The Bottom Line

Downside risk exceeds upside potential in equity markets during the next six weeks. The breakout by the S&P 500 Index last week implies that depth of the downside risk is less than previous. Selected seasonal trades continue on the upside (gold, energy, software) and downside (transportation). However, many of these seasonal trades reach the end of their period of seasonal strength this month. September is a month of transition. Trade accordingly.

Equity Trends

The S&P 500 Index gained 26.79 points (1.90%) last week. Intermediate trend is up. The Index broke above resistance at 1,426.68 to reach a four year high. The Index remains above its 50 and 200 day moving averages and moved above its 20 day moving average. Short term momentum indicators have rebounded to overbought levels.

The TSX Composite Index added 185.78 points (1.54%) last week. Intermediate trend is up. The Index broke above resistance at 12,196.77 on Friday. The Index remains above its 50 day moving average and moved above its 20 and 200 day moving averages last week. Short term momentum indicators have recovered to overbought levels. Strength relative to the S&P 500 Index has changed from negative to at least neutral.

Seasonality refers to particular time frames when stocks/sectors/indices are subjected to and influenced by recurring tendencies that produce patterns that are apparent in the investment valuation. Tendencies can range from weather events (temperature in winter vs. summer, probability of inclement conditions, etc.) to calendar events (quarterly reporting expectations, announcements, etc.). The key is that the tendency is recurring and provides a sustainable probability of performing in a manner consistent to previous results.

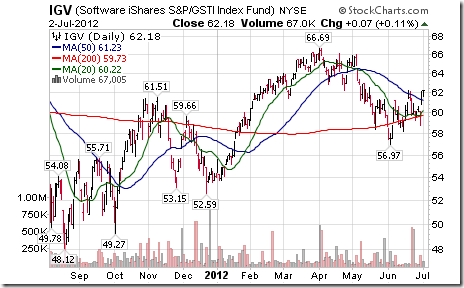

Identified below are the periods of seasonal strength for each market segment, as identified by Brooke Thackray. Each bar will indicate a buy and sell date based upon the optimal holding period for each market sector/index.

….go HERE to view Equity Clock’s Seasonality Chart for 26 other individual sectors, Commodities, Bonds etc.

Other Issues

Two unexpected events last week triggered a surprising upside move in equity markets last week, China’s $150 billion fiscal stimulus package announced on Thursday night and the ADP report showing a gain in U.S. private employment in August instead of a loss. Gains were muted on Friday when the less than expected U.S. employment report was released.

The economic focus this week is on the FOMC meeting. The Fed widely is expected to announce an additional monetary stimulus program that probably will include the purchase of mortgage backed securities by the Fed that effectively will replace Operation Twist that is expected to expire at the end of the month. However, the effectiveness of a new program is somewhat suspect. At best, it may reduce mortgage rates slightly, but mortgage rates already are near all-time lows. Importance of an additional monetary stimulus program is psychological (Investors relate monetary stimulus to higher equity prices). If the Fed chooses not to introduce another stimulus program, equity markets are vulnerable to significant short term downside risk. If the Fed chooses to go beyond a token purchase (or promise to purchase) mortgage backed securities, equity markets will move higher. The Fed in order to show political neutrality is unlikely to act beyond the September FOMC meeting until after the election.

U.S. economic news other than the FOMC meeting is expected to be neutral to slightly bearish for equity markets this week (higher trade deficit, higher inflation, higher inventories, lower consumer sentiment, but continuing strength in retail sales).

Macro events outside of the U.S. once again focuses on China this weekend and Europe later this week. Negotiations between ECB President Draghi and Greece continue on Tuesday. The German constitutional court rules on the eligibility of ECB lending on Wednesday. The Netherlands holds parliamentary elections on Wednesday.

Short and intermediate technical indicators for most equity markets and sectors improved last week but have returned to overbought levels.

North American equity markets have a history of moving lower from September to mid-October during a U.S. Presidential election year(particularly when polls show a tight race as indicated this year). Thereafter, equity markets move higher.

Cash on the sidelines on both sides of the border is substantial and growing. However, political uncertainties (including the Fiscal Cliff) preclude major commitments by investors and corporations before the Presidential election.

….read more & view 50 charts on Commodities, Interest Rates, Currencies HERE