Investors may be taken for a ride by today’s Minutes of the Federal Open Market Committee (FOMC), which expand on the FOMC’s March 13, 2012 statement; in the interim, we believe the Federal Reserve (Fed) Chairman Bernanke has gone out of his way to assure the markets that monetary policy will remain “highly accommodative,” at least through late 2014.

The Fed does indeed have a credibility problem: having assured investors that rates will remain low for an extended period, it may only take one or two FOMC members to turn more optimistic about the economic outlook to cause the markets to more aggressively price-in tighter monetary policy. Conversely, Bernanke has made it clear that he is most concerned about a recovery in the housing market and that low interest rates – throughout the yield curve – are desirable. Operation Twist is specifically aimed to achieve that, lowering long-term rates and flattening the yield curve. However, should investors become increasingly optimistic about economic improvement, odds increase that investors sell bonds, putting upward pressure on long-term rates.

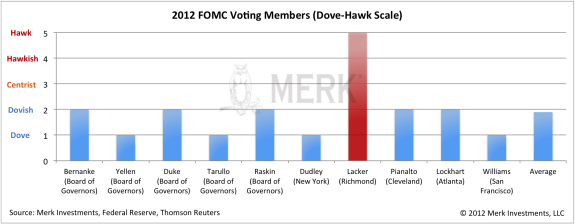

To understand the Fed’s “communication strategy”, one needs to be aware of who is calling the shots. We are not just talking about Fed Chairman Bernanke, but also the composition of voting FOMC members. Without a doubt, the “hawks” (hawks are FOMC members considered to favor tighter monetary policy compared to “doves”) on the FOMC are getting more vocal. At the same time, the only voting “hawk” on the FOMC this year is Richmond Fed President Jeff Lacker:

The scale may tilt a tad towards the centrist/hawkish side should Congress fill the two vacant seats with the candidates under consideration. Still, when all is said and done, it is the voting members who ultimately determine imminent monetary policy decisions, rather than the noise created by non-voting members. And those actions remain, in our interpretation, decisively on the dovish side:

- “almost all members again agreed to…maintain a highly accommodative stance…”

- “a number of members perceived a non-negligible risk that improvements in employment could diminish as the year progressed”

Obviously, should economic data continue to surprise to the upside, the Fed will have an ever-more difficult time defending its dovish position. The credibility of the Fed will be seriously tested as the Fed has committed to keeping rates low until late 2014. However, should we enter a weak patch, we believe the odds are rather high that the FOMC will “take out insurance” against another slowdown. In a world where everyone hopes for the best, but plans for the worst, central banks around the world – including the Fed – may keep the world awash in money.

After all, a world laden with debt may need inflation if deflation is to be avoided. Bernanke has argued many times that tightening monetary policy too early was one of the biggest mistakes the Fed made during the Great Depression. We don’t think Bernanke will repeat this. Indeed, we consider he will err firmly on the side of inflation. As such, when the dust settles, look at actions, not words. We see doves, not hawks, managing the monetary aviary.

Please register for our Webinar on Thursday, April 19, or sign up for our newsletterto be informed as we discuss global dynamics and their impact on currencies.

Axel Merk

President and Chief Investment Officer, Merk Investments

Merk Investments, Manager of the Merk Funds