have been drawn down. And then they spike upwards.

After the spike downwards in 2008, copper prices are back almost where they were before the collapse. Warehouse levels—while not as bad as they were at the end of the ’90s when inventories were very high and copper was at 60 cents—are about halfway there. Yet we have the higher inventories and higher prices tracking each other. The analysts are attributing this to the movement of investor capital into these hard assets that Martin was talking about, and they say that the inventories aren’t just stuff parked in the warehouse because there’s nobody to buy it. Instead, it’s already allocated to investors speculating on higher prices down the road or even treating it as a hedge against a debasement of the currencies and so on.

TGR: So we’re seeing that kind of growth not just in the precious metals space, but also in base metals. Did anybody address the idea of that kind of big money investment or fund investment in other metals besides even just base metals and gold?

JK: Yes, for example, nickel is really not supposed to be back at $9 because the old pig-iron nickel, which helped bring nickel back down from the $22 levels, was working at $11 and $12. Now they’re able to make it work at $7 and $8, so there’s plenty of nickel supply coming into the system. Still, nickel has managed to climb back to $9, while inventories are very, very healthy.

TGR: So it’s affecting copper, nickel and gold.

JK: We are seeing it in all the categories. Even zinc, which is in surplus this year and is supposed to say in surplus next year, but then is expected to go into deficit. At that point, suddenly demand is greater than the supply. It is a $1 or higher and has bounced back significantly from the low reached during the 2008 meltdown.

TGR: Did you observe a lot of activity at the conference that you hadn’t seen before, with fund managers sniffing around for compelling plays to work in what you’re basically describing as a groundswell of money being diverted into these hard assets?

JK: I polled exhibitors as to what kind of traffic they were getting, and yes, they are receiving a lot of inquiries. They’re coming from a range of sources, from the traditional European and North American institutional fund managers to a lot of overseas Asian-style managers. Of course, there’s also interest from the end-user crowd.

A big theme has been China’s movement to convert some of its foreign reserves into hard assets in terms of ownership of physical deposits. That’s why we have seen buyouts and significant investments or large equity stakes in a number of important projects stranded during the 2008 meltdown. That was the nature of feedback I got from exhibitors.

TGR: Do you then anticipate more of the global relationships blossoming and developing as we saw last year with a major Asian investor—actually Japanese rather than Chinese—coming in as a strategic partner with a North American company?

JK: You’re referring to the deal between Copper Mountain Mining Corp. (TSX:CUM) and Mitsubishi Materials Corporation (PS:MIMTF). Yes, more of that sort of thing, but really it all hinges on what happens in global economic trends.

There was no irrational exuberance at all at this conference. In fact, it’s a bit like a teeter-totter poised to go either way. There is hope that China will pull the global economy back on track and reinvigorate Europe and the United States. On the other hand, there also is concern that this will fall apart, and that as the fiscal stimulus packages come to an end interest rates start to rise that we will see a double dip recession in the North American markets. And if that happens to coincide with a problem in China, which has been going hell-bent at an incredible pace thanks to its $585 billion fiscal stimulus program, there is concern that his could end very badly.

So we are almost in the eye of a hurricane, and everybody’s wondering where we will be next year.

TGR: Which way are you leaning?

JK: My own feeling is that if we come out of this with the global economy back on track and the disparate signs of life that we see in the North American economy are actually more than just flickers, next year we should see the supercycle that dominated the talk at this conference from ’03 to ’08. This time it will be taken seriously, and massive amounts of money will flow into the sector. But as I say, it all hinges now on where the global economy goes.

TGR: In that context, it’s interesting to see a lot of the money still going into the hard assets as we wait for the global economy to recover.

JK: We may have to stumble for a couple of years; in which case commodity prices will sag. But if that happens, all the talk about fiscal austerity and so on will go out the window. Every nation in the world will start to print money to reflate their economy and through brute force get liquidity in the economy going again.

And when that happens, because of the conservatism that on the mining side—the supply response—there is now money ahead of that curve saying, “Okay, we don’t really need to buy copper right now. We need to buy a copper development story and put up the capital and give them the money to push it closer to the feasibility stage. Then, when we have greater clarity on the direction of the economy, we plunk down the billion dollars or whatever is needed to put this asset into production.”

That’s actually a very bullish sign for the companies exhibiting at the conference because it’s a shift away from just, say, buying physical gold to buying the ounce-in-the-ground companies. Pierre Lassonde (Franco-Nevada Corporation (TSX:FNV), in his talk (“Is $1,000 gold sugar coating Peak Gold?”) had an interesting chart that plotted the average cost per ounce, which had been rising steadily for the past two decades. But in the last year, that cost per ounce flattened even as the price per ounce of gold went up significantly. Now, what he’s saying is that a real margin is reappearing. It’s not as if the companies are finding higher-grade deposits; they are not. They have simply been able to contain costs in the aftermath of this meltdown.

TGR: What made that possible?

JK: This meltdown was very different from past economic busts because the industry had spent the entire cycle worrying that this would happen. As a result, when it finally did happen, their supply response was immediate. They cut marginal operations; they laid off people; they stopped it on a dime. This has made the cost structure quite robust, and the producers are set to benefit significantly if the metal prices stay where they are and/or perhaps go even higher.

For investors seeking larger returns, these development projects look quite good at these current prices in terms of ounces or pounds in the ground, but the companies are not reflecting valuations that take these prices seriously. These types of projects are attracting capital on the basis of speculation that today’s higher commodity prices stay and go higher in the long run.

TGR: Bargain shopping.

JK: In a sense, but it’s speculative bargain shopping. It’s speculating that your particular Beanie Baby that is cheap now is going to be very dear three or four years from now.

TGR: That takes us back to what, the ’90s? Back to the future now, what else caught your eye at the PDAC this year?

JK: I was checking out the rare earth space. Quite a few of the rare earth companies were represented, there were several rare earth receptions and a whole morning devoted to talks about the rare earth deposits, geology, market and so on. These were surprisingly well attended for a Wednesday morning, when traditionally 90% of the delegates are still in bed. So that is actually a pretty good indicator of the interest in this space.

Particularly with the assistance of one of the stocks listed going up during the days of the conference, I would say that the rare earth space is probably on the threshold of achieving a whole new level of serious attention from investors.

TGR: Any companies in that space that you find particularly interesting?

JK: The interest has been a lot of talk and a lot of tire-kicking, but not really a lot of money going into the treasury. This may change in the not-too-distant future, though.

TGR: How so?

JK: I had an interesting meeting with a representative of Molycorp Minerals, who explained their timeline of activities. If I understand it correctly, we could see a Molycorp IPO before the summer. What the institutional market is missing in the rare earth sector is a vehicle large enough for serious investments. There has been incredible media buzz about the rare earth space. The Chinese are very clearly interested in seeing rare earth deposits developed outside of China to take the pressure off them to export what they consider a resource they need to hoard for the long term.

Having said that, nobody wants to buy stocks such as Quest Uranium Corporation (TSX.V:QUC) or Avalon Rare Metals Inc. (TSX:AVL) to any large degree. With these smaller players, there are so many uncertainties about whether the feasibility study will indicate a profit margin, whether they’ll ever get a permit to get to production, or whether the metallurgical process actually will work. An aversion to investing in these very risky single-asset projects has inhibited the serious money coming into these plays. If a major company such as Molycorp does an IPO and lists on the New York Stock Exchange, though, it will validate the space and pull a lot of money into all the smaller companies. So I sense the timeliness for this improving over the next two or three months.

TGR: Do you see any other companies besides Molycorp with an asset base that could actually pull off something as significant as an IPO and list a rare earth play on the New York or Toronto Exchange?

JK: A counterpart is Lynas Corporation (ASE:LYC), listed on the Australian Stock Exchange. This company has a market cap of AU$815 million, and last year raised AU$450 million basically from institutional investors around the world after the Australian Foreign Investment Review Board said no to a Chinese proposal to put up debt and equity financing in exchange for majority control of Lynas. So this has already happened in Australia, but that market is not as liquid and popular as, say, the New York Stock Exchange.

I wouldn’t be surprised if Lynas Corp. also seeks a New York Stock Exchange listing; however, the significance of Molycorp is that this is a home-grown, American deposit, and on April 1, we’re supposed to hear the results of the RESTART bill proposal, an analysis of what America’s vulnerabilities are to rare earth supply. If they decide that we have a problem here, the intensity of the hand-wringing about what to do about it would increase and companies such as Molycorp will receive a lot of attention as at least a major part of the solution to the problem. As you may know, Molycorp has been in the process of getting its Mountain Pass deposit back into production, and it also has the ability and the knowledge base necessary to acquire other projects elsewhere in the world to beef up its rare earth supply potential.

TGR: Thank you, John. You’d also mentioned RESTART in a conversation with our sister newsletter, The Energy Report, a couple of months ago. We recently saw a news release about this, and for readers who aren’t familiar with it, RESTART stands for “Rare Earth Supply-chain Technology and Resources Transformation.” Proposed as a means of reviving a competitive rare earths industry in the U.S., it has been put forward as potential legislation by an organization known as USMMA, the United States Magnet Materials Association. USMMA reported submitting this proposal, designed to create a path forward toward “a ‘whole-of-government’ approach to resolving the Rare Earth Elements (REE) supply crisis,” to a number of federal entities—the U.S. Department of Commerce, U.S. Department Energy, U.S. Department State, U.S. Department of Defense, Office of the U.S. Trade Representative, and Office of Science and Technology Policy within the Executive Office of the President. The RESTART proposal calls for up to $1.2 billion in funding to reestablish domestic rare earth mining as well as U.S. facilities for refining, alloying, melting and production of rare earths and rare earth-based products.

USMMA said that it has already successfully advocated for inclusion of a congressionally mandated study of the rare earth supply-chain in the FY10 National Defense Authorization Act. The organization was founded by three high-performance magnet producers and suppliers in 2006: Thomas & Skinner, Inc. (Indianapolis, IN), Hoosier Magnetics (Ogdensburg, NY) and Electron Energy Corporation (Landisville, PA) in 2006. U.S. Rare Earths, Inc. (a private company) joined the group in 2009.

John Kaiser, a mining analyst with 25-plus years of experience, produces the Kaiser Bottom-Fish Report. It specializes in high-risk Canadian resource sector securities and seeks to provide investors with a framework for intelligent speculation. His investment approach integrates his “bottom-fishing strategy” with his “rational speculation model.” After graduating from the University of British Columbia in 1982, John joined Continental Carlisle Douglas, a Vancouver brokerage firm that specialized in Vancouver Stock Exchange listed securities, as a research assistant. Six years later, he moved to Pacific International Securities as research director and also became a registered investment adviser. Not long after moving to the U.S. with his family in 1994, John cast his own line in the water, so to speak, with publication of the premier edition of the Kaiser Bottom-Fish Report.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

Michael Lewis’ new book about the subprime scandal, “The Big Short,” is a fascinating, edge-of-the-seat read.

But for everyone trying to manage their own finances these days, it’s also a gold mine of valuable insights about how the modern economy really functions — and what you need to watch out for.

Among the takeaways:

1. Never, ever invest in something you don’t fully understand. Ever.

There are no exceptions to this rule. Simple, really. But it never ceases to amaze me how many people are still tempted to break it. Like all the top Wall Street bankers who were willing to bet blindly on subprime paper they didn’t understand. Many banks were still buying the stuff in late spring 2007, when the fundamentals were already in freefall. With complex investments, it’s hard know when to get in or get out. This never seems to happen when you invest in, say, a beer company.

…..read more HERE.

“Chanos says his shorting strategy for China would be to choose a copper mining company that exports 80% to China”

“Short the China Bubble” Trend Is Spreading

A China Bear trend, which got its start when Wall Street hedge fund manager and confirmed short seller James Chanos began dropping bubblish sentiments about the country, is spreading internationally.

Chanos has been saying since January that China’s booming house market has become a bubble supported largely by speculative money. One of his assumptions is that China’s urbanization has not come up to expectations. Although Chanos has also said that, “China is the engine of growth that will hopefully pull us out of the morass that we find ourselves in,” he has stuck to his point that China’s house market has been crazy, calling it a “classic pocket…of overheating and overindulgence.”

Chanos, renowned for his correct calling of the Enron debacle and the tons of money he made on it through his Kynikos Associates, has long been regarded as the most astute short seller on Wall Street.

The China-skeptic voice has long been around. Predictions of the “Technical Bankruptcy of Chinese State-Owned Banks” struck up in 2002, when China commenced its banking sector reform. Since then, such voices have been heard over China’s over-reliance on exports, the imbalance between investment and saving, its dependence on external energy resources, and a list of other issues.

Now the noise has found China’s house market to focus on, along with the government’s debt and the yuan exchange rate.

James Richards, once the general advisor for Long Term Capital Management, a massively busted hedge fund, said at a March 15 conference in Hong Kong that China is riding on the “biggest bubble” in history, which is just waiting to burst. Richards, now the general manager of Omnis Inc., a market intelligence firm, holds that, except for short term speculation, China does not deserve any investment. He said the balance sheet of China’s central bank, the People’s Bank of China, looks very much like a fund long on the US dollar and shorting renminbi.

Richards has just joined the legion of China-shorters, which includes Harvard University economics professor and former chief economist of the International Monetary Fund Kenneth Rogoff, who warn that China is at the risk of economic catastrophe.

Rogoff said in January that China’s growth rate could decline to 2% within the decade due to an “economic bubble caused by excessive lending.”

Marc Faber, an independent analyst and one who reportedly predicted the Asian Financial Crisis, has been bullish on China’s real estate market but warns of the possible bubble burst.

And the shorting voices extend far beyond the real estate sector. Victor Shih, a professor of Chinese Politics & Political Economy at Northwestern University, says in a report that between 2004 to 2009, the government debt from investment was 11 trillion yuan, (about US$1.6 trillion), double the estimation by official statistics of 5-6 trillion yuan, accounting for one third of China’s GDP and about 70% of China’s foreign exchange reserves. He estimated that total government debt may be as high as 96% of GDP. In a worst case scenario, Shih says a financial crisis may break out as soon as 2012.

Although many China analysts doubt the credibility of Shih’s estimation, there are open ears on Wall Street

On the other side of the hubbub is Jim O’Neill, Goldman Sachs chief economist, with new data on the RMB exchange rate. According to his March 3 report, GS’s model, dubbed GSDEER (Goldman Sachs Dynamic Equilibrium Exchange Rate), shows that RMB had been undervalued but is now close to purchasing power parity. GS appears to be an outlier against the international chorus pushing the yuan’s appreciation. O’Neil makes his case in three ways: since 2005, the trade weighted, effective real exchange rate has risen by 20%, largely eliminating RMB’s under valuation; China’s imports are increasing and its trade surplus is shrinking; and RMB’s purchase power at home has been undermined by inflation.

In another report, The Fair Value of BRIC’s Currencies, GS says that the real, Brazil’s currency, is one of the most over-valued currencies among the emerging economies, while the fair value of RMB has appreciated most since 2000 among the BRIC countries.

Attacking the soundness of China’s economic sectors such as real estate is not the end of it. In late 2009, Pivot Capital Management, a hedge fund company registered in Monaco, doubted the fundamental health of the Chinese economy.

Its report, China’s Investment Boom: The Great Leap into the Unknown, based on data from the 12-year investment cycle since 1998, analyzed the production capacity and demand in the infrastructure construction, manufacturing, and real estate sectors. The report concludes that China’s investment driven growth is inefficient and unsustainable, and predicted that the government-dominated lending and investment model will collapse in 2010.

The report also compares the ratio of general fixed capital formation (GFCF) to GDP, finding that in China it far overtook those of other Asian countries during the investment boom in mid 1990s. It says a ratio of GFCF to real GDP reveals that the effectiveness of China’s lending-driven growth is quickly diminishing. Between 2000 and 2008, for every US$1 of growth, US$1.50 of lending was needed, and the ratio deteriorated to $1 to $7 in 2009. Loans pouring into real estate and stock speculation gave the real economy only a very limited boost.

It also states that the potential of urbanization to growth may be illusory. In China’s Yangzi and Pearl River Deltas, and in the Bohai bay area, villages are virtually eliminated. According to the report, China’s rate of urbanization has been underestimated by 20%, indicating that the population in the line of being urbanized is in fact about 100 million, instead of 350 million as long expected. So, it says, China is sliding towards a hard landing and sending as strong a shock wave through the world economy as the US subprime crisis.

Pivot Capital Management has earned some little reputation by monitoring possible troubles in Spain, Portugal, Italy, Greece, the Baltic countries, Hungary, and Poland. It had made handsome profits by investing in government bonds and CDSs (credit default swaps) related to Greece, Portugal, and Iceland.

James Chanos says his shorting strategy for China would be to choose a copper mining company that exports 80% to China, digging out the companies liquidity and financial soundness, and “getting involved at the early stage,” as most successful investors do.

In a financial market of 10,000 participants, a stock that is collectively believed about to surge soon would be bound to surge since the 10,000 speculators would all buy it. But the sun will never rise from the west even if 6 billion people on earth believe so. Who knows?

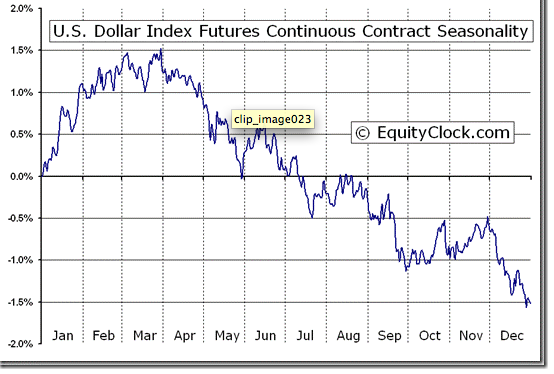

The U.S. Dollar has a history of peaking in March and moving lower until at least June. Is history about to repeat?

Seasonal influences

A 20 year seasonality study recently completed by EquityClock.com shows that the U.S. Dollar tends to move higher in January and February, peaks in March and trends lower until at least the beginning of June.

Chart courtesy of www.equityclock.com

Technical influences

The U.S. Dollar Index currently has a deteriorating technical profile. The Index reached an intermediate peak on February 19th at 81.34. Short term momentum indictors including Moving Average Convergence Divergence and Relative Strength Index have rolled over from overbought levels and continue to trend lower. Intermediate downside risk is to the top of a previous trading range at 78.45.

Fundamental influences

The U.S. Dollar is expected to remain under pressure until at least June this year due to a series of political and economic events:

- The financial crisis in Greece is close to resolution. Greece’s political leaders know that a resolution must be reached shortly in order to avoid default on its sovereign debt. Meetings later this week will determine whether resolution is achieved through the International Monetary Fund or through European finance ministers. A resolution will strengthen the Euro and weaken the U.S. Dollar.

- Recent actions by members of the U.S. Congress against China potentially could lead to an international trade and finance crisis later this year. Last Monday a group of 130 Democrat and Republic lawmakers petitioned Treasury Secretary Timothy Geithner to brand China a “currency manipulator” when he releases a report on the subject in April. The lawmakers are saying that the Chinese are in effect subsidizing exports by maintaining a low value of the Chinese currency relative to the U.S. Dollar. Under legislation proposed by lawmakers the Treasury Department is required to indentify countries with “fundamentally misaligned currencies” and to issue a “priority action” against them. Countries on the “priority” list could face a range of U.S. responses including a revision to dumping calculations, a halt in government purchases of goods and services and a restriction on trade finance and insurance. A prominent U.S. media spokesman said last week that the actions by Congressional members are equivalent to “poking a stick in the eye of your banker”. The lawmakers seemed to have forgotten that China is the largest holder of U.S. Treasury securities and, until late last year were the largest purchaser of Treasury issues used to finance the U.S. government’s mounting budget deficit. China owns more than $700 billion of U.S. Treasury securities. The Chinese already are responding to a growing protectionist stance taken by Congress. The February Treasury International Capital Systems (TICs) report released last week revealed that China was a net seller of U.S. Treasuries for the third consecutive month. Relations between China and the U.S. have deteriorating significantly in recent weeks due to a series of issues including the U.S. sale of weapons to Taiwan, the threat to Google’s presence in China and cyber attacks reportedly initiated in China. Chinese efforts to liquidate even a small portion of their Treasury securities could place significant downside pressure on the U.S. Dollar.

- A decision by the Federal Reserve last week to maintain a low interest rate policy rather than to protect the U.S. Dollar with a policy of slightly higher interest rates also adds to downside pressure on the U.S. Dollar

What to do

The U.S. Dollar is following its seasonal pattern once again. Preferred strategy is to avoid investments in U.S. Dollars unless fully hedged. Commodities priced in U.S. Dollars will see higher prices under this scenario. Basic material and energy securities will outperform as the U.S. Dollar moves lower.

Don Vialoux has 37 years of experience in the Investment Industry. He is a past president of the Canadian Society of Technical Analysts (www.csta.org) and a former technical analyst at RBC Investments. Don earned his Chartered Market Technician (CMT) designation from the Market Technician Association in 1995. His CMT paper entitled “Seasonality in Canadian Equity Markets” was published in the Spring-Summer 1996 edition of the MTA Journal. Don also has extensive experience with Exchange Traded Funds (also know as Index Participation Units) as well as conservative option strategies. In 1990 he wrote a report that was released in the International Federation of Technical Analyst Journal entitled “Profiting from a Combination of Technical and Fundamental Analysis”. The report introduced ” The Eight Phases of the Stock Market Cycle”, an investment concept that continues to identify profitable entry and exit points for North American equity markets. He is currently a member of the Toronto Society of Fundamental Analyst’s Derivatives Committee. Now he is the author of a daily letter on equity markets available free on the internet. The reports can be accessed daily right here at www.dvtechtalk.com.

Waiting for the Next Inflection Point

What are the pros doing?

I’ve been speaking with various institutional investors, and I can tell you there is little in the way of uniformity of thought. Here we are, up 70% or so from the lows of over a year ago, and there is no consensus — which is probably a good thing.

What are they thinking about? The health care bill, financial reform, the federal deficit, tax policy, a bubble in china, hyper-inflation, structural unemployment, another lost decade, and even demographics, their concerns are many and varied.

Their investment postures are even more varied. I can oversimplify them into one of five buckets

1) All In: They caught the bottom, or jumped in not much after it. They have been long and strong the whole run. They see no end in sight. Some are leveraged, some used options. My estimate: About 10% of pros fall into this camp.

2) Not-Too-Late: They joined the party later in the rally, and are still carrying some cash (10-20%) but not excessive amounts. They are not sure why we have been going higher, but feel they must participate. (About 20% of pros)

3) Reluctantly, Partially Invested: The group that originally fought the rally, but honored their stop loss discipline to flip from short to long around June of last year (after the pullback reversed). They are a combination of Global Macro traders and Long/Short funds who hate this environment, along with Trend followers who don’t want to fight the tape. They are carrying too much cash — from 20% to as much as 50%. Many are looking for the next opportunity to get short. (About 30%)

4) Bought It, Sold It, Waiting for Clarity: This group had a very good 2009, but did not want to overstay their welcome. They hit the bid near year end, and took huge performance fees. They moved aggressively to cash – 50%+ — and have dabbled on the short side. They are waiting for the next inflection point to redeploy capital in either direction. (~20%)

5) Missed it Totally, Waiting for Vindication: The “structural economic problems” and “Unconscionable Federal Reserve actions” have kept this group out of the markets. They are awaiting the next leg down, a retest of the lows, and then a break even lower. They are well stocked with Puts, bottled water, and MREs. This was a bigger cohort, but investor pressure and stress have reduced their numbers. (Down to less than 5% of hedge funds)

That’s about 85%, as there are others who simply don’t fall neatly into one of these buckets.

About The Big Picture

This site is written by and for investment professionals, as well as anyone else interested in investing, markets, and the economy. We key in on what you should — and more importantly, what you should not — do with your money. I have been writing about these topics for ~15 years, and blogging since 2003.

By sheer accident, it has become one of the best reviewed finance blogs on the web.

The writing is designed to be very accessible — no PHD required. Hell, no college degree is required. If I can make this stuff understandable to my right brain art teacher wife and my 74 year old retired real estate agent mom, then I can help you learn the basics of markets, investing and the economy.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair