Last month, Money Morning showed you how to use a technique called selling “cash-secured puts” to generate a steady flow of cash from a stock – even if you no longer own the shares.

It is a highly effective income strategy that can also be used to buy stocks at bargain prices.

But selling cash-secured puts does have a couple of drawbacks:

•First, it’s fairly expensive since you have to post a large cash margin deposit to ensure that you’ll be able to follow through on the transaction if the shares are “exercised.” Thus the name, “cash-secured” puts.

•Second, if the market – or the specific stock on which you sell the puts – falls sharply in price, you could have to buy the shares at a price well above their current value, taking a substantial paper loss.

Fortunately, there is a way to offset both these disadvantages while continuing to generate a steady income stream.

It’s called a “credit put spread” and it strictly limits both the initial cost and the potential risk of a major price decline.

I’ll show exactly how it works in just a second, but first I have to set the stage…

The Advantage of Credit Put Spreads

Assume you had owned 300 shares of diesel-engine manufacturer Cummins Inc. (NYSE: CMI) and had been selling covered calls against the stock to supplement the $1.60 annual dividend and boost the yield of 1.30%.

Let’s also assume that back in mid-January, when the stock was around $110 a share, you sold three February $120 calls because it seemed like a safe bet at the time.

However, when CMI’s price later moved sharply higher, hitting $122.07/share, your shares were called away when the options matured on Feb. 17.

That means you had to sell them at $120 per share to fulfill your call option. That might leave you with the following dilemma.

Thanks to the recent rally, the stocks you follow are too high to buy with the proceeds from your CMI sale. On the other hand, you also hate to forfeit the income you had been getting from the CMI dividend and selling covered calls.

You also decide you wouldn’t mind owning CMI again if the price pulled back below $120.

In this case, your first inclination might be to use the money from the CMI sale as a margin deposit for the cash-secured sale of three April $120 CMI puts, recently priced at about $4.90, or $490 for a full 100-share option contract.

That would have brought in a total of $1,470 (less a small commission), which would be yours to keep if Cummins remains above $120 a share when the puts expire on April 21.

That sounds pretty appealing, but…

The minimum margin requirement for the sale of those three puts – and, be aware, most brokerage firms require more than the minimum – would be a fairly hefty $8,190.

[Note: For an explanation of how margin requirements on options are calculated, you can refer to the Chicago Board Option Exchange (CBOE) Margin Calculator, which shows how the minimum margin is determined for a variety of popular strategies.]

Your potential return on the sale of the three puts would thus be 17.94% on the required margin deposit ($1,470/$8,190 = 17.94%), or 4.08% on the full $36,000 purchase price of the 300 CMI shares you might have to buy.

Either of those returns is attractive given that the trade lasts under two months – but you also have to consider the downside.

Should the market plunge into a spring correction, taking Cummins stock with it, the loss on simply selling the April $120 puts could be substantial.

For example, if CMI fell back to $100 a share, where it was as recently as early January, the puts would be exercised.

You’d have to buy the stock back at a price of $120 a share, giving you an immediate paper loss of $6,000 – or, after deducting the $1,470 you received for selling the puts, $4,530.

And, if CMI fell all the way back to its 52-week low near $80, the net loss would be $10,530. (See the final column in the accompanying table.)

All of a sudden, that’s not such an attractive prospect.

And that’s where a credit put spread picks up its advantage.

But selling cash-secured puts does have a couple of drawbacks:

•First, it’s fairly expensive since you have to post a large cash margin deposit to ensure that you’ll be able to follow through on the transaction if the shares are “exercised.” Thus the name, “cash-secured” puts.

•Second, if the market – or the specific stock on which you sell the puts – falls sharply in price, you could have to buy the shares at a price well above their current value, taking a substantial paper loss.

Fortunately, there is a way to offset both these disadvantages while continuing to generate a steady income stream.

It’s called a “credit put spread” and it strictly limits both the initial cost and the potential risk of a major price decline.

I’ll show exactly how it works in just a second, but first I have to set the stage…

The Advantage of Credit Put Spreads

Assume you had owned 300 shares of diesel-engine manufacturer Cummins Inc. (NYSE: CMI) and had been selling covered calls against the stock to supplement the $1.60 annual dividend and boost the yield of 1.30%.

Let’s also assume that back in mid-January, when the stock was around $110 a share, you sold three February $120 calls because it seemed like a safe bet at the time.

However, when CMI’s price later moved sharply higher, hitting $122.07/share, your shares were called away when the options matured on Feb. 17.

That means you had to sell them at $120 per share to fulfill your call option. That might leave you with the following dilemma.

Thanks to the recent rally, the stocks you follow are too high to buy with the proceeds from your CMI sale. On the other hand, you also hate to forfeit the income you had been getting from the CMI dividend and selling covered calls.

You also decide you wouldn’t mind owning CMI again if the price pulled back below $120.

In this case, your first inclination might be to use the money from the CMI sale as a margin deposit for the cash-secured sale of three April $120 CMI puts, recently priced at about $4.90, or $490 for a full 100-share option contract.

That would have brought in a total of $1,470 (less a small commission), which would be yours to keep if Cummins remains above $120 a share when the puts expire on April 21.

That sounds pretty appealing, but…

The minimum margin requirement for the sale of those three puts – and, be aware, most brokerage firms require more than the minimum – would be a fairly hefty $8,190.

[Note: For an explanation of how margin requirements on options are calculated, you can refer to the Chicago Board Option Exchange (CBOE) Margin Calculator, which shows how the minimum margin is determined for a variety of popular strategies.]

Your potential return on the sale of the three puts would thus be 17.94% on the required margin deposit ($1,470/$8,190 = 17.94%), or 4.08% on the full $36,000 purchase price of the 300 CMI shares you might have to buy.

Either of those returns is attractive given that the trade lasts under two months – but you also have to consider the downside.

Should the market plunge into a spring correction, taking Cummins stock with it, the loss on simply selling the April $120 puts could be substantial.

For example, if CMI fell back to $100 a share, where it was as recently as early January, the puts would be exercised.

You’d have to buy the stock back at a price of $120 a share, giving you an immediate paper loss of $6,000 – or, after deducting the $1,470 you received for selling the puts, $4,530.

And, if CMI fell all the way back to its 52-week low near $80, the net loss would be $10,530. (See the final column in the accompanying table.)

All of a sudden, that’s not such an attractive prospect.

And that’s where a credit put spread picks up its advantage.

Here’s how it works…

How to Create a Credit Put Spread

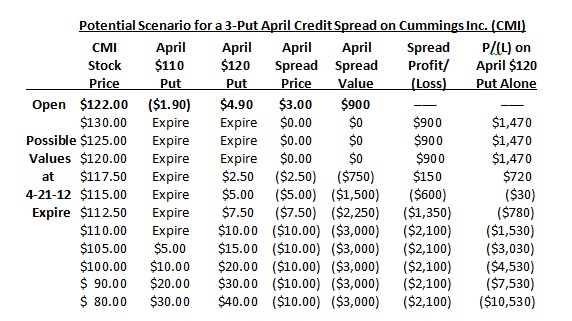

Instead of just selling three April CMI $120 puts at $4.90 ($1,470 total), you also BUY three April CMI $110 puts, priced late last week at about $1.90, or $570 total.

Because you have both long and short option positions on the same stock, the trade is referred to as a “spread,” and because you take in more money than you pay out, it’s called a “credit” spread.

And, in this case, the “credit” you receive on establishing the position is $900 ($1,470 – $570 = $900).

Again, that $900 is yours to keep so long as CMI stays above $120 by the option expiration date in April.

However, because the April $110 puts you bought “cover” the April $120 puts you sold, your net margin requirement is just $2,100 – which is also the maximum amount you can lose on this trade, regardless of how far CMI’s share price might fall. (Again, see the accompanying table for verification.)

That’s because, as soon as the short $120 puts are exercised, forcing you to buy 300 shares of CMI for $36,000, you can simultaneously exercise your long $110 puts, forcing someone else to buy the 300 shares for $33,000.

Thus, your loss on the stock would be $3,000, which is reduced by the $900 credit you received on the spread, making your maximum possible loss on the trade $2,100.

On the positive side, if things work out – i.e. CMI stays above $120 in April – and you get to keep the full $900, the return on the lower $2,100 margin deposit is a whopping 42.85% in less than two months, or roughly 278.5% annualized.

Plus, as is the case with most option income strategies, you can continue doing new credit spreads every two or three months, generating a steady cash flow until you’re ready to repurchase the stock at a more desirable price.

In this case, we say “ready” to repurchase because you’re never forced to buy the stock; you can always repurchase the options you sold short prior to expiration.

This strategy has substantial cost-cutting benefits when trading higher-priced issues like CMI, but it’s also a very effective short-term income strategy with lower-priced shares.

For example, with Wells Fargo & Co. (NYSE: WFC) trading near $31.50 late last week, an April credit spread using the $31 and $28 puts would bring in a net credit of 75 cents a share, or $225 on a three-option spread.

Since the net margin deposit on the trade would be just $675, you’d get a potential return of 33.3% in only seven weeks if WFC remains above $31 a share.

As you can see, credit put spreads are a great way to boost your gains while lowering your risks, especially in stable or rising markets.

So why not give yourself some credit.

Source http://moneymorning.com/2012/03/05/options-101-credit-put-spreads-can-boost-your-gains-and-lower-your-risk/

Money Morning/The Money Map Report

©2012 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email:customerservice@moneymorning.com” target=”_blank”>customerservice@moneymorning.com

Here’s how it works…

How to Create a Credit Put Spread

Instead of just selling three April CMI $120 puts at $4.90 ($1,470 total), you also BUY three April CMI $110 puts, priced late last week at about $1.90, or $570 total.

Because you have both long and short option positions on the same stock, the trade is referred to as a “spread,” and because you take in more money than you pay out, it’s called a “credit” spread.

And, in this case, the “credit” you receive on establishing the position is $900 ($1,470 – $570 = $900).

Again, that $900 is yours to keep so long as CMI stays above $120 by the option expiration date in April.

However, because the April $110 puts you bought “cover” the April $120 puts you sold, your net margin requirement is just $2,100 – which is also the maximum amount you can lose on this trade, regardless of how far CMI’s share price might fall. (Again, see the accompanying table for verification.)

That’s because, as soon as the short $120 puts are exercised, forcing you to buy 300 shares of CMI for $36,000, you can simultaneously exercise your long $110 puts, forcing someone else to buy the 300 shares for $33,000.

Thus, your loss on the stock would be $3,000, which is reduced by the $900 credit you received on the spread, making your maximum possible loss on the trade $2,100.

On the positive side, if things work out – i.e. CMI stays above $120 in April – and you get to keep the full $900, the return on the lower $2,100 margin deposit is a whopping 42.85% in less than two months, or roughly 278.5% annualized.

Plus, as is the case with most option income strategies, you can continue doing new credit spreads every two or three months, generating a steady cash flow until you’re ready to repurchase the stock at a more desirable price.

In this case, we say “ready” to repurchase because you’re never forced to buy the stock; you can always repurchase the options you sold short prior to expiration.

This strategy has substantial cost-cutting benefits when trading higher-priced issues like CMI, but it’s also a very effective short-term income strategy with lower-priced shares.

For example, with Wells Fargo & Co. (NYSE: WFC) trading near $31.50 late last week, an April credit spread using the $31 and $28 puts would bring in a net credit of 75 cents a share, or $225 on a three-option spread.

Since the net margin deposit on the trade would be just $675, you’d get a potential return of 33.3% in only seven weeks if WFC remains above $31 a share.

As you can see, credit put spreads are a great way to boost your gains while lowering your risks, especially in stable or rising markets.

So why not give yourself some credit.

Source http://moneymorning.com/2012/03/05/options-101-credit-put-spreads-can-boost-your-gains-and-lower-your-risk/

Money Morning/The Money Map Report

©2012 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email:customerservice@moneymorning.com” target=”_blank”>customerservice@moneymorning.com