Do me a favor and punch up a chart of General Electric (GE). Or 3M (MMM). Or DuPont (DD). Or United Parcel Service (UPS). Or basically any major blue chip, widely held, large capitalization stock.

What do you see over the past few weeks? Nothing. Very little net movement. Extremely tight ranges. Some of the smallest daily candles and bars you will EVER see on a stock chart.

It’s not just your imagination, either. The markets are truly somnolent, even now with the traditional pre-Labor Day quiet period over.

I read one fascinating article earlier this week that concluded the Dow Jones Industrial Average hasn’t traded in this narrow of a high-to-low, 40-day range in the last 100 years. Another analyst found the S&P 500 hasn’t been this tightly coiled since 1928.

I read one fascinating article earlier this week that concluded the Dow Jones Industrial Average hasn’t traded in this narrow of a high-to-low, 40-day range in the last 100 years. Another analyst found the S&P 500 hasn’t been this tightly coiled since 1928.

What the heck is going on? And what does all this low volatility mean for you as an investor?

Well, some of the blame lies with “volatility selling” in the options market, as I wrote about last month. It’s another way of squeezing a few nickels of income out of the markets in a NIRP/ZIRP world, and everyone is doing it these days.

Some of it also stems from investors anticipating potential market-moving events. The Federal Reserve and Bank of Japan are meeting on policy later this month, and investors are hesitant to make big moves ahead of those events.

Finally, some of it stems from confusion about where the economy is headed. We had a lousy start to the year, followed by a bounce back in June and July.

Now the question is whether that economic bounce is petering out.

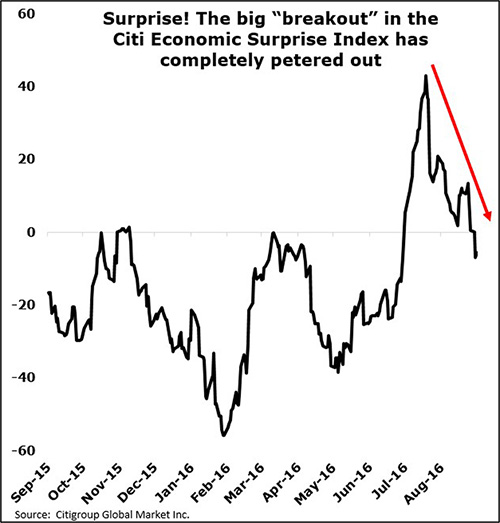

The August jobs figures and other reports on the manufacturing and services sector suggest that is the case. So does the Citi Economic Surprise Index.

The gauge purports to show whether the majority of economic reports are beating or missing economist forecasts. Many bulls crowed about how it “broke out” back in July. But take a look at this chart. The entire breakout has petered out …

I have my suspicions about where things will likely break from here.

The widening disconnect between economic reality and stock prices isn’t very encouraging, and is likely to be resolved by a downside break. Conservative “safety plays” should outperform risky, economically sensitive names. In a pre-recessionary environment, the dollar is also likely to lose, while gold and Treasuries should be winners.

But it makes sense not to get too aggressive until the market actually tips its hand. In your personal investing, I would play things smaller in terms of capital committed until we get a breakout in these various asset classes.

Until next time,

Mike Larson