Then Joseph said to Pharaoh, “The seven good cows are seven years, and the seven good heads of grain are seven years; it is one and the same dream. The seven lean, ugly cows that came up afterward are seven years, and so are the seven worthless heads of grain scorched by the east wind: They are seven years of famine.”

When a bunch of hoary old traders sat under the buttonwood tree in New York City in 1792, they knew the point of a market.

When a bunch of hoary old traders sat under the buttonwood tree in New York City in 1792, they knew the point of a market.

It was a place where buyers met sellers and they traded on a mutually agreed price.

A market was a place where people took risks, overpaid, got bargains, failed, gained, and in the end pooled money to build canals, manufacturing, and international trade.

Times Change

Yesterday, we’ve discovered yet again that the stock market is a casino where the house always wins. Janet Yellen, the chief of the Federal Reserve, has yet again shown us that “price discovery” is meaningless and the advantages are for the well connected.

Kissing the Dove of Spring

Let’s just go back down memory lane. Late last year, Yellen said she would hike rates if unemployment was below 5% (it is) and inflation was stable (it is).

She stated that stocks were expensive (P/E of 17) and the economy was going to overheat. But she was robust and had a backbone. There would be no bubbles on her watch, so she raised rates in December a quarter point to 0.50%.

The market rallied in a reverse “sell the news” scenario. She went on to say that she would raise four more times this year. The market kept going up. It was 1999 all over again!

Then in the gloom and cold of February, she shuffled the point of her duckboot in the gray slush of a New York sidewalk and mumbled under her breath. Perhaps she was imprudent.

And so, with the gusty winds of late March blowing down the canyons of New York, she spied a rock dove, an omen, and said she wouldn’t raise after all. At least not until that utopian day in the stock market where growth returns, otherwise known as the second half of the year. And there might even be a QE4 if things get tough.

No Privy Here

I’m not privy to what information Yellen has or pays attention to. In her speech she talked a lot about a slowdown in China — so perhaps that’s the problem.

Or not. Who can tell? At least Greenspan carried an overstuffed briefcase on days he hiked rates, thus giving the speculators a fighting chance. This Fed gives the impression that it doesn’t know what is going on much less where it wants to go.

Your humble editor has spotted one pattern in the Fed going back to the 1990s. They talk up rate hikes, set up the shorts, and then blow them out. The market then notches higher and the whole game starts over.

Bubble and Bust

Over the long haul, every boom needs a bust to clear out the deadwood. Bailouts by definition lead to more bailouts. Failure, on the other hand, is self-correcting.

There is another dominant economy that never cleared out the deadwood and instead propped up the status quo with bailouts, low rates, and easing: Japan, the country that just announced industrial output dropped 6.2% in February.

This is what happens when you borrow and bail out repeatedly over the decades.

It’s worse than a market crash. It is a market crash followed by false hope after false hope. It’s 25 years of taking your money.

Buy, Hold, and Go Broke

Last week I told you the market looked like it was topping out. Forward earnings were abysmal and would have to be downgraded. You can read that here.

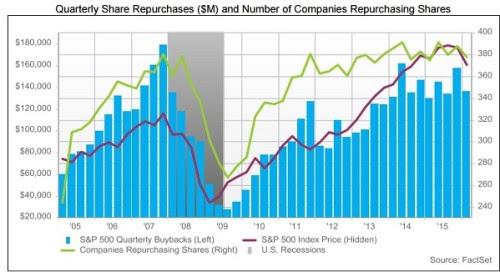

This week I’ll tell you the fundamentals are even worse. One of the pillars holding up this sham of a market has been stock buybacks. As you can see by this chart, that trend is also starting to reverse.

Note that the last time buybacks hit a zenith (in 2008), similar to the present,

it was right before the crash. As soon as stock buybacks ended, the stock market fell 50%.

If loans get hard to come by, buybacks are less of an option. Perhaps this is what the Fed is worried about.

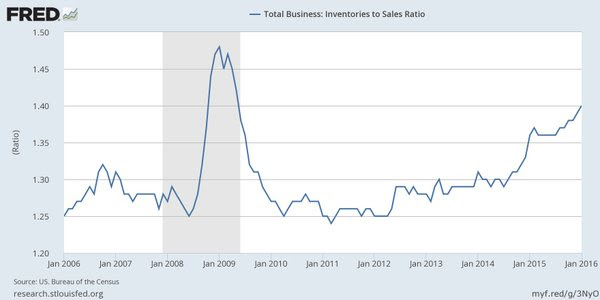

Or maybe it’s the inventory-to-sales ratio:

That’s a lot of product to have on the shelves. It must be worked off in one of three ways: writing it off, slashing prices, or cutting production and waiting.

And it’s not priced in. Here is the S&P 500 price-to-sales ratio.

History tells us that when the S&P 500 has a P/S ratio below 0.9, it will be up an average of 81% in five years. If the P/S is above 0.9, in five years, the market will be up only 4.7%.

As you can tell by the chart, we are now sitting at a 10-year high of 1.81 — twice the “buy” price.

That said, you can’t fight the Fed. Fundamentals no longer matter… until they do. Buy silver.

All the best,

Christian DeHaemer

Since 1995, Christian DeHaemer has specialized in frontier market opportunities. He has traveled extensively and invested in places as varied as Cuba, Mongolia, and Kenya. Chris believes the best way to make money is to get there first with the most. Christian is the founder of Crisis & Opportunity and Managing Director of Wealth Daily. He is also a contributor for Energy & Capital. For more on Christian, see his editor’s page.