Technically, we now have something quite clear.

INSTITUTIONAL ADVISORS

FRIDAY, SEPTEMBER 27, 2013

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The following is part of Pivotal Events that was

published for our subscribers September 19, 2013.

Overdose of Kool-Aid

The last two quotes show the absurdity of intellectual theories bereft of market history. In 2007 the establishment boasted that with the “Dream Team” at the Fed nothing could go wrong. Now the same establishment that could have anticipated the bust claims not to understand it. And then there is this week’s tout that the Fed still has some “Heavy-Caliber Ammunition”.

If it wasn’t so pathetic it would be disgusting.

The ability of the Fed to get its portion of a credit expansion “out the door” depends upon a big speculative bid from the private sector. Until May the big play was in lower-grade bonds. This is no longer the case, but through the summer stocks and crude oil have been strong. Yesterday, Bernanke announced that the bond-buying program would continue until unemployment met some arbitrary number. In so many words, he renewed his vows to keep trying to depreciate the dollar.

Markets vigorously responded to the Fed in its role as a catalyst.

* * * * *

Stock Markets

Sunshine likely in September has continued with “Benny Bucks” Bernanke providing an almost universal catalyst.

As they saying goes, “When the Fed is the bartender everyone drinks until they fall down”. More than likely it is an overdose of Kool-Aid.

Technically, we now have something quite clear.

The rally from S&P 1627 in late August made it to 1705 on Tuesday. Yesterday’s news popped it to 1726. Overall this is a multi-index spike up with both the DJIA and S&P reaching a limiting level on the Daily RSI.

This year’s strength drove the Weekly RSI to a higher level for a longer time than accomplished going into the 2007 high. And now at 73 the Daily RSI has exceeded the 66 accomplished in October 2007.

The RSI provided negative divergence on that important peak. A loss of momentum now would accomplish just such a divergence.

What also caught our eye was the reversal in Broker Dealers (XBD). Although this is a volatile and at times precarious sector it has been virtually a “one-way-street” since turning around late last year.

This thing does big and long overboughts on the way up. And at the high in 2007 a couple of rallies reached 70 on the Daily RSI.

For this year, the weekly has accomplished the longest run of very overbought in years. It ran from February to May. Since August there has been two thrusts to 70 on the Daily RSI.

Yesterday, Broker-Dealers (XBD) sold off in the morning and jumped from 140.2 to 141.5 on “the news”. This was up on the day, but in only a few minutes it gave it up. At the end of the day it was down almost 1 percent, setting an Outside Reversal.

It is a warning.

And so is the huge volatility in the gold/silver ratio, which will be detailed below.

Currencies

The dollar index was also volatile as it slumped with Bernanke’s statement.

This drove the DX below support at the 81 level to support at the 80.5 level. This slumped the Daily RSI to 33, which compares to 30 reached with the June plunge.

The ETF is UUP and the RSI declined to 30 yesterday, which compares to 28 set with the low in June. Momentum is at 33 today suggesting a reversal, which in turn suggests a positive divergence.

Last Thursday’s ChartWorks updated the bigger picture on currencies and noted that the euro was showing distribution. This indicates dollar accumulation, which is constructive.

Of course with dollar depreciation considered as the best policy ever and at any time, a rising dollar would be the worst thing that could happen.

Get prepared for the “worst” to happen.

This along with the overbought stock market at this time of year, as well as the outstanding four-year bull market, suggests the financial markets are precarious.

A firming dollar next week would provide confirmation.

The Canadian dollar rallied from 95 in late August to 98 yesterday, which represents serious resistance. The Daily RSI jumped to 68, which ended the past two rallies.

The C$ is heading to support at the 94 level.

Credit Markets

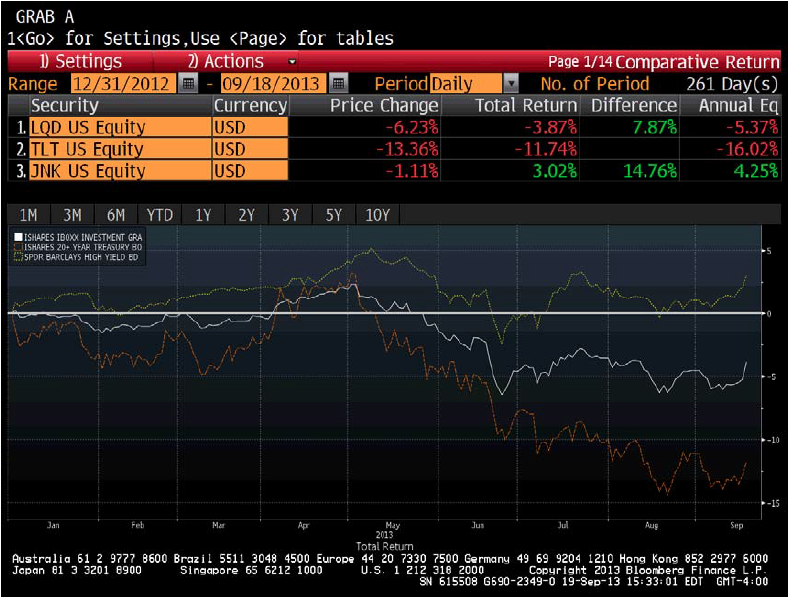

The action in lower-grade bonds suffered a “mini-panic” following the expected reversal in May. The EMB crashed to 99.4 in late June, which was exceptionally oversold. The rebound run out in mid-July at 111.18 and the price declined to 104.60 two weeks ago. The rebound started then and the Bernanke pledge popped the Emerging Bonds to 111.15 yesterday.

Clearly, this is at significant resistance and the Daily RSI reached 72 yesterday. This has accomplished a huge swing from extremely oversold to enough of an overbought to end the move.

Much the same holds for JNK, HYG and MUB.

The reversal in the huge bond market in May ended one of the greatest speculations in lowergrade bonds – ever. Once the natural reversal was in, we expected some churning around through the summer. This would lead to a more severe hit later in the year.

This week’s zoom to an overbought condition seems a timely setup to disorderly markets.

Traders can return to playing the short side and investors should focus upon 3 to 4-year AAA corporates.

Considering the possibility of a firming dollar, this position should be attractive to off-shore investors.

North American bond markets have been corrupted by the US administration and world bond markets by all central bankers, particularly the Fed. Individual investors have been uniquely forced to reach for yield.

At some point spreads will reverse to widening.

Link to September 20, 2013 ‘Bob and Jim Show’ on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2013/09/any-chance-of-a-black-october/

All One Bond Market

- Long-dated treasuries (TLT) zoomed up to a spectacular peak in July 2012.

- Despite considerable buying by the US Treasury the bear market prevailed.

- Investors could be concerned about US (or should we say Chicago?) credit worthiness.

- Although the important price-swings have been coordinated, treasuries have been a relative disaster.

- Earlier in the year, we discussed that part of a post-bubble contraction has been the Great Bond Revulsion, which occurs as the street realizes that all of the debt cannot be serviced.

- The next step in the “revulsion” could begin in a few weeks.

- Investors could find a haven and some return in 3 to 4-year Prime Corporates.

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com