Bubble, Bubble, Toil and Trouble?

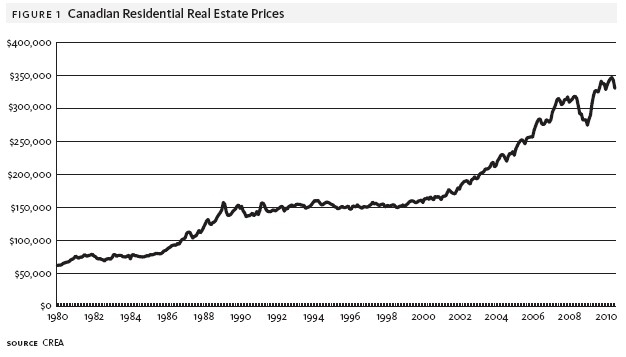

A correction in the Canadian housing market is looking ever more likely. In 2001, both Canada and the US lowered interest rates ( cheap money) which helped fuel a housing boom. In 2008 the US experienced a marked reversal in housing prices, bringing them in line to their long term growth rates. In Canada this did not happen.

We don’t feel that Canada magically avoided this correction – it just hasn’t happened yet. There are several factors that could contribute to a significant correction in Canada’s housing market.

- Our personal savings rate is decreasing (currently only 2.9%)

- Our consumer debt level is increasing (currently $25,597/person)

- Growth in housing prices continues to vastly outpace growth in rents

- Interest rates are at record lows and are poised to rise

- New mortgage rules have been instituted to slow growth

Historically, housings prices have been a function of the rents they can achieve. If it gets too expensive to buy, people will rent. This will drive housing prices down and bid up prices for rents, creating an equilibrium. In 2001, this relationship started to break down and housing prices rose significantly more than rents. Was this simply a matter of people willing to pay a premium for home ownership? Possibly, but a more likely explanation is that there was a bubble fueled by cheap credit. People justified making offers over asking prices because there was an expectation that housing prices would be higher the next year. More money was available to bid up prices and bidding wars ensued.

In the US housing prices have since moved to a level where we would expect them based on the long term house price to rent ratio. In Canada, this ratio has not experienced a correction and housing prices continue to be significantly higher than rents. This difference is muted with lower interest rates (which lowers carrying costs), but as interest rates rise, it will become more apparent as mortgages come up for renewal.

If you any questions about this report, or to discuss how Euro Pacific can help manage your portfolio, please contact me.

Kind regards,

Dan Simon

Investment Consultant

w. 416.479.8996 | f. 647.776.3284

c. 416.602.7960

tf. 888.216.9779 x403

dan.simon@europac.ca“>dan.simon@europac.ca

Euro Pacific Canada Inc.

130 King Street West | Exchange Tower

Suite 2820 | Box 20

Toronto, ON, M5X 1A9

www.europac.ca