Quotable

What’s past, and what’s to come is strewed with husks

And formless ruin of oblivion

William Shakespeare, Troilus and Cressida

Commentary & Analysis

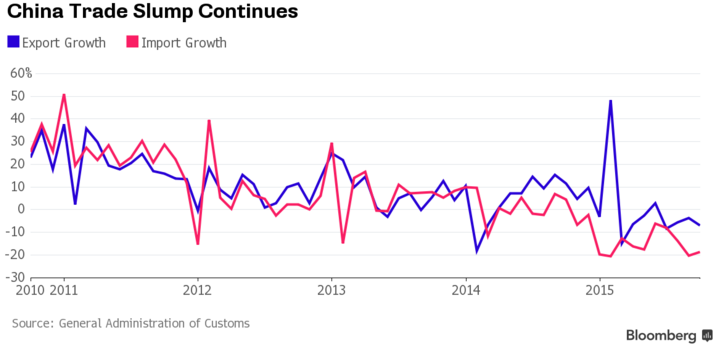

Latest China export news likely not good for commodity currencies

News today of slower than expected exports from and imports into China likely doesn’t bode well for commodities, or commodity currencies. From The Wall Street Journal, my emphasis:

BEIJING—China’s exports fell in October for the fourth consecutive month, as a once-powerful engine of the country’s growth continued to sputter in the face of weak global demand.

The world’s appetite for China’s goods—the world’s second-largest economy accounts for nearly one-fifth of global factory exports — has been lower than expected this year. Meanwhile, weak domestic demand continues to reduce imports. Both are contributing to China’s growth slowdown. (Please click here to view larger charts in the PDF version)

“The mix of the data is again not encouraging,” said Commerzbank economist Zhou Hou. “Trade momentum is unlikely to turn around in the near term.”

Sunday’s results suggest the export scene is worsening. China’s General Administration of Customs said October exports fell 6.9% year-over-year in dollar terms, after a drop of 3.7% in September. The October figure was worse than the

median 4.1% decline forecast by 11 economists in a survey by The Wall Street Journal.

Imports in October fell by a sharper-than-expected 18.8% from a year earlier, following a 20.4% decline in September. China’s trade surplus widened in October to $61.64 billion from $60.3 billion in September.

China’s Commerce Ministry said Thursday in a report that exports are likely to see little increase in 2015, while imports will likely report a “relatively big” decline as falling commodity prices continue to weigh on trade flows.

Well, last Friday’s strong US jobs number (and this China export/import news) has put a big dent in our thought oil prices would rally again—targeting to $55. We did manage to sneak out of our long CAD (short USD/CAD) position with a small gain; which was partially predicated on its correlation with oil price, i.e. stronger oil and stronger Canadian dollar.

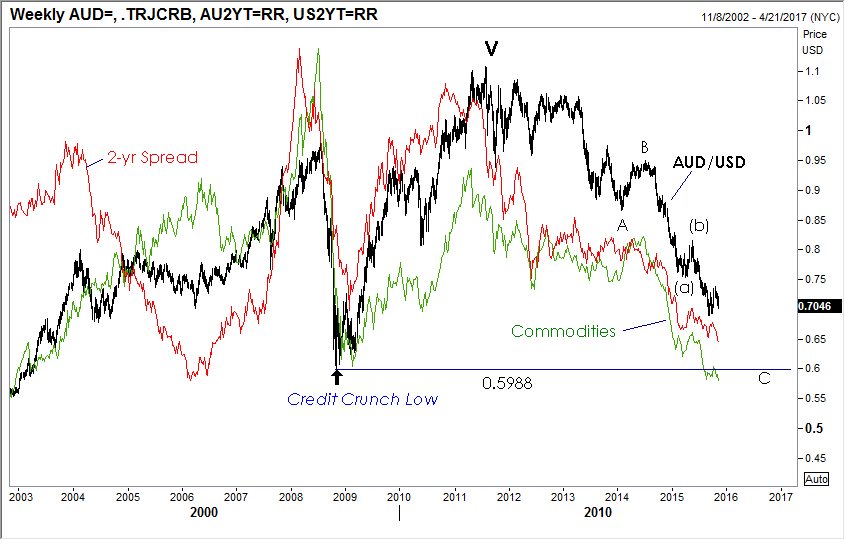

On Friday we went short AUD/USD. Maybe selling into the jobs data didn’t make sense and maybe the moves will be retraced on the open in Asia. But today’s Chinese export data may help the Aussie short trade. Despite commodities being hammered viciously for reasons known, I think some people, including me, expected the latest Chinese stimulus would provide a reprieve. It doesn’t seem it has.

Here is a look at the AUD/USD weekly chart, with commodities prices and the 2-year yield spread Australia-United States overlaid…note both the commodities index and yield spread have pierced below their credit crunch lows—but AUD/USD has not (that comes in at 0.5988; 10+ cents below Friday’s close):

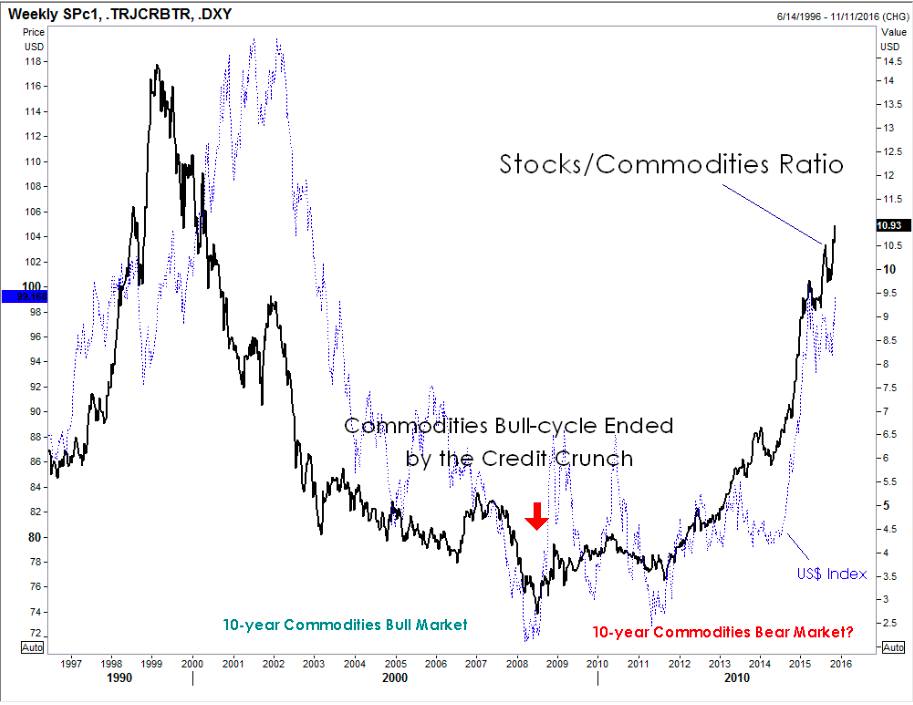

Though the real stuff hasn’t been helped by central bank largess (or maybe it would be much worse without it), the financial stuff has—evidenced being bond and stock prices.

Will there be another knee-jerk assumption the latest weak Chinese data means “more stimulus” or will we finally witness what so many have argued about, with good reason, for so long—a closing of the gaping gap between the real and financial economy (aka stocks coming down)? But will commodities come down even faster if stocks fade? Begs the question of where to hide if so…and begs for an answer that would further impact currencies: US Treasuries would be a place to hide and if that proves true, the dollar gets yet another risk bid.

Ratio: Stocks (S&P 500) divided by Commodities (Thomson Reuters CRB) versus US Dollar Index: Stocks are crushing commodities ever since the credit crunch, boosting the Stocks/Commodities Ratio. And the not so long ago hated greenback is moving right along with it.

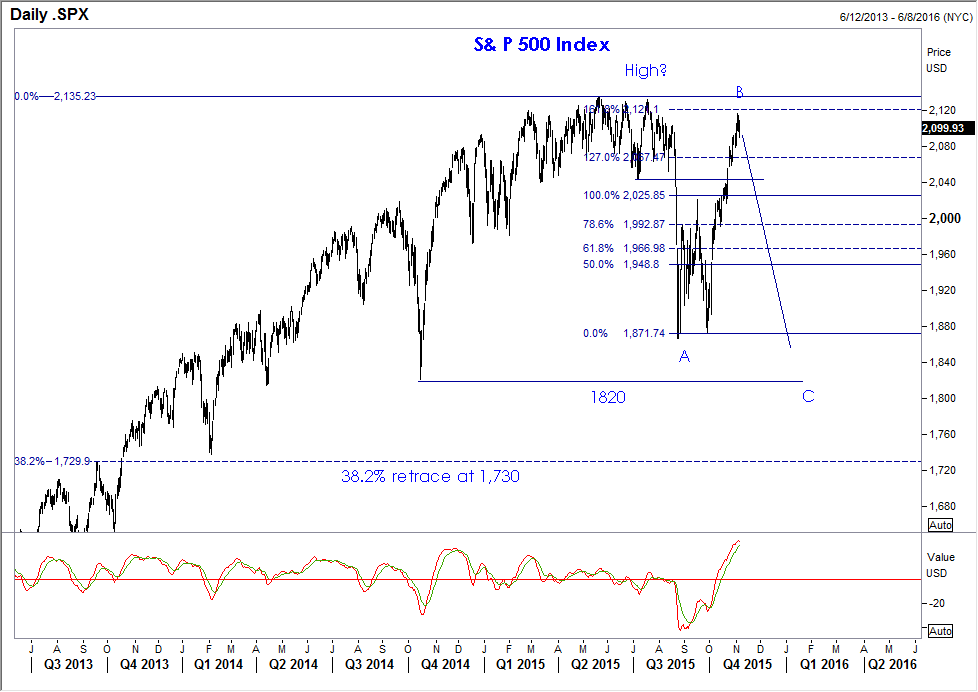

As indicated in my chart posted on Friday—what a great time for Mr. Market to do his thing…

Once again, if I could predict stock prices I wouldn’t be trading currencies. But I do believe as George Soros (the great macro investor version of GS; not the political hack version) said back in 1987—“…stocks are the largest single repository of collateral value for the real economy.” Thus, a break in stocks can be a powerful negative feedback loop to the real economy depending on where we are in the cycle; thus, it’s more potential deflationary raw material in the pound materials. That can’t be good for commodity currencies.

Regards,

Jack Crooks

President, Black Swan Capital

Twitter: @bswanca

Subscription Offer to Black Swan Forex Service [Expires on Today]

If you are interesting in becoming a subscriber to our Black Swan Forex service (which also includes our Current Options Strategist in the price) we are offering a special price.

Special One-term One Year Discounted Price: Only $695—that is over 30% off the normal yearly price of $995 (that includes a one-year subscription to Currency Options Strategist).