Short term risk in North American equity markets remains following the technical meltdown on Friday. However, equity markets already are deeply oversold. Downside risk is not substantial. Unfortunately, upside potential also is not significant. Look for lots of volatility during a base building period lasting until mid-July when “difficult” second quarter earnings reports are released. Thereafter, intermediate prospects are expected to improve. Be patient!

Other Issues

The VIX Index popped 4.90 (22.52%) last week. The Index recovered from the top of a reverse head and shoulders pattern. On Friday, it broke above its 200 day moving average. Short term momentum indicators are overbought, but have yet to show signs of peaking.

Economic news this week is expected to be mixed and is not expected to have a significant impact on equity markets.

Earnings news this week is not significant.

Macro events will continue to impact equity markets. Once again, the focus is on Europe. Comments by Federal Reserve Chairman Ben Bernanke later this week also will be watched closely. Is Quantitative Easing III on the radar screen? Traditionally, the Fed has not made significant policy changes during four months prior to a Presidential election date. That means Fed action, if occurring, is likely to be announced before the end of July.

Headline risk is exceptionally high. The media extensively warned about a slowing U.S. economy over the weekend. The politicians on both sides of the political spectrum also were notable for their comments in the media over the weekend.

Intermediate technical indicators, most notably the break by U.S. equity indices below their 200 day moving averages, suggest that the intermediate uptrend remains downward.

Short term technical indicators for most equity markets and sectors are oversold, but have yet to show signs of bottoming.

Seasonal influences for most equity markets, sectors and commodities in the month of June are negative.

Currency trends will continue to impact equity markets. The U.S. Dollar Index is short term overbought and the Euro is short term oversold. Both recorded interesting reversals on Friday. Gold quickly responded. Will there be follow through this week?

Cash on the sidelines remains substantial. Cash hordes held by Corporate America remains high. Major commitments of cash are unlikely until the market determines the next U.S. president.

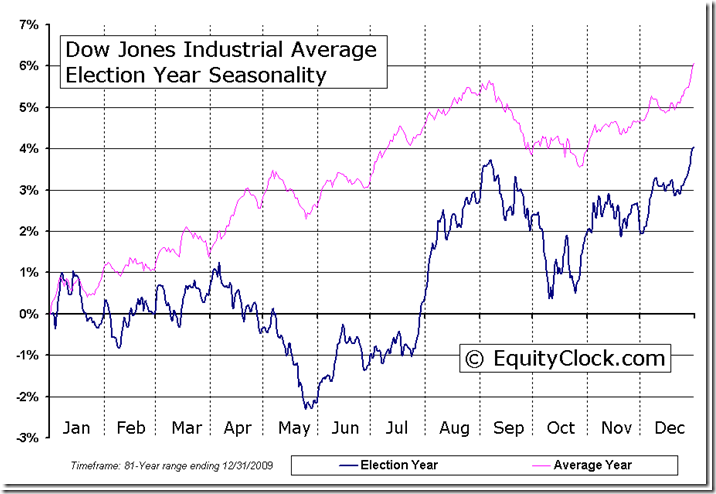

The historic pattern for U.S. equity markets during a Presidential election year were altered slightly last week when broadly based U.S. equity indices broke to new lows.

….read more of Don’s Brilliant Monday compilation of 45 Charts and commentary HERE