THE STOCK MARKET OUTLOOK FOR JANUARY 17, 2014

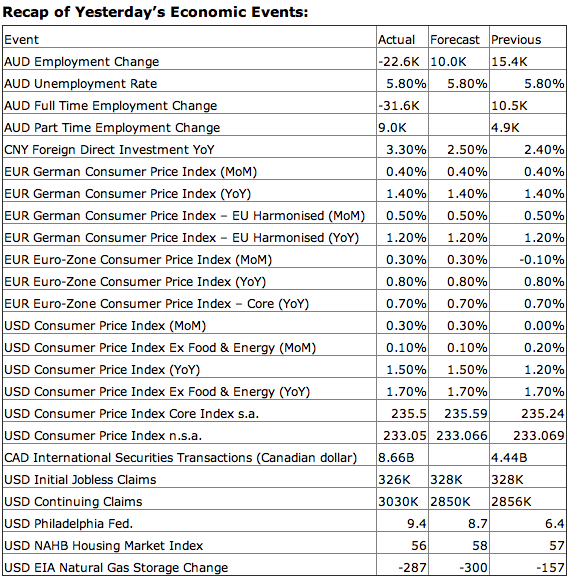

Upcoming US Events for Today:

- Housing Starts for December will be released at 8:30am. The market expects 0.985M versus 1.091M previous. Building Permits are expected to show 1.015M versus 1.007M previous.

- Industrial Production for November will be released at 9:15am. The market expects a month-over-month increase of 0.3% versus an increase of 1.1% previous. Capacity Utilization is expected to tick up to 79.1% versus 79.0% previous.

- Consumer Sentiment for January will be released at 9:55am. The market expects 83.5 versus 82.5 previous.

- Labor Department’s Job Openings and Labor Turnover Survey for November will be released at 10:00am. The market expects Job Openings to show 3.93M versus 3.925M previous.

Upcoming International Events for Today:

- Great Britain Retail Sales for December will be released at 4:30am EST. The market expects a year-over-year increase of 2.6% versus an increase of 2.0% previous.

- China GDP for the Fourth Quarter will be released on Sunday at 9:00pm EST. The market expects a year-over-year increase of 7.6% versus an increase of 7.8% previous. Industrial Production for December is expected to show an year-over-year increase of 9.8% versus an increase of 10.0% previous. Retail Sales for December is expected to show a year-over-year increase of 13.6% versus an increase of 13.7% previous.

The Markets

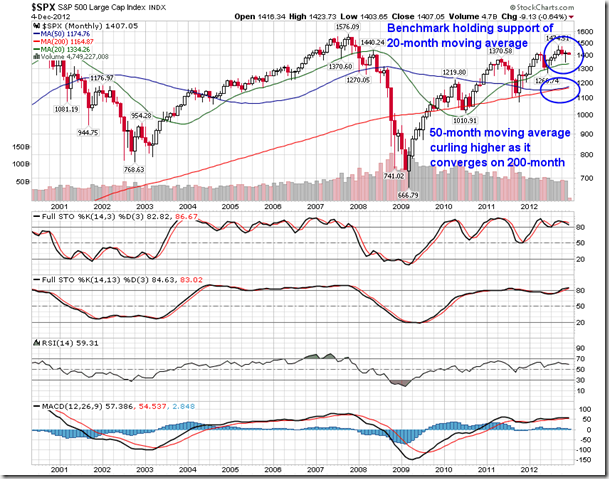

Stocks ended generally lower on Thursday as the financial sector dragged down the major benchmarks following lacklustre earnings results from Goldman Sachs and Citigroup. Shares of Citigroup and Goldman Sachs declined by 4.35% and 2.00%, respectively, falling back towards rising intermediate trendlines. Significant moving averages (20, 50, and 200-day) continue to point higher, implying positive short, intermediate, and long-term trends. Financial stocks, including Goldman Sachs and Citigroup, remain in a period of seasonal strength through to April.

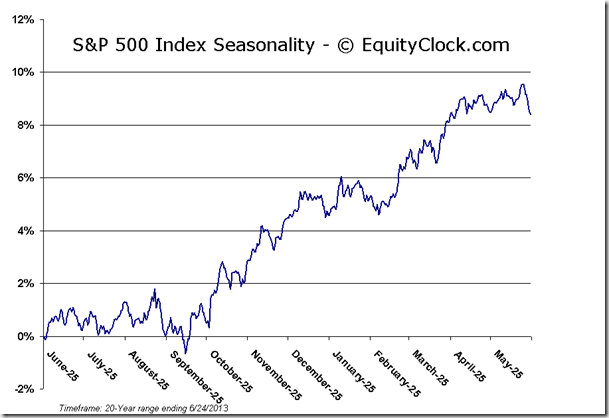

Thursday had all of the traits of a risk-off session: defensive sectors (Utilities, Health Care, and Consumer Staples) all posted gains on the day, gold posted marginally positive returns, and bonds ended higher on the day. One of the risks to the seasonal investing strategy over the next few months is that a period of risk-aversion materializes, whereby bonds, gold, and defensive equities outpace broad equity markets, forcing investor rotation from cyclical assets to alternate allocations. Seasonally, from late January through to the beginning of May, high-beta, cyclical equities typically dominate, posting gains on average and outperforming broad market benchmarks, such as the S&P 500. The iShares 20-Year Treasury Bond Fund (TLT) is giving the appearance of a significant double bottom pattern, suggesting a bounce from support may be underway, potentially drawing equity investors back to the fixed income asset class, perhaps for a brief period of time. Bond prices seasonally decline through to April as riskier assets attract investor demand, however, the path of least resistance for the bond market appears to be higher. A risk-off period doesn’t necessarily mean lower stock prices, but it could imply that some of the drivers of performance of broad market benchmarks may take a backseat role. Significant lag versus the market is already becoming apparent in the consumer discretionary sector, one of the best performing segments of the market for well over a year. The Consumer Discretionary sector remains in a period of seasonal strength that runs through to April.

And with sectors like Consumer Discretionary dragging on the broad market in the US, benchmarks outside of the US are showing signs of outperformance. The MSCI EAFE, which is essentially composed of international equities outside of North America, is starting to show signs of outperformance versus the S&P 500. Looking at a long term chart of the MSCI EAFE ETF (EFA) versus the S&P 500 ETF (SPY), the relative trend of EFA has been charting a significant base-building pattern since mid-2012, ending almost 5 years of relative declines that saw US stocks outpace the rest of the world. Opportunities outside of the US are starting to become apparent. The MSCI EAFE seasonally outperforms the S&P 500 from February through to April/May.

Seasonal charts of companies reporting earnings today:

Sentiment on Thursday, as gauged by the put-call ratio, ended bullish at 0.78.

S&P 500 Index

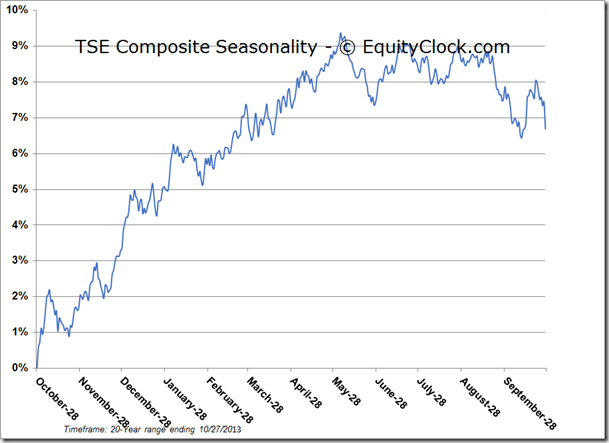

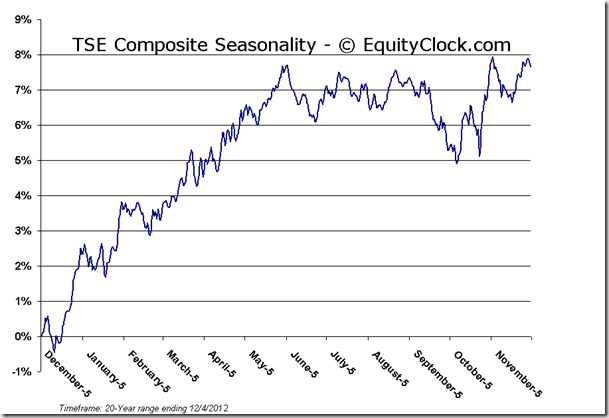

TSE Composite

Horizons Seasonal Rotation ETF (TSX:HAC)

- Closing Market Value: $14.32 (down 0.14%)

- Closing NAV/Unit: $14.33 (down 0.06%)

Click Here to learn more about the proprietary, seasonal rotation investment strategy developed by research analysts Don Vialoux, Brooke Thackray, and Jon Vialoux.

| Sponsored By… |

www.scotiabank.com/MutualFunds