Condensate is essentially a very light oil which is condensed from rich natural gas and solution gas from oil. And the price of it is skyrocketing, because it’s used to dilute both regular heavy and synthetic oil from the oilsands. It’s the saving grace for a lot of Canadian producers.

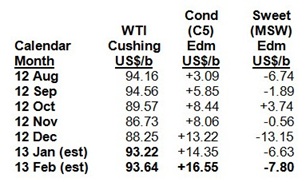

See this chart below. It shows Canadian condensate prices against WTI—see how the value of condensate is rising rapidly? In August 2012 it was only $3/barrel more than WTI. Now it’s $14 more—giving producers with lots of condensate even better economics than most oil producers!

And prices will only get better for condensate producers, one Alberta based oil and gas marketer told me, asking to remain anonymous.

“Supply and demand (for condensate) are just touching each other. Any more heavy oil coming onto market will have a big impact. We need to find other sources (of condensate).”

Or, he says, condensate prices could go even higher. He estimated that if the oilsands increases production by some 400,000 barrels per day (bopd) a year for the next several years, an extra 100,000 bopd of condensate is needed—each and every year.

I’ll explain in my next story, condensate part III, how US imports of condensate are happening, but not fast enough.

In Canada, most condensate is found in shale and tight gas formations. In the US, it’s mostly in gas associated with shale oil, especially the fast-rising Eagle Ford play.

In the United States, all this condensate is almost a problem. US refiners spent billions of dollars over the last decade to process more heavy oil. As a result they can’t really handle this light stuff.

But for Canadian gas producers, condensate is the only product that gives them substantial positive cash flow (a very few producers do make some cash flow on dry gas.) That’s why it’s so important to know how much condensate the gas producers are flowing.

Canada’s Thirst for Condensate

In the oil sands, condensate is used as a diluent to ‘thin down’ bitumen – a thick, sludgy substance – so it will flow through pipelines. Since bitumen production is climbing steadily, condensate demand is on the rise. Supply is struggling to keep up.

Canada now uses some 275,000 barrels of condensate per day as diluent. Canadian producers churn out 165,000 barrels per day (bpd), meaning oil sands operators already rely on imports to fill a 110,000-bpd gap.

That’s good, but it will probably get even better. Capital spending in the oil sands is expected to exceed $20 billion per year for the next five years. The more bitumen that is pulled from the sands, the more diluent Alberta will need to move all that heavy oil to market.

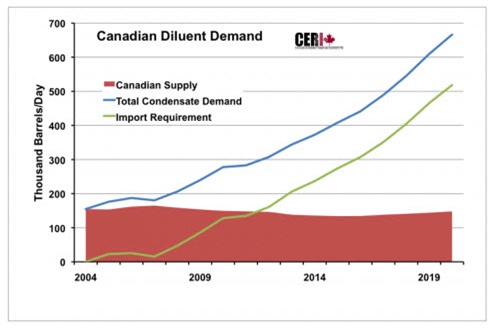

This year Canadian demand for condensate is expected to average 300,000 bpd. By 2020 demand is expected to reach 670,000 bpd, according to the Canadian Energy Research Institute, which also provided the following chart.

One issue is that Canadian NGL processing facilities are basically full. That is impacting (reducing) condensate production in the short term—creating further supply stress.

So Canadian producers are shipping in tanks directly to their wellsites, and trucking it to local markets; they’re not sending via pipe to processing plants (fractionation plants). The other reality is—and I’ve said this many times—the energy game is changing so fast in North America—fast rising production in both oil and gas, new channels to market (rail)—that nobody knows what the landscape is going to look like 2-4 years from now.

That uncertainty is causing Big Energy Money to be cautious about increasing refining capacity for oil and gas in Canada—which again, is good for commodity prices.

The second bottleneck is pipeline capacity INTO Canada.

The US is actually swimming in condensate–it accounts for as much as half of the output from US shale oil and gas basins. Refiners are buying some of it simply because it is cheap, but a condensate glut is also developing in the Lower 48.

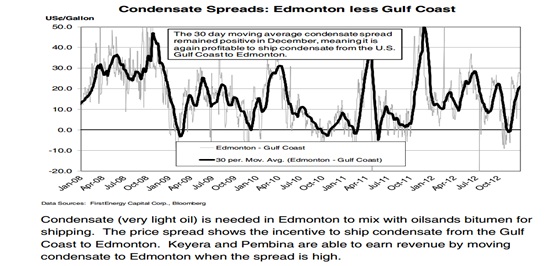

Now however, there is only Enbridge’s Southern Lights pipeline bringing condensate into Canada, and it’s not near enough. (There is some incoming condensate by rail, but now that is still small.) In Part II of this series, I’ll explain in detail this bottleneck, and what’s happening to get rid of it.

Once that glut starts moving into Canada apace, the price premium that Canadian condensate producers are currently enjoying will shrink. Condensate will still carry a good price, but the edge will be smaller.

But I expect that to be at least two years away, and if oilsands production keeps increasing, it may be even longer.

In conclusion—the growing demand for condensate in the oil sands is driving up its price. This isn’t just saving the lucky Canadian gas producers who have high condensate levels, it’s giving them better economics than most oil producers.

Pipeline bottlenecks in the US and processing plant issues in Canada should conspire to keep condensate prices high—making it the best (and least volatile) upstream commodity stories in North America.

Next, I’ll explain in detail what’s happening to condensate in the US, and the efforts to get as much up to Canada as fast as possible. In general, ‘fast’ means 2014 at the earliest, giving investors lots of time to benefit from strong domestic condensate prices.

Keith

P.S. I think mid-February is one of the BEST times for investors to discover my #1 condensate play in Canada. Learn all about my Top Pick risk-free right HERE.