Daily Updates

Market Buzz – Boyd Beats the Street Again

North American markets ended this past week on a decidedly sour note on Friday. All told, the S&P TSX composite index ended the 5-day session down 1.36%, while the Dow industrials was down 2.19%. The question now becomes whether or not the down week will become a trend and put a stopper in what has been a strong rally that has lasted over three and a half months.

Headlining the negative sentiment which sent markets lower was another round of worry that the Chinese government will be forced to take further steps to curb lending and slow the country’s economy. This pushed commodity prices and the resource-heavy Toronto stock market sharply lower Friday.

On the day, the S&P/TSX composite index tumbled 185.5 points or 1.43% to 12,749.24, while the resource laden TSX Venture Exchange declined 32.14 points to 2,007.14. The Canadian dollar fell heavily against the U.S. dollar as prices for oil and metals retreated, losing 0.9 of a cent to close at 99.1 cents US.

Expectations of more Chinese government measures to tighten credit and slow economic growth have been rising since data released Thursday showed that inflation hit a 25-month high in October.

In U.S. economic news the University of Michigan’s gauge of consumer sentiment edged up to a better than expected 69.3 from a reading of 67.7 in October. However, the gauge is still well below June’s reading of 76 and pre-recession levels above 80.

Switching gears to our Canadian Small-Cap universe (www.keystocks.com) this past week, http://www.keystocks.com/ReportRequest.aspx, the Boyd Group Income Fund (BYD.UN:TSX), posted another strong set of quarterly results pushing its share price to new highs.

Through its operating company The Boyd Group Inc. and its subsidiaries, is the largest multi-site operator of automotive collision repair service centers in North America, currently operating 133 locations in the four Western Canadian Provinces and eleven U.S. States. Boyd carries on business in Canada under the trade name “Boyd Autobody & Glass” (37 centers) and in the U.S., Boyd operates under “Gerber Collision & Glass” (59 centers) and “True2Form” (37 centers).

This past week, Boyd reported that its revenues for the three months ended September 30, 2010, increased by 32.1% to $69.0 million compared with sales of $52.2 million in the same period of the prior year, after adjusting for the effect of discontinued operations. For the quarter, net earnings after discontinued operations were $3.2 million, or $0.267 per diluted unit and Class A common share, compared with net earnings of $2.2 million, or $0.188 per diluted unit and Class A common share, for the same period in 2009. The Fund paid distributions of $1.0 million, representing a payout ratio of 16.9% for the quarter.

Boyd has now returned 229% to our clients over the past couple year after hitting new highs at the $7.00 level this week.

Looniversity – Consumer Confidence 101

If you’ve ever watched the markets with even a modest degree of interest, you’ve probably heard of the Consumer Confidence Index (CCI). Ever wonder what the heck it is? Let us put you at ease. In the U.S. (most widely quoted), the CCI is put out by the Consumer Confidence Board and based on a survey that samples 5,000 households. The CCI is considered one of the most accurate indicators of confidence. It looks at factors including wages, interest rates, spending habits, and even goes as far as calculating the number of “help wanted” ads in newspapers to detect how tight the job market is.

The basic idea behind consumer confidence is that the better consumers’ current and economic prospects appear, the more likely he/she is to spend – the more he/she spends, the better it is for the overall economy. Of course, the opposite is also true.

When evaluating the index, many people pay close attention to trends or the moving average over the past 3-6 months. Should the index move above or below the moving average, it is a good indication that consumer confidence is significant. Month to month changes are not considered to have as great an impact as the overall trend.

The CCI is watched closely by the U.S. Federal Reserve when determining interest rates, which affect stock prices. Lowering interest rates make it easier to borrow, which ultimately supports consumer spending and higher confidence – something the stock markets get a warm and fuzzy feeling about.

Put it to Us?

Q. When analysts or accountant types talk about “book value”, what are they referring to?

– Paula Kerr; Edmonton, Alberta

A. Outside of the financial world, “book value” can probably be looked at as that little red tag in the corner of your paperback, but within the wonderful world of finance, it has two other distinct meanings.

- The value at which an asset is carried on a balance sheet (example: a car for a cab company). In other words, the cost of an asset minus accumulated depreciation.

- The net asset value of a company, calculated by total assets minus intangible assets (patents, goodwill) and liabilities.

Book value is the accounting value of a firm. It has two main uses:

- A. It is the total value of the company’s assets that shareholders would theoretically receive if a company were liquidated.

- B. By being compared to the company’s market value (price-to-book ratio), the book value can indicate whether a stock is under or over-priced.

KeyStone’s Latest Reports Section

- Q3 Results Disappoint from Medical Equipment Provider, Yield Remains Strong, but Balance Sheet Weakened – Rating Downgraded to SELL (Flash Update)

- Staple Consumer Service Company Posts Better-Than-Expected Q3 2010 Results, Significant Acquisition, Ups Distributions for 12th Consecutive Quarter, Yield 5.14% – Maintain Rating Despite 200% + Gain for KeyStone Clients (Flash Update)

- Oil & Gas Service Stock Post Strong Q3 Rebound & Positive Management Outlook for Balance of 2010 – Maintain Rating (Flash Update)

- Higher Metal Prices Result in Strong Third Quarter for Breakwater Resources – 43% Share Price Appreciation Since Initial Recommendation, but Valuations Remain Attractive at 4.8 Times Earnings and 1.3 Times Tangible Book Value (Flash Update)

- Wireless Phone Retailer Announces Strong Q3 Results, Primed for Better Q4 – Maintain BUY Rating (Flash Update)

“…with all the thought and good intentions that we provided…we achieved absolutely nothing. Nothing that I did and very little that old Ben [Strong, head of the US Federal Reserve] did…produced any good effect…or any effect at all. Except that we collected a lot of money from a lot of poor devils and gave it over to the four winds.”

In three sentences, Montagu Norman, ex-chief of the Bank of England, described the handiwork of a whole generation of his fellow financial plumbers. This was the generation that made central bankers what they are today. Before 1914 they were expected to do nothing, that is, neither to aid the economy nor harm it. Since 1945, hardly a day went by that they did not clog a pipe or inadvertently blow up a gas main.

This was the generation of Hjalmar Schacht in Germany and Emile Moreau in France, while the aforementioned Ben Strong represented the US and Norman himself, wearing his velvet cape and traveling under a pseudonym, stood up for England. This was the generation that financed war well and the peace badly. Borrowing heavily from the Americans, the British and the French were able to keep WWI going long after they were effectively bankrupt. Then, rather than write off the bad debt, everyone waited for someone else to pay it. The Americans watched the mail for checks from the British, while the British sent polite reminders to the French, who tried to foreclose on the Germans by invading the Ruhr; this got them no money, but it had the unintended consequence of boosting Adolph Hitler’s budding career in politics. The debts were bad; the busted-up Reich couldn’t pay anything near the amounts demanded. And the more grease the Germans scraped up and sent west, the more their own economy creaked and weakened; the more they tried to pay the less they were able to pay.

This was the generation that took its currencies off the gold standard in order to run up debts that they couldn’t pay…and then went back on the gold standard, as if they meant to repay them…and then off again in order to renege.

And this is the generation that is autopsied in Liaquat Ahamed’s book, Lords of Finance. It is meant to be a book about finance. But the central figures seem scarcely able to add and subtract. The Germans faced a $12 billion reparations bill, equivalent to about $2.4 trillion today. There was no way they could pay. Pretending that the money was forthcoming then was as vain and pernicious as expecting the Irish to make good on their bank debt, or expecting Americans to honor their $200 trillion worth of financial commitments, today.

At least the Frenchman, Moreau, had his priorities right. He ducked meetings and dodged international monetary conferences so that he would be in the country for the opening of hunting season or so he could run for mayor of his home village of St. Leomer, with about 200 residents. Later, he left his post completely, in order to earn more money at the Bank of Paris and the Low Countries.

His German counterpart, Horace Greeley Hjalmar Schacht, should have taken up hunting too. Instead, he took up Hitler. But that was after he was famous for having solved Germany’s hyperinflation problem. The mark had fallen to 4.2 trillion to the dollar in November, 1923. The trouble with the mark was obvious. There were too many of them; Schacht’s predecessor, von Havenstain, had anticipated quantitative easing by 9 decades. Schacht took over at the Reichsbank and on the 20th of November introduced a new currency, the rentenmark. Von Havenstain dropped dead the same day. At least Mr. Schacht was a smart fellow. Like Norman, he occasionally was afflicted by an honest insight: “The whole modern world is crazy…everybody here is crazy,” he said. “And so am I… I am compelled to be crazy.”

But the remarkable thing is Ahamed’s conclusion. On 502 pages we listen to central bankers and economists quack like ducks. On page 503, the author reveals that he is deaf. He tells us that the world is a better place thanks to them. All the evidence of the previous pages argues against it. None of them increased world output by a single sou or pfennig.

Take Mr. Strong. Would things have gone better if he had not died in 1928, as the author suggests? He imagines that Strong would have intervened more forcefully in 1931, forestalling further bank failures. He seems to have missed the lesson of his own book – that bad debts should be allowed to die quickly. Besides, in his own telling of the story, it was Ben Strong who was more responsible for the Great Depression than anyone else. He lowered rates in 1927, even though the stock market was already running hot. “One of the most costly errors committed by [the Fed] or any other banking system,” Adolph Miller testified before Congress in 1931. The error led to a bubble…which was followed by a bust, which his successors – who again refused to let bad debt die – turned into a long depression.

Good work, boys.

Regards,

Bill Bonner

for The Daily Reckoning

Joel’s Note: Bill is now accepting applications to join The Bonner & Partners Family Office.

If you haven’t had a chance to review the invitation, you can do so below. It should be mentioned, however, that this opportunity is not for everyone. To be blunt, it requires a serious commitment on your part…a commitment most people will never make. Then again, most people will never gain access to the international contact list of industry specialists and contrarian analysts Bill has spent the past three decades building. Most people will never amass, let alone preserve, the kind of wealth and financial security they dream of…

Either way, the offer to join The Bonner & Partners Family Office is open. It’s not for everyone, but it’s here for you, if you want it. [Click To View Invitation]

Longwave Group founder Ian Gordon sees strong signs that point to impending catastrophe, citing historic precedents. A globally renowned economic forecaster, author and speaker, Ian Gordon has been described by Eric Sprott of Sprott Asset Management as “a rare breed in the investment advisor arena…If you care to listen, Ian will tell you how it will all end.”

But despite his chilling forecast, which includes the Dow dropping to about 1000 points, Ian expects investments in high-quality junior gold miners to pay off royally…because the capital fleeing the markets will flow in their direction.

The Gold Report: In the 11 years that you’ve been investing in gold juniors, you’ve recorded an annual rate of return of approximately 70%. Going back to 2000, most brokers and money managers likely would’ve categorized your investment strategy as very risky. However, you’ve stated that you always felt it’s been very safe because you understand the Kondratieff Cycle. What about the Cycle gave you the confidence to go long on gold and gold juniors?

Ian Gordon: I knew that the big bull markets in stocks always occur in the autumn of the cycle; and in 1999, I was confident that the autumn bull market that started in 1982 was coming to an end due to the massive ongoing speculation, particularly in the dot.com stocks. A new issue was coming to the market every day and once it did, the price rose two to three times on the first day of issue. That kind of speculation, and the fact that some things should never have even been allowed to come to the market, indicated to me that we were coming to the end of the big autumn bull market – sort of like the frenzied days in the summer of 1929.

When such big bull markets end – as it did in January 2000 for the Dow and March 2000 for the NASDAQ – it’s a signal that you’re going into the Kondratieff Winter period. This is the time when debt is wrung out of the economy, essentially. Knowing that, and knowing what happened following the ’29 autumn stock market peak that signaled the onset of winter, I knew the end of the big bull market would be extremely bullish for gold just as it was following the 1929 stock market peak.

I was also watching the Dow/Gold ratio, which is the price of the Dow Jones Industrials divided by the price of an ounce of gold. This ratio peaked in July of 1999 when it took 43.85 oz. of gold to buy the Dow; that was the highest level this ratio has ever been. That extreme high convinced me that the great autumn stock bull market was ending. That stock market peak would herald the onset of the Kondratieff Winter when debt is eradicated from the economy. Winter is a terrible time for stocks but a very favorable season to be invested in gold and gold mining shares; thus, I was very confident in determining that a new and very strong and long bull market was about to begin in gold and gold shares. Consequently, I positioned my investment account 100% in precious metals stock, principally Gold Mining shares, and the entire investment account was committed to shares in the junior miners.

TGR: If it started in 2000, we’re now 11 years into this Kondratieff Winter; but it’s only been bad for the last two years. How much worse will it get before it starts getting better?

Ian Gordon: It has to get a lot worse. The debt has to be wrung out of the economy. Because we’re on a pure fiat paper money system, worldwide debt is massive, particularly in the United States. If you look at non-public debt in the US – corporate, consumer and financial debt – it’s $42 trillion, and most of that will be washed out of the economy.

It’s a very painful process. It creates massive pressure on the creditors, principally the banks and the debtors, which results in huge bankruptcies on both sides of the ledger. We’ve already seen banks failing and that process is not finished. We’ve already started to see huge bankruptcies – General Motors, AIG, several companies that have already failed because of the debt. The process has only just begun.

TGR: If the government is printing money to pay off some of the public debt and the debt has to be wrung out of the system before we see another spring, doesn’t that just prolong the winter?

Ian Gordon: That’s what happened following the ’29 market peak, and the US was in a much better position than it is today. At that time, the US was the world’s largest creditor nation; I think the total federal government debt was $16 billion as opposed to nearly $14 trillion now. Hoover and Roosevelt threw money at the economy trying to bail it out. They weren’t successful but they did significantly increase the federal debt during the ’30s; it increased even more during World War II.

TGR: How do you measure the extent to which debt is being wrung out?

Ian Gordon: The best way is by looking at debt in relation to GDP. The US debt:GDP ratio last bottomed in 1952, which coincided almost exactly with the onset of spring in the present cycle. But I’m not sure how we’re going to see the public debt wrung out of the system. Obviously, the intention is to try and inflate it away. Unfortunately, during a Kondratieff Winter, you’re nearly always in a deflationary environment because, as debt is cleansed from the economy, prices are dropping dramatically and money is coming out of the economy. It’s very difficult to increase the money supply in that kind of environment. So I don’t see the US government and the Federal Reserve being able to inflate their way out of this predicament. In fact, the US could very much be riding down the same road as Greece, Ireland, Iceland and so on, with Portugal and Spain now waiting in the wings to do that.

It’s going to be a very, very uncomfortable time for all of us. We’re predicting that the world monetary crisis will actually deepen in 2011. The whole world monetary system could collapse due to this excessive sovereign debt; that’s what happened from 1931-1933. At that time, every country went off gold to try and inflate their currencies and buy their way out of the Depression. The world monetary system collapsed and a new monetary system didn’t evolve until 1944, at Bretton Woods, when the US Dollar became the world’s reserve currency. So from the breakup of the system, there’s a gap of several years before a new monetary system is developed.

When the monetary system collapses, essentially, global trade also collapses. After the monetary system collapsed in 1931, world trade dropped by 75%. At that time, the US could afford to become very isolationist because it was self-sufficient in food and oil. Great Britain resorted to trading within the British Empire. Europe became sort of an entity unto itself. We could see something quite similar starting to develop in 2011. We’re almost certain that will bring about trade war and, ultimately, real war.

During the trade war that developed in 1930 when the Smoot-Hawley Tariff Act was put in place in the US , huge tariffs were raised against foreign goods coming into the country. Of course, the Europeans responded in kind by raising massive tariffs against American goods coming into Europe. Essentially, Japan got frozen out, which is why it got very aggressive looking for natural resources.

TGR: Looking at the West, one might put the US and Europe in one bundle. In essence, many economists would put India and China in another bundle. With the latter growing and the former either stagnant or beginning to shrink, do you see any possibility that China and India could buoy up international trade?

Ian Gordon: If the world monetary system collapses – and we are close to that now – world trade collapses, too; and under the circumstances, China or India could do nothing to reverse the situation. Anyway, I see China as being very much the US of the ’20s and ’30s.

TGR: How so?

Ian Gordon: The US became the world’s greatest creditor nation, lending copious amounts of money to the Allies to fight World War I. After WWI, the US went on a massive industrial expansion that included automobiles, aircraft, refrigeration, telephone, cinema, all of sorts of things. That was really the US heyday. Because the country was so wealthy, there was a lot of bad investment. US banks had so much money that a lot of it was loaned out – particularly going into countries, such as Austria and Germany. In ’29, once credit got more restrictive, the US banking system started to get into trouble.

I see the same thing happening now in China. Industrial growth has paralleled or even exceeded what the US experienced in the ’20s. China is now the world’s largest creditor nation as the US was then. There’s a massive amount of bad investment in China; whole cities are being built that are empty – that’s bad investment, bad lending by the banks. I can see that whole system collapsing as early as next year.

TGR: Let’s go back to your outlook for 2011. You’re looking at monetary crisis and a potential failure of the global monetary system. In that case, going to gold makes a lot of sense. How does an investor begin to shift a portfolio toward gold – Gold Bullion, gold mining stocks, ETFs? What would be your recommendations?

Ian Gordon: The physical should be taken in hand. The only paper I can recommend in gold is in gold mining shares. I certainly don’t want to invest in a gold ETF because it’s a paper claim on the physical. Who knows what’s going to happen if this whole thing blows up? What kind of government decrees will come out with regards to gold and so on? If the whole monetary system blows up – and we see a 1-in-5 chance of that in 2011 – it will be much more serious than the blowup of ’31 because the whole system appears to be imploding. People will distrust paper money. I’m not sure how it goes into the end, but those are the kinds of things that people have to consider. They’re quite extreme.

So, is investing in gold shares a good thing? You’re being paid out in paper money and you’re buying in paper money. What happens if paper money is worthless? I don’t know. I’m trying to think that kind of scary scenario through in my own mind. But it’s something of which we should all be aware. We’re basically hanging by our fingernails above a great chasm.

TGR: You don’t like Gold ETFs because you don’t know what a government might do to the underlying asset. Isn’t that also true of gold mining shares? If things go wild, couldn’t you see governments putting tariffs or mining restrictions on what’s coming out of the ground?

Ian Gordon: Yes, that’s a worry. I don’t think we would see that happening in Canada; but in the US , we know that in the ’30s Roosevelt confiscated all US citizens’ gold. After 9/11, a Federal Reserve spokesman suggested that to avert a panic in the market they could buy the shares of gold companies – in effect, nationalizing gold companies.

TGR: Do you factor in such possibilities when you’re looking at junior mining stocks?

Ian Gordon: I do, but we’d probably get some indication if something drastic happened. I am invested in companies that are in Alaska and Nevada and so on. I tend to look more and more into companies that are invested in Canada, as it is the only Western capitalist country that has never confiscated her citizens’ gold. Gold mining is such an important industry in Canada that I just can’t see the government doing it this time, either.

TGR: But the government has nationalized industries in Canada; so what makes you think that wouldn’t happen with mining?

Ian Gordon: If you go back to the ’30s, gold mining became the asset of choice for most investors. Massive amounts of capital flowed into the gold sector. There were major discoveries all along the Abitibi Greenstone Belt, in British Columbia and in the US By 1940, according to the US Bureau of Mines, there were 9,000 operating gold mines within the country. I doubt there are more than 500 gold mines operating in the US today. If money flows to the gold mining industry this time, as it did in the 1930s – and I’m sure it will – a lot of this money will flow into Canada from all over the world.

TGR: As I understand it, when you’re looking at gold juniors you follow a formula that weights management and properties to account for 50% of what you consider a good investment. And you want to see potential for your investment to double within 10 months. Could you tell us a little more about how you analyze companies?

Ian Gordon: First, I never invest in a company unless I’ve met with management; and that’s pretty easy living here in BC. I want to get a confidence in and a feel for management – management is the key. I’ve seen good companies messed up by bad management. I’ve seen companies that were likely looked upon as potentially mediocre at best, but good management can frequently turn such companies into outstanding investments.

TGR: Other than management, what’s important to you?

Ian Gordon: In addition to management, I have to feel comfortable with the properties the company has amassed and the potential that exists for big discoveries on those properties. We certainly do look at political risk when we’re assessing companies; we don’t want to be investing in companies that are located in politically risky countries.

Of course, I have to be confident in management and I have to believe that an investment in the company will produce a significant return. And as you pointed out earlier, I have been able to average about 70% a year over the last 10–11 years in my own portfolio despite taking a massive hit – as did most people – in 2008.

Every time I buy shares in a company, I must be able to see the potential for the share price to double within 10 months. This potential may be because I am anticipating good exploration results or seeing additional ounces being discovered. I look for companies that are not yet recognized by investors because of poor public relations. In some cases, I’ll find this double price potential in a company that has gone out of favor due to a lack of exploration progress, but I might see that things are improving. However, because most investors have grown tired of such companies, they won’t be paying attention.

TGR: You’ve given investors some good information to consider. Let’s hope it’s not as bad as you think it’s going to be.

Ian Gordon: I don’t want it to be this bad but things look pretty bleak, especially when taken from a historical perspective.

TGR: When we reach that turning point where the Dow begins to dive, won’t the junior mining stocks also drop rapidly?

Ian Gordon: They didn’t in the ’30s because all the capital flowed to gold. There were huge discoveries.

TGR: So junior Gold Mining firms will have such opportunities due to the capital flowing toward gold.

Ian Gordon: Right. People like my friend, Eric Sprott – who runs a whole host of funds as the chairman of Sprott Asset Management – are extremely bullish on the precious metals because, like me, he sees the potential of a significant economic and financial worldwide disaster. He, too, is very frightened about the potential outcome of a worldwide economic collapse. And, much the same as I do, he sees that money will flow into precious metals, including these junior companies. That’s where he’s invested and that’s where I’m invested.

TGR: You and many other speakers at the 2010 San Francisco Hard Asset Conference were pretty consistent in the message about expecting worse than we saw last year and possibly even worse than 2008.

Buying Gold? History says you need to own it, offshore, outside your home jurisdiction if you’re right to be Buying Gold for defense. Start here with a free gram at world No.1 online, BullionVault now….

As we start the new year, Beacon Rock Research Founder Mike Niehuser has doubts about growth and believes that inflation may spook stocks and bonds. In this exclusive interview with The Gold Report, Mike recommends looking for leverage to the metal price through investment in exploration and development metal stocks with large world-class assets, and names a few of his favorites.

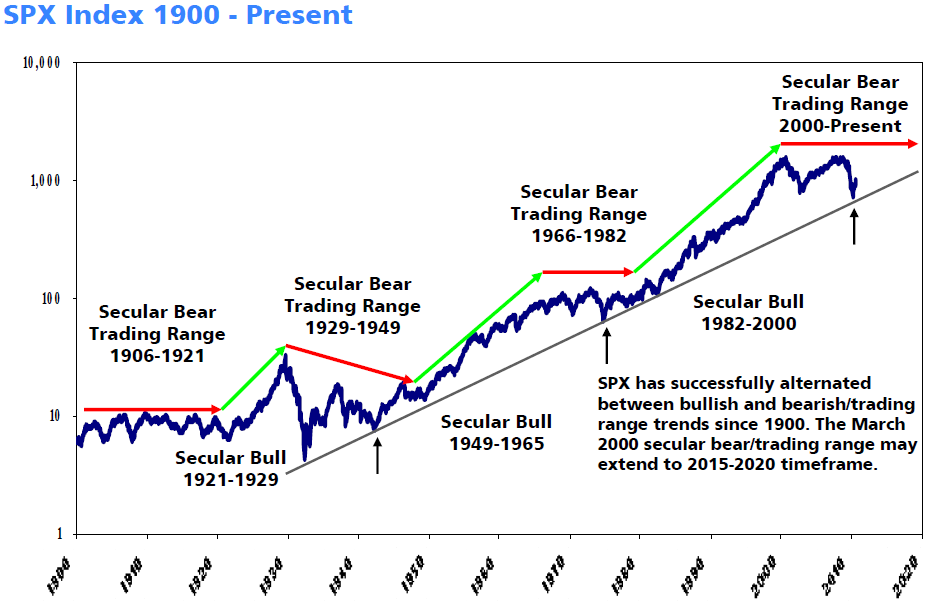

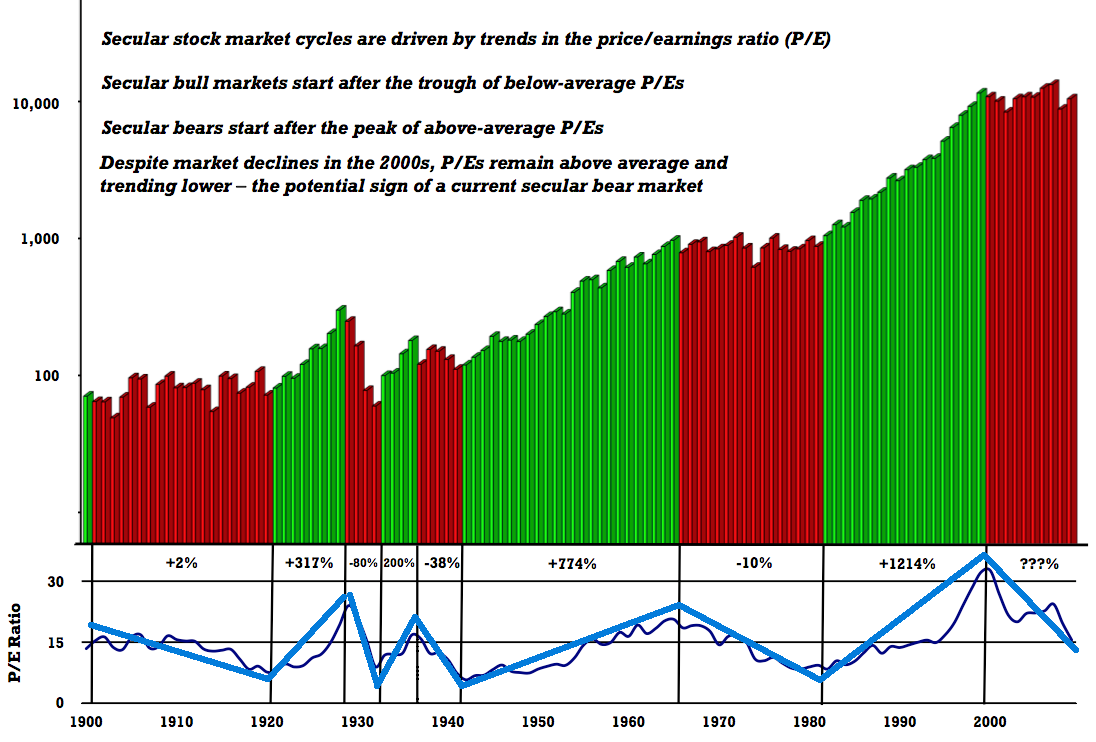

Click on Image for Larger View

Click on Image for Larger View

Click on Image for Larger View

All Charts by The Big Picture

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair