He roller coaster

He got early warning

He got muddy water

He one Mojo filter

He say one and one and one is three

Got to be good looking

Cause he’s so hard to see

Come together right now

Over me

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

Come together, yeah

-The Beatles

It seems the European Central Bankers didn’t read the latest issue of Institutional Investor. Had they perused the pages, they may have stumbled on an acceptable strategy from former Goldman Sachs managing partner slash US Treasury Secretary slash Citigroup chairman, Robert Rubin. In the words of writer Ben Baris, speaking on the subject of restoring the US economy Rubin said, “A potent combination of political will and the legislative agenda must come into alignment and rejuvenate Washington in order to achieve any goals.”

Funny, later in the article Rubin criticized the Europeans for how they were handling their crisis (implying their stop-and-go tactics should be avoided in the US.)

I would have liked to have been sitting with Sir Robert around an infinity edge pool at some Caribbean getaway this weekend when the European Central Bank tore away their metaphorical WWRRD bracelets in protest of added bureaucratic pressure from “above.”

The G-20 met this weekend to approve additional funding of the IMF that could backstop, particularly with respect to Europe, any nation that might come under pressure during a critical period of economic reforms. Member countries were heard to be singing a cappella to The Beatles hit song, Come Together, which explained comments after the meeting that suggested most finance ministers were on board with this move to bolster IMF resources.

That is except for two relevant parties: the US (who did not want to ask Congress for any more money) and the European Central Bank.

The IMF expressly asked the ECB to cut interest rates back further and ready the liquidity spots in hopes of further relieving economic pressure. And the US’s reluctance to probe Congress didn’t stop Treasury Secretary Geithner from laying responsibility on the back of the ECB. Even though the IMF’s stated goal of raising an additional $400+ billion was achieved this weekend, there is plenty of negativity surrounding the ECB’s discretion.

ECB executive board member Joerg Asmussen

“We think we have done our task in the last months by quite a number of standard and non-standard measures we have taken,”

ECB Vice President Vitor Constancio

“The stance of our monetary policy is fully appropriate … It’s appropriate to the situation and the prospects that we (face) right now.”

ECB’s Jens Weidmann

“You cannot solve structural problems in the economy with instruments of the monetary policy.”

“Higher interest rates are also an incentive to restore lost confidence. The common monetary policy must not be used to compensate for shortfalls in reforms.”

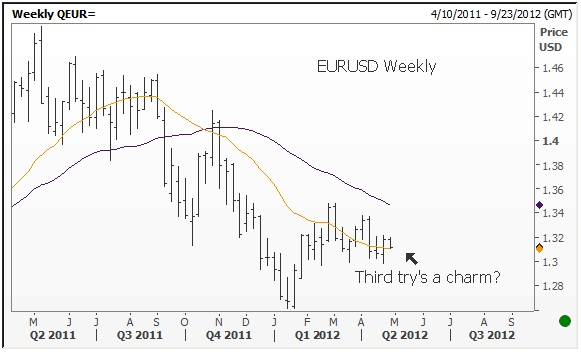

The euro is under pressure this morning. [A major slump in German PMI manufacturing – 46.3 vs. expectations of 49.0 – is not helping, especially since recent sentiment numbers out of Germany have been cause for optimism.]

To Read More CLICK HERE