Watching the rise in US long-bond yields got me to wondering: What if the fall in the Japanese and Chinese current account surpluses continues, i.e. this trend is for real?

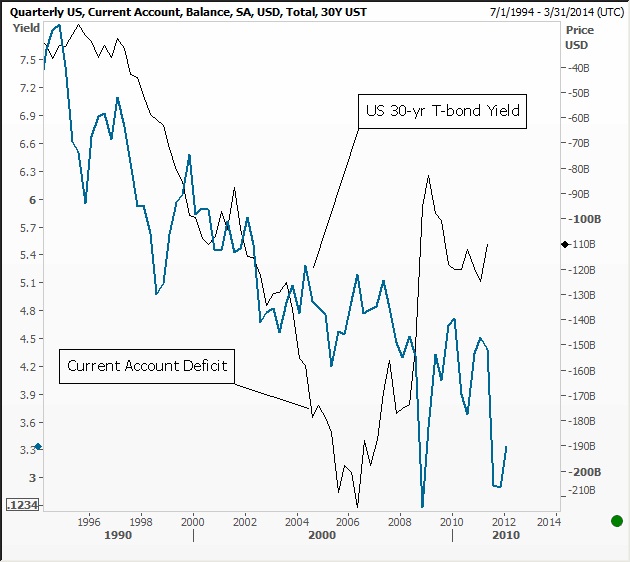

US Current Account Deficit (black) vs. 30-yr US Treasury Bond Yield (blue):

If so, it means both countries recycle less of their yen and yuan, respectively, back into the US capital markets. It means the global economy could finally see some rebalancing between the major deficit country, the US and surplus country, China. It means the US current account deficit, which seems to worry many people and economists alike, is likely to improve, as Japan and China morph increasingly into capital importers instead of capital exporters.

Has this rebalancing begun? We don’t know yet. But interestingly, given the needs for Japan to rebuild and China to change its growth model, it could very much be the next major global macro trend for the global economy. If so, there are three major implications, and several investment themes spawned:

Has this rebalancing begun? We don’t know yet. But interestingly, given the needs for Japan to rebuild and China to change its growth model, it could very much be the next major global macro trend for the global economy. If so, there are three major implications, and several investment themes spawned:

1) US long bond yields have likely bottomed (price topped), and

2) The next major growth phase for the global economy will be the rise of the Asian Consumer.

3) Global capital and trade flow will become a two-way street.

Some additional comments:

-

Japan may be morphing into a capital importer (first year-on-year trade deficit since 1980 was recorded in 2011). Interestingly, the tsunami and its devastation may have been the catalyst that leads to a normalization of the Japanese economy, i.e. rising interest rates, local commercial bank lending, and local business investment.

— Because of Japanese nuclear power going offline, Japanese imports of crude oil is up 350% compared to the same month last year.

— Normalization is part and parcel to a weaker yen as the game of risk aversion and “hiding” large pools of capital goes away.

-

China’s GDP growth will likely continue to fall (inherently reducing its giant reserve surplus), but this will not likely be a disaster if China’s growth model changesto support consumers (enriched consumers don’t care about GDP numbers; they care about reality) and moves away from State Owned Enterprises, which includes massive capital investment projects and consistent export subsidies of companies operating in the red or on wafer thin margins.

— No need to recycle surpluses and keep buying US Treasuries in order to keep the currency suppressed, because …

— A stronger yuan will increase consumer wealth, relatively, making the transition to a new model more efficient, i.e. benefiting import industries at the expense of exporters.

-

Asian-block countries will be relieved if China signals it is serious about making a transition that empowers its consumers. Asian-block nations who have implicitly and explicitly suppressed the value of their own currencies over the last several years thanks to China’s explicit currency suppression and growth model. Asian-block countries compete against China for the same Western demand. Thus, in the process of that competition, consumer market development across Asia as a whole has been stymied. Thus, China’s signaling of a change in its local growth model will likely be reinforced strongly across the region.

-

Stronger Asian consumer demand and stronger Asian currencies mean Western consumer goods flow more freely to the East and the US trade balance improves dramatically, and it will be quite good for Europe too. Thus, the US trade balance and need for external capital to close the current account gap will decline naturally as Asian consumer demand increases.

Risks to this rosy long-term scenario are many; here are just a few examples:

-

Contagion to emerging markets triggered by the European debt crisis could be severe …

-

Potential financial crisis in China as debt grows to dangerous proportions and unrest is met with more internal crackdowns on its citizens …

-

A major debt crisis in Japan, triggered by its need to import funds, but inability to see long-term interest rates rise (which is part and parcel to attracting funds from international investors) …

-

US remains mired in its seemingly “never-ending” war policy and do little to improve its unsustainable fiscal deficits …

Net-net if this major trend plays out, it means the US may avoid its fiscal train-wreck destiny and paradoxically if Chinese leaders trust their average citizens more, they will gain even more control of their own destiny.