Daily Updates

Poor people and countries suffer most in global recessions. The Economist this month runs with an excellent article on the catalysts for growing unrest in China, some highlights:Poor people and countries suffer most in global recessions. The Economist this month runs with an excellent article on the catalysts for growing unrest in China, some highlights:

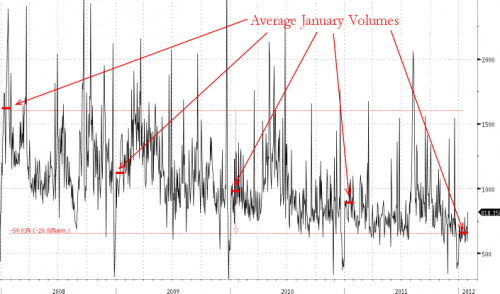

Presented with little comment except to say that the total lack of volume (and massive concentration of what volume there is at the close) is hardly reflective of a market that is anything other than broken and dying. Last January (2011) the average number of stocks traded on the NYSE per day was 891mm shares vs 661mm for this January (a 26% drop YoY!) and this is down an incredible 59% from January 2008.

January 31/2012: The final days of January saw the Dow down four out of the last five trading sessions. The sheer size of this still-forming top is scary. I think this top will be followed by a phenomenon known as the Kondratief bear cycle, a cycle that can endure for as long as 20 years. The other name for it is the nuclear winter, a rare and dangerous phenomenon that can last for a generation.

As we end the month it is notable that Lowry’s Selling Pressure Index (supply) is still substantially above their Buying Power Index (demand).

Joe Granville’s on-balace-volume statistics remain bearish, and Joe warns of years or bearish markets ahead.

In fact, Joe’s OBV figures are so negative that I called Joe on the phone today to ask him if his figures were for real. He told me that he expects the Dow to fall 4,000 points from here when this top breaks down. And no, Joe was not kidding.

Because the Dow was down on four days out of five sessions last week a corrective rally may be expected this week, but watch the volume. Whether volume increases on a rally tells us a lot about the strength or weakness of the market.

From the fundamental side, the yield on the Dow is down to a mini 2.52%, meaning that the Dow is way overpriced and way overvalued. Remember, the essence of Dow Theory is VALUES

Other article by Richard Russell:

Move Into Gold (Janary 11/2012

Sage Advice (December 13th/2011)

Red Alert (November 25th/2011) (via Michael Campbell)

About Richard Russell, author of the world’s longest-running investment letter, Dow Theory Letters went bullish on Gold below $300 in 2002, has stayed bullish and remains L/T bullish to this day:

Richard Russell has made his subscribers fortunes. One of the best values anywhere in the financial world at only a $300 subscription to get his DAILY report for a year. Go HERE to subscribe.

The Directional Change on January 23rd showed gold was moving to the upside. However, it is just a lot of noise until the previous month’s high of 1769.40 is exceeded. Volatility should continue but gold MUST close above 1755 on January 31st to signal a possible rally into February.

Martin Armstrong will appear live from Princeton, New Jersey at the World Outlook Conference, February 10, 11 to discuss his latest forecast for the Stock Markets, Gold and other markets. For tickets click on the World Outlook button at the top or HERE

I’d like to tell you about a study I read recently.

It’s a slim little booklet titled One-Way Pockets by Don Guyon (a pen name for a broker). The book, which was first published in 1917, covers some studies he did on the trading behavior of accounts at the time. What he found was timeless.

The language is charmingly stuck in the World War I era. “At the fag-end of the never-to-be-forgotten ‘war brides’ market,” he begins, “I began, in a casual sort of way, to analyze the accounts of half a dozen of the firm’s most active traders.”

During the “war brides” market of 1914-15, defense stocks and industrials surged in response to the outbreak of World War I. [Editor’s note: “War bride” was a nickname for what we now call “defense stocks.”] But Guyon found that even though such stocks had already made large moves up, his firm’s clients had big stakes in them with small profits. This was not a unique circumstance. Guyon found that this was the way the top of every bull market looked, in his experience in the brokerage business. In 1917, there was a bear market, and these traders lost money.

Why?

This is where Guyon’s studies yield a few interesting results.

He looked at five leading stocks these accounts traded: United States Steel, Crucible Steel, Baldwin Locomotive, Studebaker Corp. and Westinghouse Electric. He analyzed the buy and sell decisions on each account and summed them up.

What he found was amazing. All of these stocks scored large gains during the war brides market. Yet “the average price at which each stock was bought for the six accounts was higher than the average price at which it was sold.”

Clearly, people bought them mostly after they had already gone up a bunch. Then they sold them when they fell.

Guyon did another study in which he looked at the order books of his firm’s accounts, plotting the buys and sells day by day from March 1916 to March 1917. A similar pattern emerged. The traders would buy a stock after the stock had risen. They would sell into declines. As Guyon wrote:

This analysis of transactions affords corroborative evidence of the same general trading faults that were revealed in the six accounts previously reviewed. Once again, the public sold too soon, repurchased at higher figures, bought more after the market had turned and, finally, liquidated on the breaks.

Tips, rumors, news — all these things Guyon thought only confused investors, pushing them to make emotional and ill-timed decisions. Guyon’s trading advice later in the book is not so useful, but the main point of his studies stands the test of time. The main point is simply that “the great majority of speculators are…consistent losers in Wall Street.”

Much of this reaffirms what is always true in the stock market. People chase price moves, rather than buy and hold (and sell) based on careful consideration of what they own.

People are also, everywhere, impatient. It makes me think of an old Far Side comic with two vultures sitting on a tree. If memory serves, one says to the other, “Patience, my ass! Let’s go kill something!”

Most people are like that vulture. They can’t wait. They need to “do something.” But as One-Way Pockets shows, “doing something” is often the wrong thing to do. Patience is better.

There are plenty of modern studies that find the same results as Don Guyon. Similar studies, yet more comprehensive, show how increased frequency of trading leads to poorer results relative to accounts with less activity. Other studies affirm that investors don’t even earn the stated returns on their mutual funds, because they take money out after it has done poorly (and the price is low), and add money when it has done well (and the price is high).

This is counter to all the good advice that is out there about investing from such greats as Warren Buffett, Peter Lynch, Seth Klarman, Martin Whitman and others who preach the virtues of buying cheap and holding on. It’s all out there, and you can acquire a first-class education about good investing for very little money. Yet, as Guyon writes, “These venerable Wall Street ‘dos’ and ‘don’ts’ have always reminded me of the ‘Stop! Look! Listen!’ signs encountered on a day’s motor trip, whose number and sameness cause them to be disregarded.”

I don’t know about you, but I find these things endlessly fascinating. That a man writing in 1917 could speak to us so clearly and usefully is one of the charms of markets. No matter what time or place, people are people, markets are markets, and they seem to behave in a universal manner.

Therefore, if we know what kind of behavior loses, we should do something different if we want better results. That would be picking up beaten-up stocks and riding them, rather than trying to guess at price movements and jump in and out of them.

So I’d urge you to be patient with your stocks. In my investment service, Mayer’s Special Situations, I have recommended a select group of promising stocks with tremendous upside potential. Not all of them will work out, of course. But as a portfolio, I think we will continue to have some big winners over the years.

Regards,

Chris Mayer

for The Daily Reckoning

Chris Mayer is managing editor of the Capital and Crisis and Mayer’s Special Situations newsletters. Graduating magna cum laude with a degree in finance and an MBA from the University of Maryland, he began his business career as a corporate banker. Mayer left the banking industry after ten years and signed on with Agora Financial. His book, Invest Like a Dealmaker, Secrets of a Former Banking Insider, documents his ability to analyze macro issues and micro investment opportunities to produce an exceptional long-term track record of winning ideas.

Urgent Video Report: Thanks, Ronald Reagan! Today’s Washington might be out to ruin your retirement. But lucky for us, Reagan’s White House might have just saved you. How? With a little-known “loophole” Ronnie signed into law nearly 25 years ago. Click here for details.

With its announcement this week that it will keep interest rates near zero until at least late 2014, the Federal Reserve has put another large crack into the foundations underlying the US dollar. In a misguided attempt to provide clarity and transparency, Ben Bernanke has instead laid out a simple road map for economists and investors to follow. The signposts are easily understood: the Fed will stop at nothing in pursuing its goals of creating phantom GDP growth, holding down unemployment, propping up stock and housing prices, and monetizing government debt. To do so, it will continue to pursue a policy of negative interest rates, while ignoring the collateral damage of unsustainable debt, virulent inflation, misallocated resources and credit, suffering yield-dependent retirees, and a devalued U.S. currency.

Not surprisingly, precious metals and foreign currencies rallied strongly on the news – with gold up more than 4.3% and the Dollar Index down nearly 1.6% in the days following the announcement. The Dollar Index is now down more than 3.5% from its highs in mid-January.

In coming to the momentous decision to extend the Fed’s prior low-rate promises by another 18 months, Bernanke and his cohorts relied on a somber view of the economy that is at odds with the sunnier view presented the night before by President Obama in his State of the Union address. To justify holding rates so low for so long, the Fed is choosing to ignore the fact that CPI inflation is currently running north of 3%. Instead, it has conveniently chosen to look at a hand-picked alternative measure, the chain-weighted core PCE, which comes in just a shade below the Fed’s arbitrary 2% target. How convenient.

After some changes in key membership at the Federal Reserve’s policy-setting Open Markets Committee, in which a few long-time hawks were put out to pasture, the Fed has now established itself at the extreme dovish end of the policy spectrum. Among other central banks around the world, it may now be outflanked only by some very profligate ones in South America and sub-Saharan Africa. Unfortunately, the FOMC has its hands on the wheel of the world’s reserve currency, and therefore its decisions may lead the planet into financial chaos as long as other nations are content to follow the Fed farther and farther into a swamp of liquidity. To paraphrase Pete Seeger’s protest of the escalation of the war in Vietnam, “we are waist deep in the Big Muddy and the damn fool yells ‘press on.'”

The only bright side of the announcement is that it provides precious-metal and foreign-equity investors a fairly good sense that they are on the right side of history. In order to keep rates low, especially at the long end of the yield curve where it matters most, the Fed must continually print money to buy U.S. Treasuries. This will likely push more investors into gold and away from dollar-denominated assets.

As a testament to their own faith in themselves to forecast economic conditions, 6 of the 17 voting FOMC members indicated that they would have preferred to keep rates close to zero at least through 2015. Some even had the audacity to prefer no change until 2016! This comes from the body that couldn’t predict the 2008 financial crisis, even while it stared at them from point-blank range. To look into a completely uncertain future and determine that negative interest rates can persist for another four years without igniting inflation is to me the height of economic insanity. Sadly, the inmates have the keys to the institution.

The lunacy persists in the rest of the government as well, with Congress and the White House still failing to address our nation’s long-term debt issues. The Fed’s commitment gives these politicians a “Get Out of Jail Free” card to continue avoiding responsibility. The deficits will be monetized, so no real efforts need be made to cut spending or raise taxes on middle-class Americans. Central to these plans is the assumption that the rest of the world will happily park their savings in U.S. dollars forever. If the latest announcement does not disabuse the world of this notion, I don’t know what will.

As long as interest rates remain far below the rate of inflation, the U.S. economy will fail to equitably restructure itself for a lasting recovery. As a secondary effect, U.S. savers will likely continue to suffer from a lack of yield and a weakening currency. In the end, the collapse of the U.S. economy will be that much more spectacular due to the great lengths we have gone to postpone it.

About Peter Schiff – CEO & Chief Global Strategist Euro Pacific Capital and Euro Pacific Precious Metals

Mr. Schiff is one of the few non-biased investment advisors (not committed solely to the short side of the market) to have correctly called the current bear market before it began and to have positioned his clients accordingly. As a result of his accurate forecasts on the U.S. stock market, economy, real estate, the mortgage meltdown, credit crunch, subprime debacle, commodities, gold and the dollar, he is becoming increasingly more renowned. He has been quoted in many of the nation’s leading newspapers, including The Wall Street Journal, Barron’s, Investor’s Business Daily, The Financial Times, The New York Times, The Los Angeles Times, The Washington Post, The Chicago Tribune, The Dallas Morning News, The Miami Herald, The San Francisco Chronicle, The Atlanta Journal-Constitution, The Arizona Republic, The Philadelphia Inquirer, and the Christian Science Monitor, and appears regularly on CNBC, CNN, Fox News, Fox Business Network, and Bloomberg T.V. His best-selling book, “Crash Proof: How to Profit from the Coming Economic Collapse” was published by Wiley & Sons in February of 2007. His second book, “The Little Book of Bull Moves in Bear Markets: How to Keep your Portfolio Up When the Market is Down” was published by Wiley & Sons in October of 2008.

Mr. Schiff began his investment career as a financial consultant with Shearson Lehman Brothers, after having earned a degree in finance and accounting from U.C. Berkeley in 1987. A financial professional for over twenty years he joined Euro Pacific in 1996 and has served as its President since January 2000. An expert on money, economic theory, and international investing, Peter is a highly recommended broker by many leading financial newsletters and investment advisory services. He is also a contributing commentator for Newsweek International and served as an economic advisor to the 2008 Ron Paul presidential campaign. He holds FINRA Series 4, 7, 24, 27, 53, 55, 63 & 65 licenses.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair