Tuesday 4 February 2014

Quotable

“Everything that seems to us imperishable tends towards decay; a position in society, like anything else, is not created once and for all, but, just as much as the power of an empire, is continually rebuilding itself by a sort of perpetual process of creation, which explains the apparent anomalies in social or political history in the course of half a century. The creation of the world did not occur at the beginning of time, it occurs every day.”

Marcel Proust

Commentary & Analysis

I floated the idea in Currency Currents a year or so ago, suggesting maybe the euro was becoming the new yen given its economic backdrop relative to the price action. I.E. no matter the seeming malaise across Europe, its currency continued to remain supported, relatively. The yen of did something similar if you look back: it rallied for years even though Japan’s debt kept rising and its GDP kept falling and its interest rates went to zero (threw a monkey wrench into the whole yield spread argument). Two questions here: Will Europe become mired in the same deflationary trap as Japan’s economy once was? And if so, will its currency react the same way—rally?

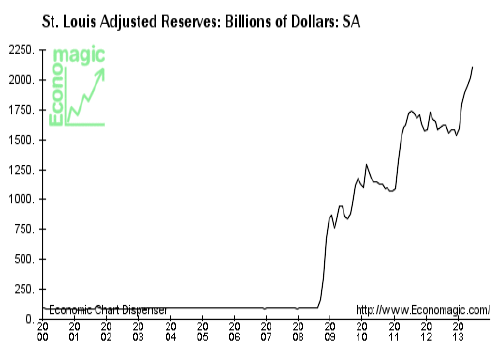

I am not picking on Europe here, so let’s be clear. Everyone knows US policymakers are doing all they can to follow down the same debt and monetary death trap Japan has already blazed. Remember about three or four years ago when Ben “Blitzkrieg” Bernanke assured us the Fed had plenty of tools available to generate inflation? The implicit meaning was the central bank will do all it can to help the Federal government turn its bonds into certificates of confiscation. Well Ben, you’ve done your part by pumping up reserves in the banking system by 2516% since the credit crunch…

…and what do you have to show for it: Falling inflation rates across the G6…not the same as deflation but proves Ben’s toolbox isn’t all that.

Black Swan Capital’s Currency Currents is strictly an informational publication and does not provide personalized or individualized investment or trading advice. Commodity futures and forex trading involves substantial risk of loss and may not be suitable for you. The money you allocate to futures or forex trading should be money that you can afford to lose. Please carefully read Black Swan’s full disclaimer, which is available at http://www.blackswantrading.com/disclaimer