On Thursday morning, whilst taping this week’s Audioblog, I discussed how overnight, the PMI Manufacturing reports in China, Japan and essentially all of Europe were not only miserable but well below expectations. Heck, even the PMI report in the United States of Economic Lies came in at just 54.7, down from 56.2 last month and well below expectations of an increase to 56.5. In fact, it was the lowest print in ten months, validating with this week’s slew of 4Q GDP estimate downgrades. Which, by the way, were predicated on myriad factors from weak exports, to declining capital investment and even “Polar Vortex 2.0.” In other words, a broad mosaic of data suggesting America is succumbing to its terminal debt addiction, amidst global economic weakness not inappropriately compared to the Depression.

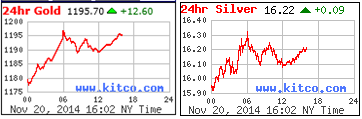

Consequently, the 10-year Treasury yield was on the verge of breaching the Fed’s current “line in the sand” at 2.30% yet again, whilst stocks were in danger of actually declining; and, for the third time this week, gold was about to take out $1,200/oz. (after having been turned back by “Cartel Herald” algorithms the prior two days, at exactly 6:00 AM EST).

Consequently, the U.S. government decided to go as “all-in” on economic data manipulation as Japan has with its hyperinflation strategy. To that end, recall when Forest Gump told the man at the bus stop that he owned the Bubba Gump Shrimp Company; to which, the man replied “Boy, I’ve heard some whoppers in my time, but that tops them all!” To a man, I’d be more inclined to believe Forest could be a CEO than what the government proclaimed this morning; i.e., the “Philly Fed” business conditions index not only rose significantly from last month’s reading of 20.7 but exploded to 40.8. In other words, a ten standard deviation “beat” of the consensus expectation of 18.0, whose theoretical odds occurring at just one in 1.5×10^23. And not only did this “survey” print its strongest reading since 199 but strongest new orders component since 1988!

I doubt anyone in the investment world believes that’s even remotely true, particularly as it not only contradicted the PMI report published just 15 minutes earlier but essentially every real data point imaginable. I mean in the past two weeks alone, it was reported that durable goods orders, factory orders, construction activity and industrial production declined in October, whilst retail sales rose a scant 0.3%. Throw in the aforementioned, grisly international data and it’s difficult to believe any increase occurred – let alone, of the magnitude this travesty of a report depicted.

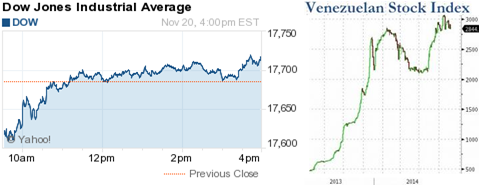

Of course, the “Dow Jones Propaganda Average” was treated to its 20th straight “dead ringer” algorithm – as it prepares to hyper-inflate, Venezuela-style.

However, a funny thing happened in the world of “recovery”; as not only did Treasury yields decline, but closed just three basis points from the aforementioned “line in the sand” the Fed is so terrified of. After all, it borders on comical that the Fed is pretending to consider rate hikes – even if not for a “considerable time” – when rates are plunging. Let alone, when rate declines occur as their data cookers purport the “best economic conditions” since 1993; and oh yeah, the “stock market” is trading at record highs.

Better yet, despite relentless capping and attacking – no less, with the potentially Cartel-destroying Swiss referendum just ten days away; gold and silver not only recovered yesterday’s Cartel orchestrated losses, but closed at the day’s highs – setting up gold for a fourth attempt to take out $1,200 in four days. Could we actually have three straight strong Friday’s – which frankly, NEVER happens? Much less with the Swiss referendum next Sunday?

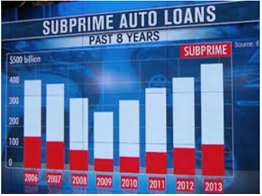

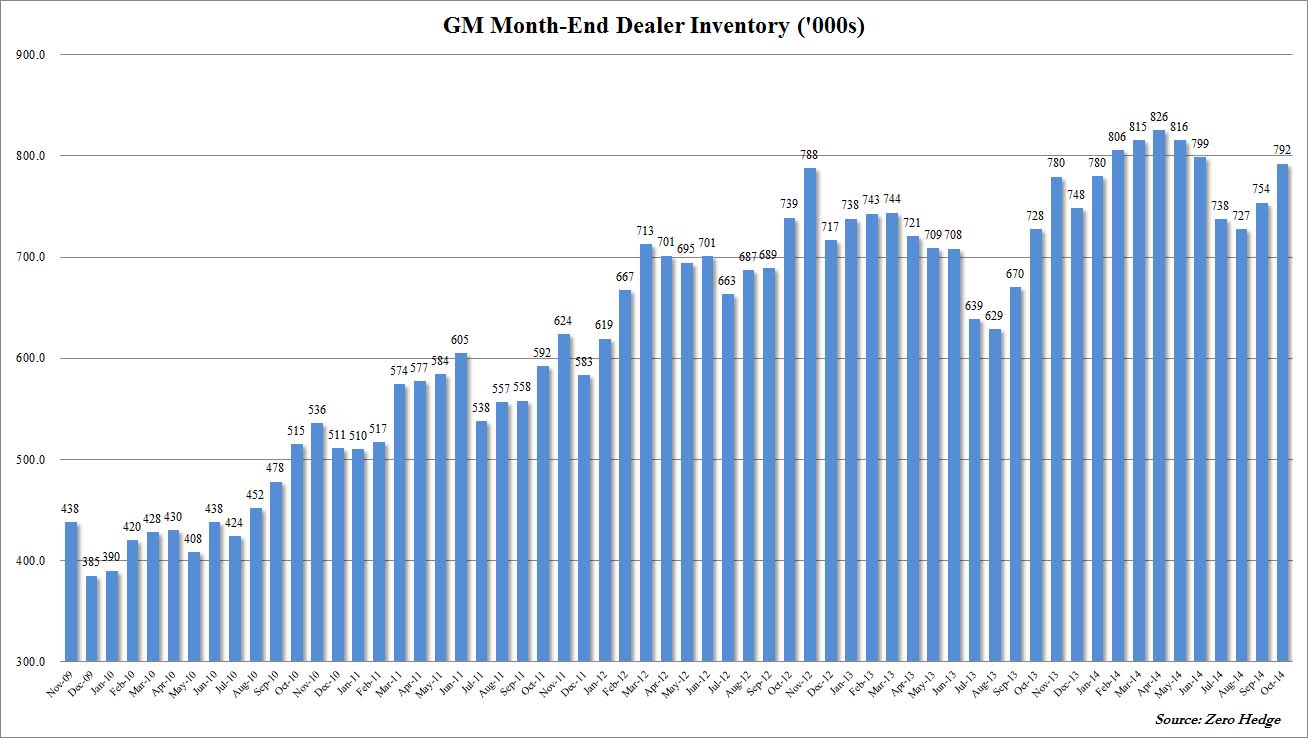

For some time now, we have discussed how the “propaganda leg” of the “evil tripod” of money printing, market manipulation and propaganda is permanently broken. In other words, no matter what propaganda is reported, the world is starting to realize the true state of the U.S. economy. For example, auto sales cannot be characterized as “strong” when they are either leases or subprime loan financed; let alone, amidst an environment of record “channel stuffing.”

Zero Hedge

Better yet, the “sentiment” of trade organizations like the National Association of Home Builders has as much credibility as a fox in a henhouse; particularly when it explodes to multi-year highs when both home sales and housing starts (in the latter case, principally rental units) remain at recessionary levels.

And thus, the issue of the boy who cried wolf. At some point, people stop listening; and in this case, global fixed income and commodity markets decidedly aren’t buying America’s “recovery” propaganda. Not to mention, the physical gold and silver markets, which are both experiencing record demand. Given the reality that “Economic Mother Nature” is revealing, it won’t be long before the money printing and market manipulation “legs” break as well. And when they do, if you haven’t already protected yourself with real money, you may never get the chance; certainly, not at prices anywhere near today’s historically suppressed levels.

{kind=link}

{kind=link}