- In the wake of our Note on the importance of PMI data, I thought it would be beneficial to point out what I think the six most important data points to be released this week and why

MONDAY July 29th

With so much of American’s wealth tied up in their homes, today’s release of pending home sales (both month-over-month and year-over year) will be an important indicator of the relative health of the housing market in the US.

The fall in the monthly consensus number (-.1% from a previous monthly increase of 6.7%) is believed to be due to increasing mortgage rates in the US. Such a precipitous drop shows how sensitive consumers are to higher rates. The double digit gains on a YOY basis are due to the low rate environment manifested through the Federal Reserve’s near-zero interest rate policy and this is the number analysts are more focused on as it is more indicative of a trend.

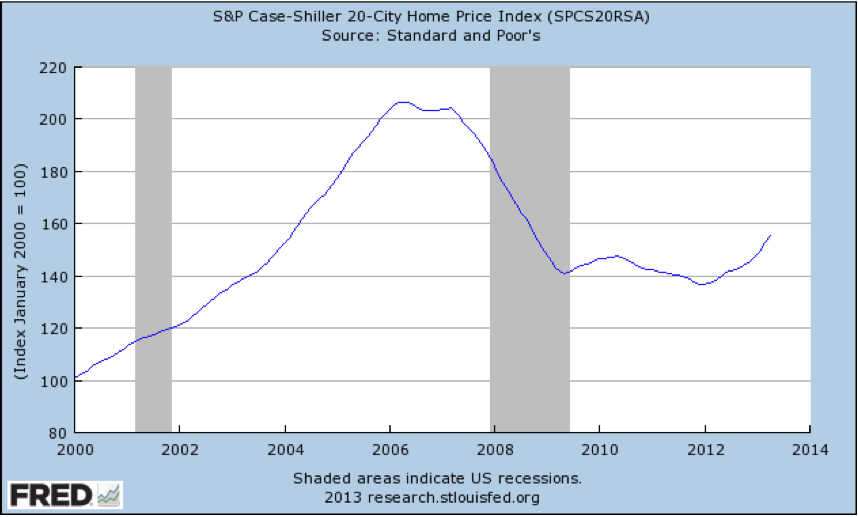

Though the housing market in the US has quite a hill to climb to regain its valuations pre-Great Recession (see chart below of the Case-Shiller 20 City Home Price Index), the recent strength in these (and other) housing market numbers has some cautiously optimistic.

TUESDAY July 30

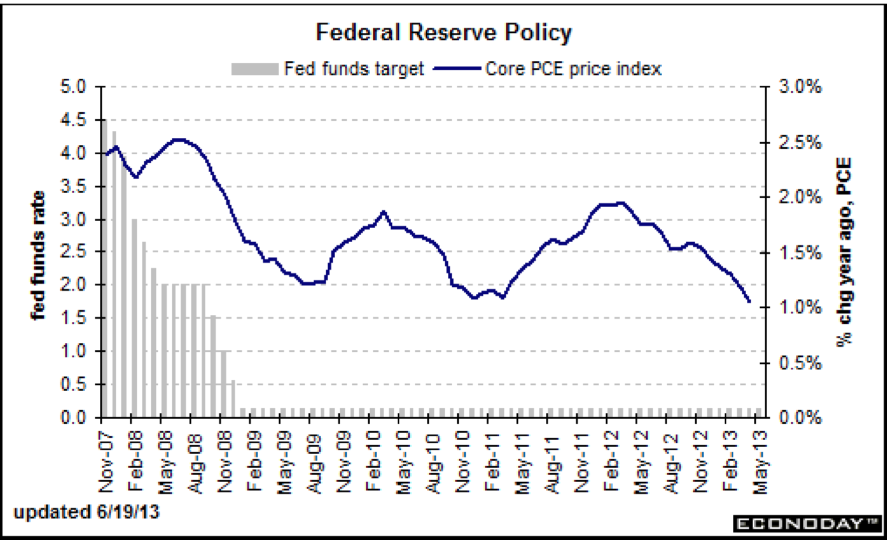

The Federal Open Market Committee (FOMC) begins its two day meeting today to debate the state of the US economy and hence, the direction of monetary policy, inflation, and prices. It’s no secret that the FOMC is split amongst the hawks who want to hasten an end to QE and raise rates and the doves, Chairman Bernanke among them, who want to keep rates in the US low for “an extended period”. The results of the two day meeting will be announced on Thursday. The chart below looks much more deflationary than inflationary and this is at the core of the debate at the FOMC. Short-term interest rates are expected to remain unchanged.

WEDNESDAY July 31

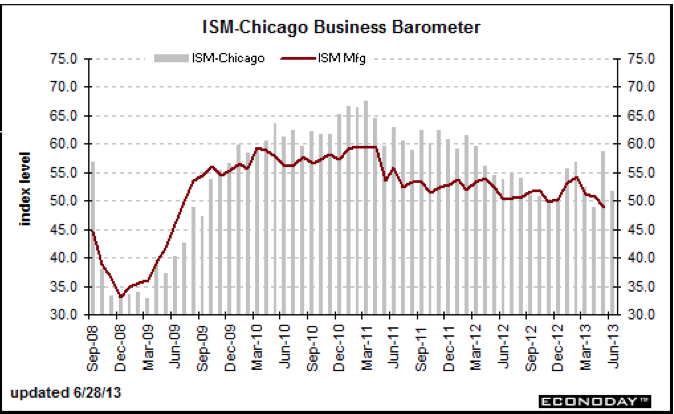

Two items of economic data of note today, specifically Q2 GDP and the June Chicago Purchasing Managers Index.

I discussed my affinity for PMI data in a Note last week, and with the US PMI data recently showing strength, the Chicago number will be watched to see if this trend can continue.

June’s number registered 51.6, down from the previous month, but still indicative of an expanding industrial base. The current forecast number is 54.

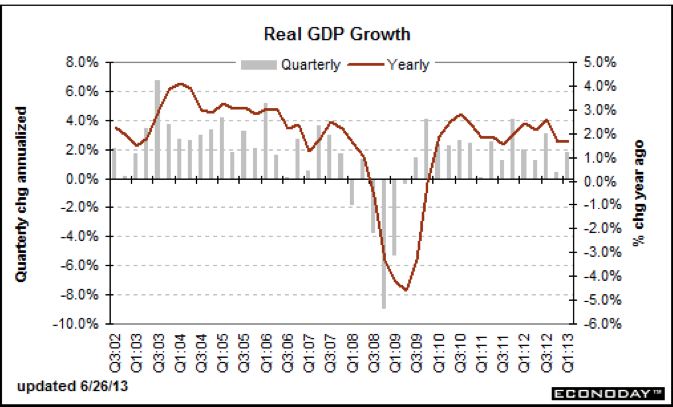

As for GDP,

the forecast looks somewhat less rosy as overall the US economy continues to “tread water”. The US economy grew at a rate of 1.8% in Q1 and the economy is forecast to grow by 1.2% in Q2 in the wake of recent downward revisions.

THURSDAY August 1

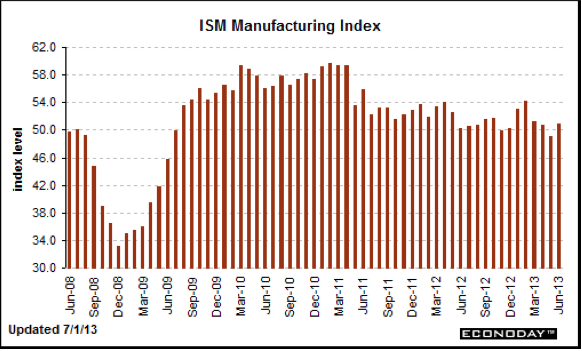

Today, the ISM Manufacturing Index is released and, like the PMI data before it, is forecast to show growth of 51.5 versus 50.9 in June. The ISM index is compiled by discussing a host of factors with purchasing managers from over 300 manufacturing firms in the US. According to Bloomberg, topics discussed include: the general direction of production, new orders, order backlogs, inventories, customer inventories, employment, supplier deliveries, exports, imports, and prices.

As a reminder, any reading above 50 is positive and a sign of increasing confidence within the manufacturing sector of the economy.

FRIDAY August 2nd

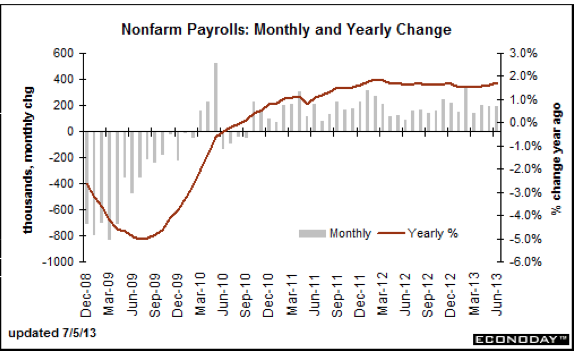

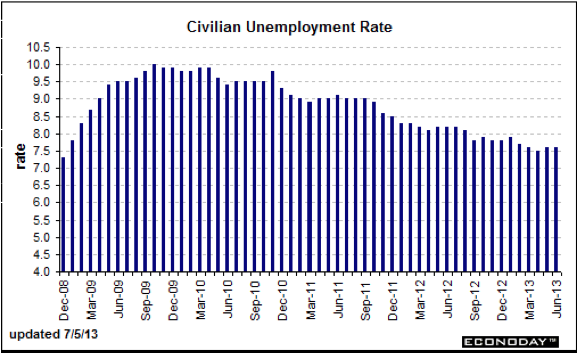

If the Rose Bowl is the “Grand Daddy” of College Football games, then today’s release of the monthly Initial Jobless Claims is the Grand Daddy of US economic data.

While I have reservations about this number and the unemployment rate in general including how the underemployed are accounted for and the “type”, or quality of job created, the impact that this number has on the financial markets cannot be ignored. I’ve said in the past I put more credence in past month’s claims numbers as they’ve been revised to portray a “truer” employment picture despite the flaws in how this number is calculated.

The unemployment rate is forecast at 7.5% down slightly from 7.6% and the non-farm payrolls are expected to increase by 175,000 down from 195,000 the previous month.

It is generally believed that a jobs number greater than 125,000 net new jobs per month is required to stay ahead of population growth and demographic changes in the US. This, however, is the subject of some debate. While the unemployment rate is still high by historic and structural standards, the job creation in the US economy, coupled with nascent strength in the housing market and manufacturing sector, have many believing in continued strength in the US in the second half of 2013 continuing into 2014.

The key will be the direction of interest rates and the health of the US consumer, as we have indicated before.

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual resultscoulddiffermateriallyfromthoseexpressedinanyoftheforwardlookingstatements. Suchrisksanduncertaintiesinclude,butarenotlimitedtofutureevents and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin. We own no shares in any companies mentioned.

MORNING NOTES 7/29/2013