I divide my participation in the markets between my short term trading accounts and my long term savings accounts. I use my short term trading accounts to move in and out of the futures and options markets with positions that I may hold for a few days to a few months. I try to earn trading profits with these accounts but I also see this activity as “keeping my hand in” as I try to gauge what is going on day-to-day in the markets (See Charts Section below.)

My objective with my long term savings accounts is capital preservation and for the past couple of years I’ve been very conservative…mostly in cash…as I’m far more interested in hanging onto that money than in trying to earn a couple of extra percentage points by reaching for yield. My short term trading accounts and my long term savings accounts constitute ~95% of my net worth. Over the past couple of years I’ve diversified my currency exposure by swapping ~25% of my net worth into US$ at an average of ~9700 USDCAD.

I’ve also been pretty conservative with my short term trading accounts. I rarely use leverage and the manic-depressive mood swings of the markets have kept me defensive. Over the past few months I’ve realized that I have little ability to handicap the short term European political response to their growing debt crisis…and thus little ability to anticipate the risk-on/risk-off price swings that result from changing perceptions of the European political theater.

My long term view of what is happening in the world makes me comfortable to have my savings largely in cash. I think we’ve had a 30 year credit boom, the greatest in human history, and that produced a great boom in asset prices and a great willingness, by both borrowers and lenders, to finance risk. I think we are now in a major reversal of that 30 year credit boom, and that this reversal will play out over several years as leverage is wrung out of the markets. Assets that boomed the most on debt financing will likely fall the most as leverage is reduced. To quote Gary Shilling, we are in an “Age of Deleveraging” and I anticipate that deleveraging will grind on relentlessly, regardless of the rearguard actions of central banks and governments.

Perhaps one of the most painful consequences of “Way more money has been borrowed than will ever be repaid” is that “Way more promises have been made than will ever be kept.” It seems to me that politicians of all stripes will try to avoid or deny this problem….but the math is overwhelming…some promises are going to be broken…and some people are going to get hurt as a result of that.

The world economy seems to be falling back into a recession, or worse, as the deleveraging process continues…markets are pricing that in…weak credits have to pay more to borrow money while stronger credits pay less. Commodity prices remain under pressure. Increasing stress on the financial system seem likely to change our world in ways that we haven’t anticipated…and may be poorly prepared to deal with….for instance we will likely see widespread “new arrangements” for pension payouts.

My default position when I look at financial markets is skeptical…I don’t think of myself as a pessimist…but rather as a realist anticipating the inevitable consequences that come after 30 years of irrational exuberance – financed with other people’s money! I expect that one of the key social divides in our not-so-distant future will be “Who is going to pay?” Who is going to have their “entitlements” cut? Who is going to have their “taxes” raised?

Charts Section

(Note: I’m not a trading advisory service. I’m not going to detail my personal trades…but here are a few charts that I find interesting…)

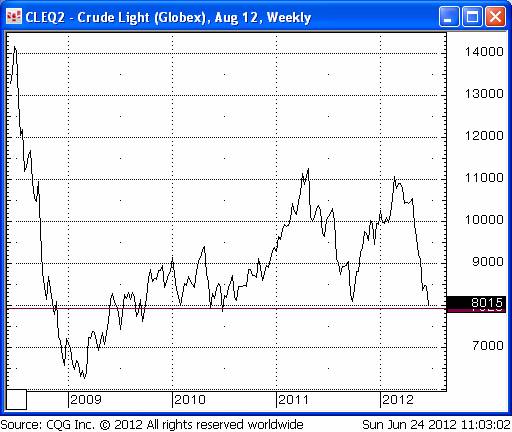

Crude: Short term oversold? Prices are at key support. Decline since Feb. anticipating global economic slowdown / reduced Iran tensions / increasing crude production / and maybe, “substitution” of crude demand with Nat Gas?

Gold: A test coming of key support levels ~ $1525/35? Downtrend from last September highs looks powerful

Silver: Right at key support levels…I’d expect a break below $25.

Silver/Gold ratio: continues down from Key Turn Date May 2, 2011. Not positive for “risk” trades.

LME Aluminium: Often over-looked relative to copper. But it grinds lower from Key Turn Date May 3, 2011. Hearlding global economic slowdown?

US Ten Year Note: Did we finally make a top in a 30 year bull market in bonds? Maybe…but selling powerful up-trends is rarely a profitable strategy!

But it is interesting to note on the daily charts that the recent Turn Date of June1/June 4 remains intact and that TNote prices had their lowest close in a month even as the S+P reversed sharply from resistance this past week…

Japanese Yen: the Yen had its lowest close in nearly two months and the recent June 1/ June 4 turn date remains intact. Is the Yen finally starting its long predicted downtrend?

vadair@union-securities.com“>vadair@union-securities.com