Reflections on “Paper Reserves” of Central Banks; Gold and the Tapering Disconnect

But what about foreign central bank assets, especially China and Japan?

Reflections on “Paper Reserves” of Central Banks

Hugo Salinas Prices covers the topic in an excellent article Some Thoughts on ‘International Reserves’

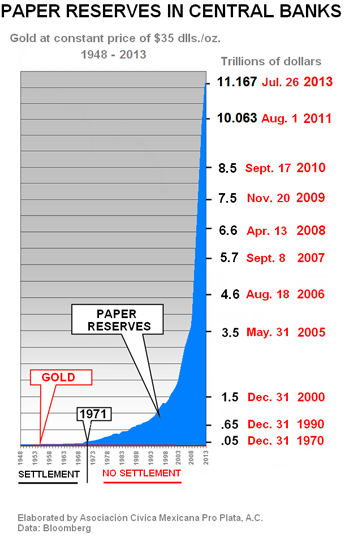

International reserves, excluding gold, as reported by Bloomberg, courtesy of Doug Noland at www.prudentbear.com on July 26, 2013, stood at $11.167 Trillion dollars.

International reserves, excluding gold, are mainly made up of dollar and euro holdings.

On August 1, 2011, holdings amounted to $10.063 Trillion dollars. One year later, holdings had increased to $10.450 Trillion dollars, an increase of $387 billion dollars.

In the most recent twelve months, holdings have increased by $717 billion dollars, to the present level of $11.167 Trillion dollars.

International reserves increase when importing countries cannot pay for their imports with exports; in other words, when the importing countries have “trade imbalances” and make up the trade imbalance by sending (mainly) either dollars or euros to the exporting countries.

The increase in “International Reserves Excluding Gold” from 1971 to the present – 42 years – has been spectacular.

It is important to note that “International Reserves” are invested in diverse Bonds, prima facie evidence that trade imbalances have not been settled since 1971. Settlement happens when a debt is paid. If a country owns Bonds, it is a holder of debt and has not been paid. Had the trade imbalances been settled, International Reserves would be not much different from what they were in 1971.

“International Reserves” thus represent credit which the exporting countries of the world have granted to the importing countries which use dollars and euros as money; when these countries tender dollars or euros in “payment”, they are not settling any debt; they are simply running up more debts with the exporting countries. $11.167 Trillion dollars and counting. The Reserves earn interest – they are invested in Bonds – and so the Reserves must also grow, as interest earned accumulates.

When and how will this increase in the debt of the importing countries to the exporting countries find a limit?

10 days, 10 weeks, 10 months, 10 years – nobody knows. But this game is going to end, someday, and its ending will be painful. When the dust settles, a whole new world will replace the present one. We have no idea what it will look like, but it will be here, populated by humanity who will not cease to wonder: “What were they thinking?”

Gold and the Tapering Disconnect

It should be crystal clear this “game” cannot possibly continue forever. Yet, the doves on the Fed, notably Janet Yellen (who amazingly is even more dovish than Bernanke), act and talk as if it can.

Is any “tapering” is going to occur? Certainly the Fed is not going to hike rates, even if some small amount of tapering does occur.

This setup should be good for gold, but it sure hasn’t.

Curiously, the stock market acts as if no tapering is coming, but gold acts as if the Fed is actually about to tighten, not just taper.

As with perpetually rising trade deficits, this disconnect will not go on forever, but I cannot say when it ends, and nor can anyone else.

For more on the balance of trade problem and how to permanently fix it, please see Hugo Salinas Price and Michael Pettis on the Trade Imbalance Dilemma; Gold’s Honest Discipline Revisited.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

Read more at http://globaleconomicanalysis.blogspot.com/2013/08/reflections-on-paper-reserves-of.html#akDpoy3qUXx0Ammm.99