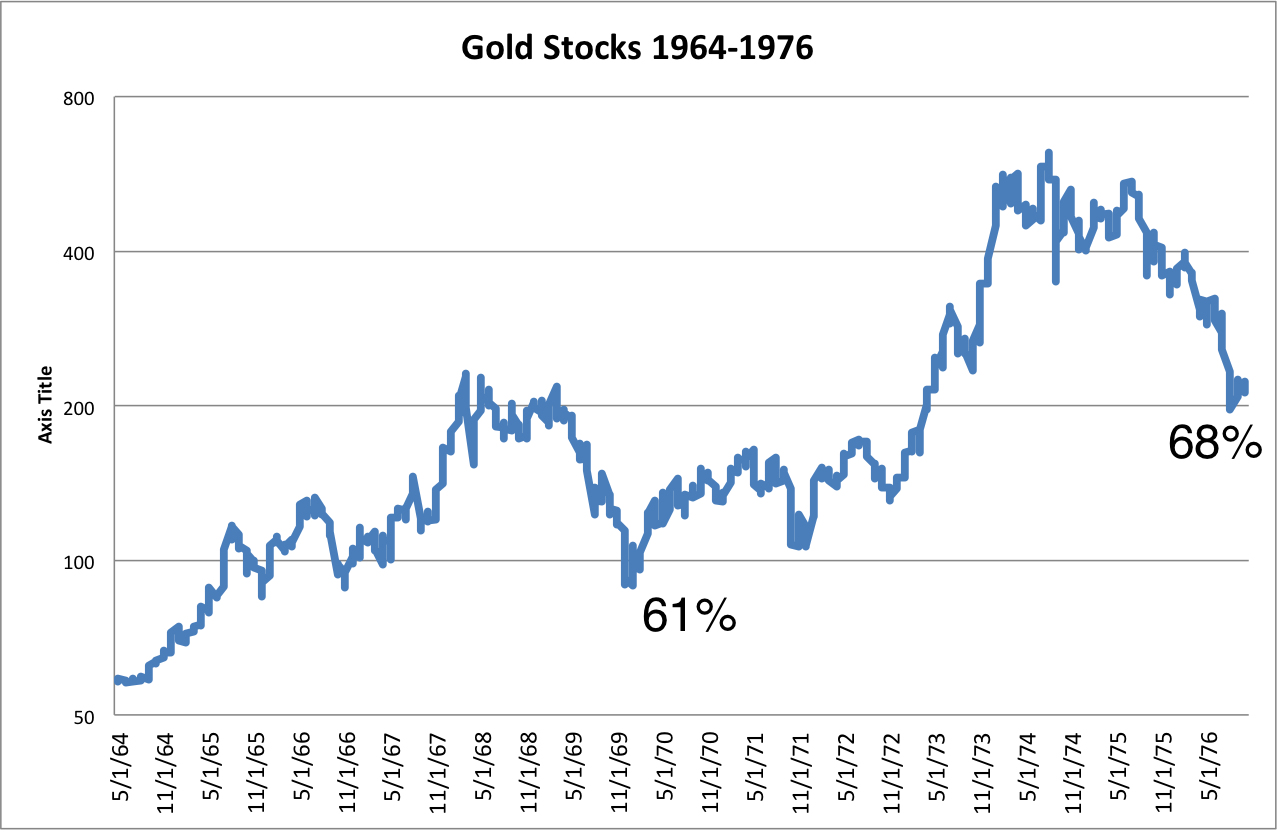

At the end of 2012, the investment community laughed at my prediction that 2013 will produce phenomenal gains in the uranium miners (URA). Read my interview with The Energy Report at the end of 2012 which may have signaled the bottom in the uranium miners.

At the end of 2012, the investment community laughed at my prediction that 2013 will produce phenomenal gains in the uranium miners (URA). Read my interview with The Energy Report at the end of 2012 which may have signaled the bottom in the uranium miners.

In 2013, our uranium bellwethers Areva (ARVCF) and Cameco (CCJ) have significantly outperformed the S&P 500 (SPY) by a significant margin. The uranium price has been making a very bullish turnaround since early November. Cameco is on the verge of a breakout at $22 and we may soon witness a golden crossover of the 50 and 200 day moving average. Now those who ridiculed me claiming uranium was dead are now coming to the realization that the uranium sector which was reviled by investors a year ago is now coming back in favor. Areva and Cameco are significant outperformers in 2013 as well as the small nuclear modular reactor manufacturers such as Babcock and Wilcox (BWC) and Fluor (FLR) which I have highlighted over this past year.

For years I have predicted that the recent low price in uranium which hit 8 year lows in 2013 may actually be the catalyst to look for higher grade and more economic uranium deposits particularly in the Athabasca Basin in mining friendly Saskatchewan and in low cost in situ uranium operators in the United States as the Russian Megatons to Megawatts expired in 2013. This low uranium spot price may actually be causing a uranium rush for these lower cost production capabilities. Higher cost uranium mines are being shut down or delayed all over the world. However new uranium discoveries are receiving a lot of attention especially in the Athabasca Basin which is the highest grade uranium mining district in the world. Some of the older mines such as Rio Tinto’s low grade Rossing and Ranger Mine have been facing technical challenges.

This low price in uranium is possibly the reason why Cameco (CCJ), Rio Tinto (RIO) and Denison (DNN) have been buying junior uranium explorers in the Athabasca Basin trading at bargains due to the weak resource sector. These assets are high grade meaning potentially lower production costs in a stable jurisdiction. Smart money knows nuclear power is here to stay as there are more reactors operating and under construction now post-Fukushima than from before the once in a millennium natural disaster.

…read page 2 HERE