The world has gotten so used to ultra-low interest rates that even economists and money managers seem to be shocked by what happens when rates start creeping back towards normal levels.

The world has gotten so used to ultra-low interest rates that even economists and money managers seem to be shocked by what happens when rates start creeping back towards normal levels.

Some of the mini-bubbles that formed in an essentially free-money environment are now starting to leak. Notably:

US Housing

While the action in this sector is nothing like the raging mania of the 2000s, prices in many hot US markets are at all-time highs, while affordability is at or near an all-time low. And now rising mortgage rates are beginning to bite.

Pending Home Sales Reflect “Dispirited” Buyers

(Mortgage News) – Pending sales, which were widely expected to make a good showing in November, pulled back sharply instead. The National Association of Realtors® (NAR) said its Pending Home Sales Index (PHSI), a forward-looking indicator based on contracts for existing home purchases, declined 2.5 percent to 107.3 in November from 110.0 in October. NAR said “the brisk upswing in mortgage rates and not enough inventory dispirited some would-be buyers.” The decrease brought the PHSI to its lowest level since January of this year and it is now 0.4 percent below the index last November which stood at 107.7.

Analysts polled by Econoday had been upbeat about the November outlook. The consensus was for an increase of 0.5 percent with some analysts predicting as much as a 2.0 percent gain.

Lawrence Yun, NAR chief economist said, “The budget of many prospective buyers last month was dealt an abrupt hit by the quick ascension of rates immediately after the election. Already faced with climbing home prices and minimal listings in the affordable price range, fewer home shoppers in most of the country were successfully able to sign a contract.”

US Auto Sales

Cars and trucks have been one of the economy’s bright spots for several years — which seems to have gotten everyone just a little too excited. Auto financing practices have lately begun to resemble those of the subprime mortgage bubble: Today’s average loan is for more money, lasts much longer, and is held by a much weaker credit than ever before. Now, with interest rates rising and pretty much every potential buyer already locked into a car mortgage, the bubble optimism is evaporating.

GM Plant Closures Could Signal Trouble for U.S. Auto Industry

(NBC) – General Motors will temporarily idle five U.S. assembly plants next month in a bid to reduce bloated inventories.

The cuts focus on plants building sedans and coupes, such as the Chevrolet Cruze, Cadillac CTS and Chevy Camaro, which have been losing momentum as American motorists by the millions shift from passenger cars to utility vehicles and other light trucks.

But the move could also signal a broader slowdown of the U.S. automotive market after three consecutive years of record sales. The big questions are how fast and how far a slide the industry could be facing.

Forecasts by IHS Automotive and other research firms say sales could slide by 200,000 vehicles or more, with a variety of factors threatening to create even more of a downturn. These include rising fuel prices and increasing interest rates. Automakers could offset higher monthly payments by offering new loan and lease subsidies, but such moves would, in turn, impact industry profitability.

GM’s decision to cut production at plants in Michigan, Ohio, Kansas, and Kentucky comes as it watches inventories surge, in some cases, to nearly three times what the industry considers the norm: about 60 to 65 days’ worth of vehicles on dealer lots. The company has a 177-day backlog of Camaros, while its overall inventory grew from a 79-day supply in October to 84 days at the end of November.

China

That the world’s second largest economy — with a debt load that has quintupled in the past seven years — can be called a “mini-bubble” illustrates the size of the meta-bubble in which it has emerged.

The story in a nutshell is that China responded to the Great Recession by borrowing more money in the following half decade than any other country ever, and wasting a big part of the proceeds. Now its banking system is cracking under the strain of mounting bad debts, and newly-rich Chinese are getting their capital out of Dodge at a rate that if allowed to continue will bring on a full-scale credit crisis. Already-extant capital controls will apparently be tightened up shortly.

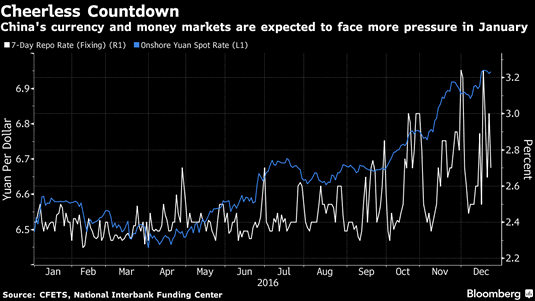

No Happy New Year in China as Currency, Liquidity Fears Loom

(Bloomberg) – China bulls could be facing a grim New Year’s eve.

China’s markets are seeing renewed pressure this month as the Federal Reserve projects a faster pace of rate increases for 2017 and its Chinese counterpart tightens monetary conditions to spur deleveraging and defend the exchange rate. The declines are capping off a tough year for investors during which bonds, shares and currency all slumped.

China’s 10-year government bond yield has surged 21 basis points in December, poised for its biggest monthly increase since August 2013, and its first annual gain since that same year, China bond data show. The yuan’s 6.6 percent decline in 2016 puts it on course for its worst year since 1994, while the Shanghai Composite Index is headed for its largest drop in five years.

The three-month interbank rate known as Shibor rose for a 50th day, its longest streak since 2010, to an 18-month high on Wednesday. The overnight repurchase rate on the Shanghai Stock Exchange jumped to as high as 33 percent the day before, the highest since Sept. 29. As banks become more reluctant to offer cash to other types of institutions, the latter have to turn to the exchange for money, said Xu Hanfei, an analyst at Guotai Junan Securities Co. in Shanghai.

The onshore yuan’s surging trading volume suggests outflows are quickening, according to Harrison Hu, chief greater China economist at Royal Bank of Scotland Group Plc. The daily average value of transactions in Shanghai climbed to $34 billion in December as of Wednesday, the highest since at least April 2014, according to data from China Foreign Exchange Trade System. The offshore exchange rate dropped 0.15 percent on Wednesday to trade near a record low, while the onshore rate was little changed.

None of these, not even China, are by themselves enough to destabilize a global financial system that’s still awash in new credit. But all three at once? Maybe.

And of course there are more potential eruptions waiting in the wings, what with the Italian bank bail-out getting harder as deposits flee those sinking ships and US stocks at record levels and thus (if – an admittedly big if – history is still a reliable guide) due for a correction.

So whether or not these current dramas amount to anything memorable, they clearly represent limits on the global financial bubble. More such limits will emerge shortly.

…related: More on crashing sovereign debt markets …