Daily Updates

Market Buzz – Market Uncertainty Makes a Case for Dividend Investing

While the close of market on Friday, June 24th ended a three week spree of consecutive declines in the TSX Composite Index, the picture is not as rosy as one might be inclined to think. The TSX closed the week at 12,909 points, up modestly from 12,769 at the start of the week, but down fairly significantly from the mid-week high of 13,159.

Crude oil remains a hot topic on the market’s collective mind, with the commodity continuing to decline from its year-to-date high of almost $115 per barrel to $91.16 at the end of the market on Friday. Arguments over what causes specific commodities to rise and fall are often highly polarizing with some camps pointing to fundamental supply and demand and others to speculation. The only things known with certainty are firstly that the true answer always lies in between the rationales provided by the opposing camps and secondly, regardless of the real drivers, commodity price movements are impossible to predict. The decline in crude oil price has caused similar declines in Canada’s universe of energy stocks, which is undoubtedly a key contributor to the declines we have been seeing in the TSX, an index whose weighting towards energy is estimated at over 30 per cent. Looking to current events in the oil market, the February shutdown of 1.5 million barrels per day of production from Libya has caused the U.S. government to recently announce the release of 60 million barrels of oil held as strategic reserves. It seems plausible that this temporary increase in supply is at least partly to blame for the recent declines in crude oil prices, as this was undoubtedly the intended outcome of the action. Global economic uncertainty aside, if indeed the release of strategic reserves is a significant contributor to lower prices, then we should see crude oil start to appreciate again after the next 30 days or so. For context, global oil consumption sits roughly between 80 and 85 million barrels per day.

Whether it is concerns over declining commodity prices, lower growth rates in Asia, or the unprecedented debt loads in Europe and the United States, one argument is for indisputable, that is that we are playing in uncharted and uncertain markets. In a market where uncertainty appears to be the rule, many investors have found safe (or safer) heavens in the wonderful world of dividend investing. Throughout history, dividends have been the core source of return for equity investors. Recent studies have indicated that as much as 70% of total equity returns were attributable to dividends between 2000 and 2010. Considering numbers such as these, it is no wonder that we have seen dividend investing come back since the 2008 market meltdown. For conservative investors, utilities, banking, and telecom continue to be the preferred sectors. Leaders in these areas have generated spectacular capital appreciation over the past two years and many tend to increase their dividends on an annual basis. While yields have been compressed during this period, investors are still able to find long-term opportunities to buy companies that pay yields of 3% to 5% and are able to grow their distributions at 5% per year or more. Moving into the higher risk categories of dividend stocks, we have seen opportunities in number industries such as agriculture, healthcare, real estate, financial, and special situations, where companies are continuing to provide investors with a solid mix of income yield and capital appreciation. In these markets, investors are gravitating to yield as income may be the only source of investment return in a flat or down trending market.

For investors interested in learning more about how KeyStone Financial can help add dividend growth stocks to a portfolio, go to our Income Stock Report website (www.incomestockreport.com) or email us at subscriptions@keystocks.com.

Looniversity – Corporate Bling!

A simple question — If a company reports earnings of one million dollars, does their bank account swell by the same amount? Not necessarily. Why not, you ask? Well, in the wild and wacky world of public companies, financial statements are based on accrual accounting, which, in an effort to best reflect the financial health of a company, takes into account non-cash items such as depreciation. Sometimes, however, it can be valuable to strip off all the “accounting noise” and look at how much “actual cash” a company is generating. The statement of cash flow provides us with this information.

What is Cash Flow?

Cash flow is the constant flow of money in and out of a company. The outflow of cash is the money paid every month to pay salaries, suppliers, and creditors. The inflow is the money received from customers, lenders, and investors. All companies provide the cash flow statements as part of their financial statements, but cash flow can also be calculated as net income plus depreciation and other non-cash items.

Why is a look at the cash flow statement important? A company not generating the same amount of cash as competitors is bound to lose out when times get rough (can anyone say now?). Even a profitable company (by accounting standards) can go under if there isn’t enough cash on hand to pay bills. Unlike reported earnings, a company can do little to manipulate their cash situation. Unless tainted by outright fraud (which is apparently a consideration), this statement tells the whole story: either the company has the cash or it doesn’t.

Put it to Us?

Q. I am fairly novice in the investment realm and wanted to ask how much it will cost to get set up to casually invest with a broker?

– Jessy Rudd; Calgary, Alberta

A. Understanding the costs associated with becoming a casual investor is important if you want to be successful. It is important to realize that there are tangible costs, such as commission and funding for an account. Also, don’t forget about the hidden costs, such as the time and effort. Fortunately, it will cost you nothing to set up your account with either a full-service or discount brokerage in Canada. For most beginners however, the first major obstacle is the amount it takes to fund a trading account. There is no magic amount that is needed and this will vary depending on your personal situation.

Commission is the second cost and can vary widely based on which type of brokerage service you require. A full-service broker offers clients access to their research and are often willing to give clients advice based on their risk profiles. With this high-level of service comes a higher commission fee. On the other hand, a discount brokerage offers clients the ability to buy and sell various securities, with a considerably lower cost. Most discount brokers do offer access to their research, but you will have to navigate the information yourself.

KeyStone’s Latest Reports Section

- IP Company’s 2011 EPS Meets Expectations, Hold Strong Cash Position, & Yields 3.6% – Short-Term Cost Increase Leads to Long-Term Opportunity – Maintain Rating (Flash Update)

- China-based Fertilizer Stock Posts Q4 2011 Slightly Below Expected, Growth Expected into 2012, Fear Creates Buying Opportunity (Flash Update)

- Profitable, Low Cost, Junior Gold Producer Operating in South East Asia – New Focus Buy (New Buy Report)

- Cash Rich Communications Software Company Posts Strong Q2, Strategic Acquisition Sets Table for Long-Term Growth – Maintain Rating (Focus BUY) (Flash Update)

- China-based Athletic Apparel Manufacturer Posts Solid Q3 2011 Results, EPS on Upswing Again, Strong Cash Position (Close to Half its Market Cap), No Debt – Reiterate BUY (Focus BUY) (Flash Update)

Exclusive Money Talks Special Bonus: Keith Schaefer’s Investor Report on the Bakken – Email us at info@moneytalks.net

A couple quick thoughts on today’s Big Oil News – the IEA releasing 60 million barrels from Strategic Reserves around the world to help lower global oil prices – before I get into who will benefit from this (and there’s a surprise here).

In terms of fundamentals, this really is a cry for help.

a. 60 million barrels equals about 18 hours of global production – hours, not days or weeks. It’s inconsequential.

b. The world is already well supplied with oil – there is no shortage of oil anywhere on earth that I can see. North America in particular is overflowing with oil.

c. Oil doesn’t trade on its fundamentals, or it would be $60-$70 a barrel right now. Or pick your own number. But it would be lower.

In terms of market psychology however, the IEA may be smarter than the pundits think.

Oil, like all markets, trades on fear. And there is now so much liquidity in the world that often (if not usually) the tail wags the dog in commodity markets. What I mean by that is that the financial derivatives surrounding oil – the ETFs, the futures contracts etc. – help determine the price of commodities as much as the underlying demand. So managing their fear and greed of investors in those products is a bigger job than ever before.

Exclusive Money Talks Special Bonus: Bakken – The Hottest Oil Play Going in North America… and the next junior oil company that could be its next big payout! Email us at info@moneytalks.net to receive this free report from Keith Schaefer, Editor of the Oil & Gas Investments Bulletin now.

With this new reality that has developed over the last decade, but especially since QE1 & QE2, I would suggest the governing elites of the world (DAD) need a new way to communicate to the capital markets (MUSCULAR INDEPENDENT TEENAGER) to really get their attention that they will pull out all the stops to obtain a semi-permanent lower oil price.

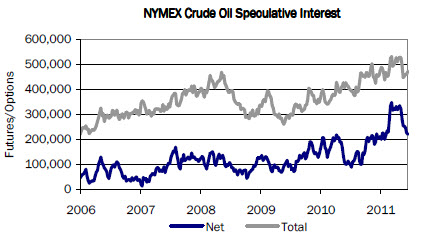

But what it could do is convince many of the new entrants in the futures market to dump their “oil long” holdings. Speculators have been buying oil long contracts in record amounts up until a few months ago. See this chart from Canadian brokerage firm Canaccord Genuity:

Now, the chartist in me says that after a recent round of weakness, a dive in oil prices will weed out the latent longs – cause them to give up hope. And then the liquidation of ETF holdings, of futures contracts, begins in earnest and causes a waterfall effect on oil prices.

If/when that speculative liquidation happens, trend lines get exacerbated – things go up higher than fundamentals would say they should, and go lower than what fundamentals indicate. So I suggest that when oil traders and other market players say oil is going HERE, wherever here is, you can likely count on it going 10% past that.

That’s the tail wagging the dog, and why we have so much more volatility in the commodity markets now.

So in one sense, this chart tells me the timing of the IEA announcement was perfect, if they were targeting a large part of the market – the speculators. They’re saying we will do everything we can to keep oil lower for longer than you think, this lower oil price scenario is not short term, so you will lose money on your trade.

(I have this mental image of the head of the IEA saying to oil long speculators – SOLDTOYOUSUCKA!)

Perhaps the IEA was looking at fundamentals saying hey, there is no need for this oil price as supplies are plentiful and the western world’s economy is weak, so if we can just change market psychology a bit, we can get what we want – $80 oil.

So who will benefit from today’s news, i.e. how can I use today’s news to make money?

One place is obvious, the other one is…counter-intuitive.

Certainly if you want lower prices, bring on more supply. And that means more drilling, which should be music to the ears of investors in energy services stocks – the drillers and their sub-trades, like the fracking companies and the supply companies to them.

The energy producers of the world ARE increasing their spending to find new supply – a whopping 25% more in 2011 over 2010 to $133 billion, says US securities firm Raymond James. Here in western Canada, producers will be spending 32% more this year over last, according to Canadian brokerage Wellington West Capital Markets.

But the strangest sector to benefit from lower oil prices, I think, will be junior oil stocks. For the last two months the overriding psychology in this space has been backward.

That is – the oil price has to go down before junior oil stocks can go up.

Junior oil stocks were having the same inverse relationship to oil that the Dow Industrials were; a high oil price will cause recession so sell riskier and junior stocks – including junior oils.

The first clue that this thinking was affecting junior oil stocks was when they did not benefit from the last $20 move in the price of oil, up to $125/barrel.

Then as the Arab Spring did NOT move into Saudi Arabia, the world’s largest oil producer, the political risk premium came out of the global oil price, and oil fell back to $100.

But that wasn’t enough for junior oil stocks to move again. Partly that’s because it’s summer – many investors leave for holidays, and trading volumes dry up. A lot of these stocks have raised hundreds of millions of dollars and now have hundreds of millions of shares issued – and need lots of volume to keep their share price up. So in one sense, the value reset button has already been pushed on many junior oil stocks.

For over a month now I’ve been reading into the junior energy markets that until oil gets under $90 and stays there for a short while, the market is not willing to buy the juniors in such a wave that a rising tide will lift all boats like it did from September 2010 to March 2011.

Another way of saying this is that junior oil stocks aren’t low because the market has no faith in the oil price; rather, it’s because the market has too much faith in it.

So once the market is convinced the oil price will stay low enough to not cause recession, it will again buy the juniors, as even at $80/bbl these companies make GREAT money. Some valuations will get reset (though much of that is now done), but the fast growing, discovery making juniors will once again get rewarded.

– Keith

Keith Schaefer is Editor and Publisher of the Oil and Gas Investments Bulletin. The Bulletin subscription service finds, researches, and profiles growing oil and gas companies that Mr. Schaefer buys himself, so Bulletin subscribers know he has his own money on the line.

Mr. Schaefer identifies oil and gas companies that have high growth rates, or have the potential for that – this usually means they have a large undeveloped land position in an area where either production costs are very low or production rates can be very high. They are covered by several research analysts, so there is research support and institutional money flow behind them.

The Oil and Gas Investments Bulletin subscriber portfolio is up 85% year-to-date as of October 10, 2009.

There is tremendous potential to profit in oil and gas companies for informed investors. Technology has transformed exploration in both oil and natural gas in three short years. New plays in old locations are opening up huge profits for producers and their shareholders. And high-impact international plays are starting to benefit from these new technologies as well.

For subscription information, please click through to the Oil and Gas Investments website HERE

ETF’s are showing early technical signs of recovering from oversold levels.

Considering the only soundbite that was relevant from Ben Bernanke’s 45 minute 2:15pm oratory was that “we don’t have a precise read on why this slower pace of growth is persisting” America, and the entire civilized world, could have done just as well without it.

Instead, we should have listened to Jim Grant, who once again correctly identifies all the things that the Fed chairman should have said (Bernanke certainly focused on the other side): “What we are not going to get is a concession that QE2 has achieved its unintended consequences, namely a lower dollar exchange rate, a higher gold price meaning weaker confidence in the dollar, slower economic growth and a higher measured rate of inflation. Those are some of the things that have come out of this experiment and let us call it by its name money printing…How do we know that this 30% gain in the Russell and 20% gain in Dow since the Chairman spoke in August, how are we to know these are real values. The prices are up, but are people who are buying these stocks on the back of the Fed, are they doing something wise from an investment point of view, and if the market is too high because the Fed has put it there, what does the Fed do when the market comes down, which opens the fate for QE3.”

And on a far more important topic which we will soon hear much more of, namely extensive US money market exposure in Europe, which will be completely locked up if, pardon, when there is a major liquidity run in Europe snagging American money market liquidity: “The money market mutual funds have nothing to do in this country cause rates are zero, go to Europe. So money market mutual funds investors are taking quite ponderable risks for about a 0% return, these funds are yielding a few basis points only. But to get those few basis point, these funds are crossing the Atlantic right smack dab in the middle of the European banking crisis. This is a prime example of the unintended consequences of this massive intervention by our central bank.” Indeed, this is just one simple example of the massive clusterfuck, which certainly does not need Greece’s $5 billion notional in CDS, to make the Lehman liquidity freeze seems like a little melting ice cube. And since everyone now agrees that Greece will default, and it is only a matter of time, all the trillions in dollars in the shadow and open banking systems that we have been exposing for years now, will suddenly be locked up in the forms of 1 and 0 in computers belonging to institutions that are no longer operational. And most unfortunately, the man in charge of it all, has a quivering lip problem.

Much more in the entire must watch interview with Bloomberg’s Margaret Brennan:

…go HERE for the Bloomberg video (scroll down a bit)

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair