Since my sophomore year in college what I’ve loved most is analyzing economics, finance and corporate fundamentals. The 1987 crash occurred when I was still a clueless high school senior, but by the time I started my first internship in 1989 – at Paine Webber, cold calling certificates of deposit yielding 6% – I was reading the Wall Street Journal daily and daydreaming of working at Goldman Sachs. My first decade in the business was highly optimistic, but by the time Goldman actually offered me a job in May 1998, I already disliked them so much, no amount of money could have sealed the deal. Instead, I worked for Salomon Smith Barney – owned by none other than what has turned out to be the nation’s most destructive financial force outside JP Morgan and Citigroup.

In the ensuing 16 years, the business I once loved was utterly destroyed by the “1%” running such firms; with Citigroup’s own Sandy Weill spearheading the 1999 repeal of Glass-Steagall; which, in hindsight, was the single most destructive economic act of our lifetimes. By the time I left Wall Street in 2005, equity research had been long discredited; and by the time I left mining investor relations to join Miles Franklin in 2011, the Wall Street institution was permanently lost to corruption. More ominously, its traditional economic roles of capital formation and allocation were no longer necessary; as following two decades of offshoring “productivity” gains and the emergence of Eastern hemisphere powers like China, America’s economic empire was in irreversible decline. This is when TPTB realized the only way to maintain the status quo – or more appropriately, “kick the can” that last mile – was exponential growth of money printing, market manipulation and propaganda. This is how dying empires collapse; and oh yeah, fiat currency Ponzi schemes in their terminal stage.

Today, 25 years from that Paine Webber internship with CD yields at 0% and in danger of turning negative, I still love financial analysis more than anything. However, now that markets are rigged, my finance degree, CFA degree and 15 years of buy- and sell side experience have been rendered moot. Thus, I’ve been forced to build an “alternative” analytical mosaic; which fortunately, is not immune to the forces of “Economic Mother Nature.” Using it, as well as common sense, I have been consistently correct in my expectations of global economic growth; and via this mosaic, I have never been more negative about the world’s short- and intermediate-term outlooks. As for the long-term, I have not the slightest idea when prosperity will return. However, what I do know is that until today’s global fiat Ponzi scheme inevitably implodes, prosperity is not possible. This is why I hold 90% of my liquid net worth in physical gold and silver; as when the dollar, Euro, yen and other fiat trash are dramatically devalued in the coming years, they are theonly assets guaranteed to maintain purchasing power.

Which brings me to today’s very important topic. Not that we haven’t spoken of it countless times before; but as a new world-threatening “episode” has emerged, with the prospect of violently expanding in the coming months it appears to be a good time to speak of it. Which is the economically catastrophic impact of fiat currency volatility, particularly relative to the dying universally despised “dollar.”

Yesterday, I read an article titled “Germany loses the battle for the ECB, as QE goes global.” Essentially, it was referring to the virulent “final currency war” we have been writing of for years. In other words, in the final cancerous stage of the fiat Ponzi scheme, global economic growth has been so badly crippled, politicians and Central bankers are resorting to dramatic currency devaluations in the hope of gaining all-important manufacturing market share – and thus, “jobs.” The fact that inflation erodes the value of such gains and prompts draconian retaliation by other nations – in the form of “competitive currency devaluations” – bothers them not, so long as said jobs are produced.

Unfortunately, this deadly “zero sum” game is infamous for not only destroying capital, but prompting economic – and often military – wars. This is why global unrest has not been this ubiquitous in generations, and why World War III is just one “black swan” event away. Currency volatility makes it nearly impossible to build a long-term corporate strategy and wreaks havoc with earnings – particularly, at companies whose financial departments are too “cute” with hedging strategies, which by and large fail miserably. This is the legacy of a world gone mad in which not a single currency is backed by anything but the “full faith and credit” of corrupt, uncaring, financially unsophisticated governments which cede unlimited money printing authorization to bankers incentivized to generate inflation for their own interests.

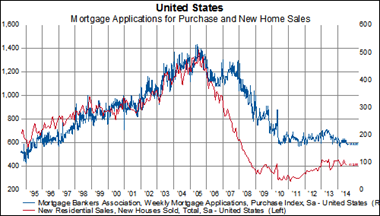

Regarding economic activity, what more damning statement can be made than the below chart, of the supposedly strongest sector of the supposedly strongest nation; let alone,this fantastic article by David Stockman of the true state of U.S. employment decay? Meanwhile, Europe’s widely watched Sentix Investor Confidence Index plunged this morning from 2.7 in August to -9.8 in September, whilst Japanese capital spending was reported to have experienced its largest decline since the “deer in headlights” economic trough of 1Q09. In other words, “it” appears to be starting – which is why you mustconsider protecting your assets as soon as possible!

In our view, the “single most bullish PM factor imaginable” is the catastrophic economic dislocation, political and social tension and inflation caused by the currency volatility inherent in all fiat currency regimes. Such volatility increases as their inevitable end approaches; and the current “emerging market” currency plunge – catalyzed by Draghi doing “whatever it takes,” and the Bank of Japan on the verge of same – is the fourth such episode in the past five years. In last year’s “Inflation and Arab Spring,” we wrote of how such volatility – which always effects lesser “non-reserve” currencies first – creates massive inflation surges, nearly always followed by social unrest. This time around with sovereign balance sheets and economies in dramatically worse shape, we shudder to think how inflationary – and potentially, hyperinflationary – the coming round of massive Central bank money printing will be. And yes, that goes for the “tapering” Federal Reserve as well.

Is this week’s U.S. rate surge (albeit, quite modest in absolute terms) due to better economic prospects (NO!), Fed manipulation or otherwise? Who knows; but as is becoming quite evident, next week’s Scottish independence referendum has emerged as quite the “black swan” candidate. Amidst such a capricious global economic situation, such an event could send shock waves through financial markets – particularly the other “supposedly” strong nation, England. Of course, in reality, England’s economy is in the same sorry shape as ours – with its only “bright spot” being the same high-end real estate bubble as the one the Fed has created here; which, by the way, was deflatingbefore the potentially catastrophic “Yes Scotland” movement gained steam. More importantly, the inevitable secession – and expulsion – movements I first wrote of in 2011’s “unprecedented” are clearly gaining momentum; which is probably why Spanish bond yields had their biggest spike in 15 years this week – and why nations like Italy, states like California and various other municipalities are in danger of monstrous yield spikes in the coming months.

In the past month, the “dollar index” has risen modestly from 81 to just over 84; in other words, solidly within the 70-90 range it has traded within for the past decade. However, the inflationary impact of such a move cannot be underestimated. In the case of Europe, the euro’s recent plunge will likely generate the inflation Draghi so desperately wants, even before ECB QE starts in October. In Japan, which not only broke through long-term support at 105/dollar this week, but 106/dollar as well, it may well be that the “real Yen bomb starts now.” And as for U.S., said dollar “surge” will cause dramatically weaker earnings for the multi-national corporations dominating the economic landscape; which, given unparalleled equity overvaluation and economic data “decoupling” could prove catastrophic to TPTB’s “recovery” illusion,” no matter how hard their “PPT teams” huff and puff.

Such dramatic economic shifts, in turn, will warrant retaliation by the Fed – in the form of further monetary easing, yielding increased money printing by the countless nations “pegged” to the dollar – such as China; and so on and so on. In other words, the latest round of “emerging market” currency collapses – which cumulatively, have shaved nearly 40% of purchasing power versus the dollar in the past three years – has the potential of catalyzing the “big one”; from which, when it commences, there will be no possibility of reversal or escape from regional hyperinflation.

And when the “big one” inevitably occurs, there will no longer be even the slightest doubt of what the true definition of “inflation” is. Or, for that matter, that the “dollar index” is not how one should measure the dollar’s strength – but instead, the real items of value it buys or won’t buy – such as history’s only real money, physical gold and silver. To that end, we hope you will consider protecting yourself before it’s too late; and if you do, that you’ll give Miles Franklin celebrating our 25th year of business the opportunity to earnyour business.

Andrew C. Hoffman, CFA

Marketing Director

Miles Franklin Ltd.