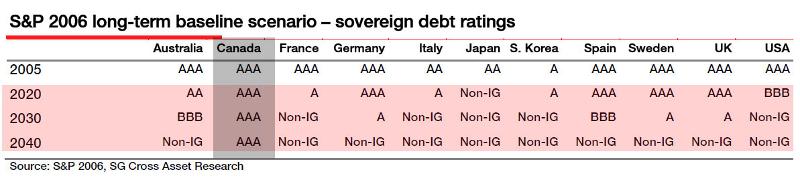

According to research by SocGen, by 2040 Canada will be the only G7 country with investment grade sovereign debt. By as early as 2030 the US, France, Italy and Japan will all lose investment grade status. To put this into perspective this means that in less than 2 decades the debt of countries currently representing approximately 50% of global GDP will be ineligible for investment by the smallest municipal pension fund.

Japan is actually expected to lose investment grade status in less than 10 years and looking at the charts below this should not come as a surprise when it happens. BTW – Japan by itself represents almost 10% of global GDP.

Clearly some profound changes are coming to the sovereign debt markets and most importantly to the idea of the “risk free” rates of return that can be found there. As one wag recently described it, sovereign debt no longer represents “risk free return” but rather “return free risk”.

US Budget Deficits – Sustainable?

Perhaps a picture truly is worth a thousand words. In this case think of the word “unsustainable” over and over again.

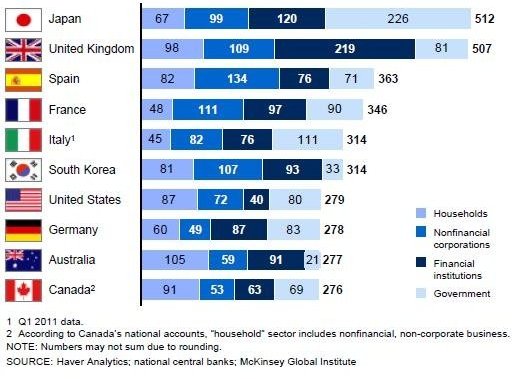

If Greece is Bad What are the UK and Japan?

The chart below is the total debt as percent of GDP for the 10 largest mature economies. Greece isn’t even worth an honourable mention when placed alongside the truly gargantuan debts of Japan and the UK – on a per capita or absolute basis.

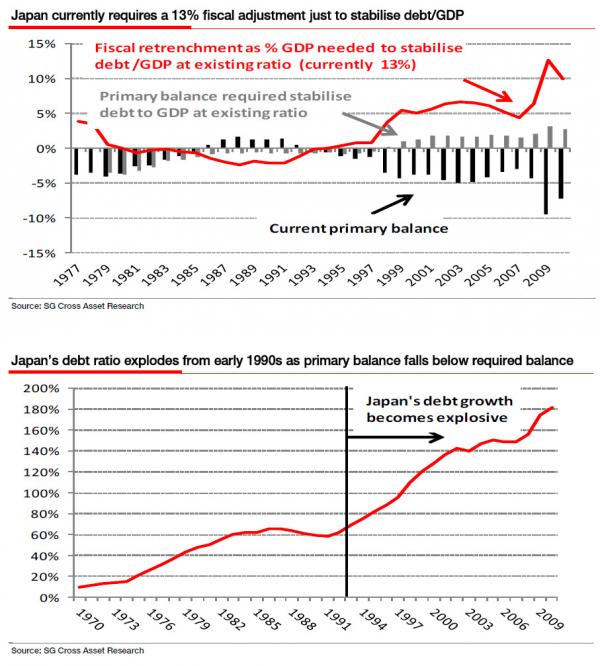

Is Even More Bad News Possible for Japan?

Sadly the answer appears to be yes. Deteriorating demographics with the attendant upward pressure on government spending and a move to sustained current account deficits – all in a low growth environment – have combined to create the perfect storm for Japan’s fiscal position – its bad and getting worse rapidly.

Agcapita Farmland Fund III

Farmland increasingly is in the news as more investors come to appreciate the superior qualities of the asset class – including low return volatility, diversification benefits due to a limited correlation to public equities and good risk adjusted returns. Agcapita Fund III is currently open and RRSP eligible.

- Residents in BC, Alberta, Saskatchewan or Manitoba – CLICK HERE to be contacted with more info.

- Resident in Ontario and an Accredited Investor – CLICK HERE to be contacted with more info.

The Ontario Securities Commission has a detailed definition of Accredited Investor which can be found HERE. However in general Accredited Investor means:

- An individual who, alone or together with a spouse, owns financial assets worth more than $1 million before taxes but net of related liabilities or

- An individual, who alone or together with a spouse, has net assets of at least $5,000,000.

- An individual whose net income before taxes exceeded $200,000 in both of the last two years and who expects to maintain at least the same level of income this year; or

- An individual whose net income before taxes, combined with that of a spouse, exceeded $300,000 in both of the last two years and who expects to maintain at least the same level of income this year.

- An individual who currently is, or once was, a registered adviser or dealer, other than a limited market dealer

Some Quotable Quotes

Simply for entertainment value if nothing else, here is former Federal Reserve Chairman Alan Greenspan describing the robust nature of the US housing market and the safety of mortgage backed securities – all shortly before the largest financial crisis in history driven by a collapse in US housing prices:

“I believe that the general growth in large [financial] institutions have occurred in the context of an underlying structure of markets in which many of the larger risks are dramatically — I should say, fully — hedged.”

“Even though some down payments are borrowed, it would take a large, and historically most unusual, fall in home prices to wipe out a significant part of home equity. Many of those who purchased their residence more than a year ago have equity buffers in their homes adequate to withstand any price decline other than a very deep one.”

“The use of a growing array of derivatives and the related application of more-sophisticated approaches to measuring and managing risk are key factors underpinning the greater resilience of our largest financial institutions …. Derivatives have permitted the unbundling of financial risks.”

“Improvements in lending practices driven by information technology have enabled lenders to reach out to households with previously unrecognized borrowing capacities.”

“Indeed, recent research within the Federal Reserve suggests that many homeowners might have saved tens of thousands of dollars had they held adjustable-rate mortgages rather than fixed-rate mortgages during the past decade, though this would not have been the case, of course, had interest rates trended sharply upward.”

Regards

Agcapita