The Bottom Line

A surprising quiet week for U.S. equity indices and most sectors following early strength on Monday! Most indices were up or down slightly, typical of markets that have lost momentum after a major upside move. Preferred strategy is to accumulate sectors and markets with favourable seasonality on weakness in order to take advantage of the October 28th to May 5th period of seasonal strength.

The Markets

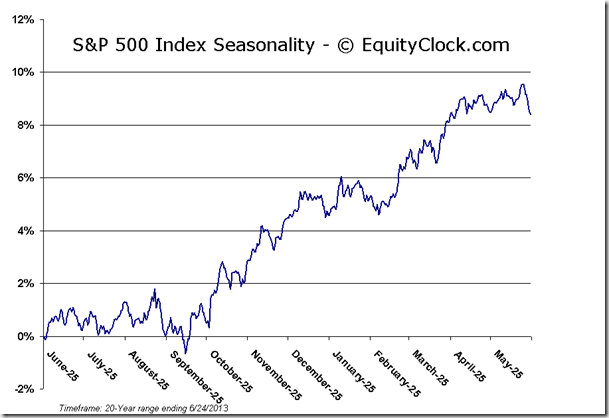

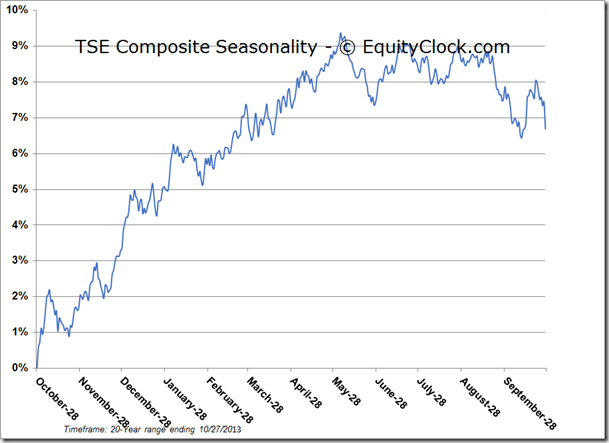

Welcome to the favourable six months of the year for equity markets. Today, October 28th, marks the average optimal entry date for equity positions to take advantage of the period of strength for stocks that runs through to May 5th of next year. Gain for the S&P 500 Index over this period, from October 28th through to May 5th, averages 8.53% with positive results realized in 16 of the past 20 periods. Results are consistent for Canadian equities with the TSE Composite averaging a gain of 8.87% over the past 20 years. Positive results were realized in 17 of the past 20 periods. During this favourable season for equities, through to the end of the year, bonds and commodities can continue to perform well, however, returns are typically less than stocks, making the equity market more attractive as risk-on plays dominate portfolio allocations.

Equity markets have already returned substantial gains over recent weeks, pushing benchmarks into overbought territory as the seasonally strong period for stocks begins. Overbought conditions on the October 28th average optimal date are fairly rare, based on an analysis of the past 50 years of data. The S&P 500 has been overbought on October 28th only 8 times, making entry points into equity positions extremely challenging. Equity benchmarks, such as the S&P 500 Index, offered more enticing entry points 6 of the 8 times within a few weeks following the average optimal date as stocks traded off of their overbought highs. Strategically allocating funds to equities upon any sort of weakness over the next few weeks continues to make sense, ideally once overbought conditions have concluded. Next short-term seasonal low for equity markets typically occurs on November 18th, on average.

….view more seasonal charts HERE

Economic News

September Industrial Production to be released at 9:15 AM EDT on Monday is expected to increase 0.3% versus a gain of 0.4% in August. September Capacity Utilization is expected to increase to 78.0% from 77.8% in August.

September Retail Sales to be released at 8:30 AM EDT on Tuesday are expected to slip 0.1% versus a gain of 0.2% in August.Excluding auto sales, September Retail Sales are expected to increase 0.2% versus a gain of 0.1% in August.

September Producer Prices to be released at 8:30 AM EDT on Tuesday are expected to increase 0.2% versus a gain of 0.3% in August. Excluding food and energy, PPI is expected to increase 0.1% versus a gain of 0.0% in August.

Case Shiller August 20 City Home Price Index to be released at 9:00 AM EDT on Tuesday are expected to show a year-over-year gain of 12.4% versus an increase of 12.0% in July.

August Business Inventories to be released at 10:00 AM EDT on Tuesday are expected to increase 0.2% versus a gain of 0.4% in July

October Consumer Confidence to be released at 10:00 AM EDT on Tuesday is expected to slip to 75.0 from 79.7 in September.

October ADP Employment to be reported at 8:15 AM EDT on Wednesday is expected to fall to 150,000 from 166,000 in September.

September Consumer Prices to be released at 8:30 AM EDT on Wednesday are expected to increase 0.1% versus a gain of 0.1% in August. Excluding food and energy, CPI is expected to increase 0.1% versus a gain of 0.1% in August.

FOMC Decision on interest rates is scheduled to be released at 2:15 PM EDT on Wednesday

Weekly Jobless Claims to be released at 8:30 AM EDT on Thursday are expected to decline to 340,000 from 350,000 last week.

Canadian August GDP to be released at 8:30 AM EDT on Thursday is expected to increase 0.2% versus a gain of 0.6% in July.

October Chicago Purchasing Manager’s Index to be released at 9:45 AM EDT on Thursday is expected to slip to 55.0 from 55.7 in September.

October ISM to be released at 10:00 AM EDT on Friday is expected to fall to 55.0 from 56.2

…read Don Vialoux’s full Monday report HERE