Uncategorized

Mike and the team are taking some well-deserved time off, so there won’t be a Christmas day show. But tune in next Wednesday, December 29th for a special year in review show. Highlights from 2021, and of course, a look ahead to 2022.

In the meantime we know Mike won’t be able to resist posting to Facebook and Twitter so enjoy those feeds too.

Merry Christmas and Happy Holidays!

Get the inside scoop on preferred shares and the tax benefits of dividend income with Nick Otton of Capitalight Research. Plus Mike talks to Terry Glavin about Canada’s feeble response to China, a horrific and troubling quote of the week, the shocking stat and much, much more. Right here starting at 8:30am pacific on Saturday, Dec 11th.

Kevin Muir, the MacroTourist himself, joins Michael to share where he’s looking for undervalued Canadian companies plus some of the markets he’s trading in the short term. The Fed “retires” the word transitory as it applies to inflation, Victor Adair on the “whipsaw” market action he’s seeing at the Trading Desk, a Shocking Stat of epic proportions, and much more.

All right here starting at 8:30am pacific on Saturday, December 4th.

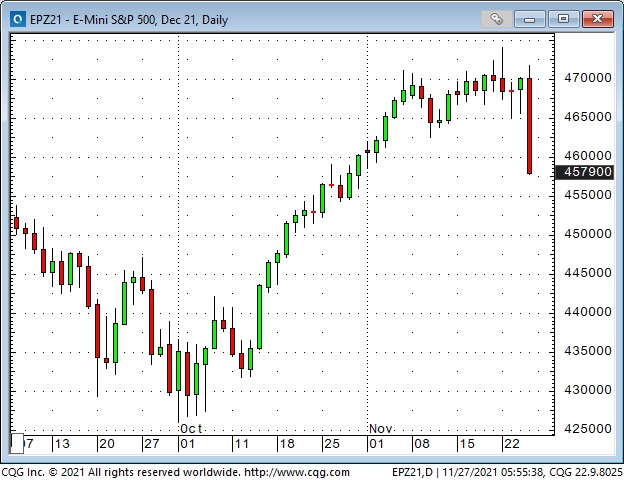

Risk Happens Fast

The S+P 500 hit All-Time Highs on Monday’s opening – but closed 165 points (3.5%) lower by Friday’s close. The daily S+P futures volume on Friday was the highest since early October – and was probably the highest EVER for a Thanksgiving Friday.

The DJIA closed at a 7-week low, down ~1,800 points (5%) from the All-Time High reached three weeks ago.

The Acid Test

My recent thinking has been that market complacency would likely continue – unless the September/October lows are taken out. I think people who have put money into “passive” investment strategies have been told to expect minor corrections and short-term spikes in volatility – but to stay the course because, inevitably, stocks will keep rising.

I think those folks also “feel” as though the unrealized gains in their investment accounts are as “good as cash” when it comes to calculating their net worth, and that, while the market could have a dip now and then, it will NEVER AGAIN drop like it did in March 2020.

When Complacency Turns To Panic, Volatility Soars

There was complacency with “risk-on” sentiment across asset classes early this week, but as sentiment turned “risk-off” Thursday afternoon and prices began to slide, “liquidity risk” accelerated the panic, and volatility soared.

Position Unwinding Added To Volatility

For the past few weeks, traders (especially in the interest rate and currency markets) have been building positions around the idea that the Fed would be “forced” to raise interest rates much more, and much faster, than previously expected – because of “inflation.” There was severe unwinding of some of those positions in illiquid market conditions during the last 24 hours of the trading week.

Interest rates: As stock indices tumbled on Thursday/Friday, bonds rallied hard, and short-term interest rate futures “un-priced” at least one Fed rate increase next year.

Currencies: The US Dollar Index surged to a new 16-month high early this week on expectations that the Fed would be much more hawkish next year than previously expected. The USD reversed those gains on Friday to close unchanged for the week.

The Japanese Yen plunged to a new 5-year low against the US Dollar early this week but reversed HUGE on Friday. Speculators have amassed a HUGE net short Yen position over the past few months.

The Swiss Franc caught a “haven” bid Friday after tumbling the past two weeks on expectations of Fed tightening next year.

The Canadian Dollar hit a 6-year high against the USD at 83 cents in June but fell back as the USD began to rally against all currencies.

The CAD rallied to a lower high (81 cents) in October as commodity indices (especially crude oil) surged to 7-year highs. When the commodity indices (especially crude oil) began to roll over and slide lower, the CAD also began to trend lower.

WTI rallied from ~$62 to ~$85 (37%) in two months, from mid-August to mid-October. The strong demand for near-term delivery over deferred delivery caused a severe steepening of the forward curve. Front-month WTI fell from ~$85 three weeks ago to a low of ~$68 Friday, with more than half that decline happening in illiquid conditions on Friday. Implied volatility in WTI options spiked sharply.

Gold rallied ~$110 the first two weeks of November and fell ~$100 the next two weeks. Gold’s initial rally phase happened in sync with a USD rally (an unusual occurrence) as both markets reacted to the “soaring inflation” narrative. Gold’s tumble happened as the USD continued to rally (the more typical gold/dollar relationship), and as real interest rates reversed from record negative levels.

Open interest in the gold futures market (circled above) increased sharply as gold rallied in early November as speculators “chased” it higher. As gold fell, some of those speculators “bailed out,” exacerbating the decline.

My Short Term Trading

The only position I held as this week began was short gold, and I covered that for a good profit on Monday. Gold had tumbled ~$75 in three days – I was only short because I was looking for some “give-back” after the early November rally – so I covered the position.

I shorted the NAZ about an hour after the Monday floor session opened. The market had surged to an All-Time High on the opening but then dropped below the opening range. I had been looking to sell “irrational exuberance,” so I saw a nice setup and got short with tight stops. The market fell during the day, and I lowered my stops – and was stopped for a small gain later in the day.

The falling bond market on Monday increased my confidence to short NAZ as that index is heavily weighted with “long duration” stocks.

I shorted NAZ again on Tuesday but I was also watching the Dow futures and noticed they were not falling. I covered the short NAZ for a small gain and bought Dow futures. I was stopped for a small loss.

I bought the S+P on Wednesday, was stopped for a small loss, but then I bought it again. The market closed right on its highs so I decided to stay with the trade into the Thanksgiving holiday. (This was a decision to give the trade an opportunity to run. The market had been trending strongly higher, had dipped Monday and Tuesday, and was now closing right on the highs. Staying with the trade was the right thing to do.)

The market continued to rally in the Wednesday overnight session. I raised my stops. The market drifted sideways during the Thursday holiday session, but then began to tumble as soon as the Thursday overnight session began and I was stopped for a small gain.

I made the right decision to stay with the trade when it closed on its highs. At its best levels, I was ahead nearly 40 points but was stopped for a gain of only four points. I have no regrets about that. Given what happened next, I’m thankful that I use stops.

I bought the CAD and gold on Wednesday. I was stopped for a small loss on the CAD in the Thursday overnight session and covered the gold for a small gain Friday morning.

I did not establish any new positions Friday and was flat going into this weekend. My P+L was up just short of 1% on the week.

On My Radar

I don’t know if Friday’s market action was the start of something BIG or a one-day flash-in-the-pan. I’m willing to go either way, although I’m leaning towards the start of something.

My bias has been that too much money has been flooding into risk assets without appreciating just how risky those assets can be. The risk in those assets has increased “because” of the money flooding in.

Thoughts On Trading

For years I had a small yellow sticky note on my screens saying, “Anything Can Happen.” I put it there to remind myself that I had no idea what was going to happen next.

A few weeks back, in the Quotes From The Notebook section, I featured the Godfather saying, “I spent my entire life trying not to be careless.”

If I wanted to briefly explain the essence of my trading style, I would say that I never want to take a big loss. I never “fall in love” with a trade.

Several years ago, I started working with another broker that I didn’t know very well. We were opening a new office for a Chicago commodity firm in Vancouver. One day I overheard him talking to his best client. He was telling his client why they had to stay with a trade that was relentlessly going against them. I couldn’t believe what I was hearing.

A few days later, I had an epiphany while taking a shower before I headed to work (I get a lot of good ideas in the shower or in the pool – there’s something about water that does that – and, of course, you can’t make a note to yourself when you’re in the water!) My epiphany was that the broker was, first and foremost, a stockbroker – who also happened to be a commodity broker – and that stockbrokers believe and tell stories – good commodity brokers don’t do that.

Here’s a 90-second video of Jack Schwager (author of the Market Wizards series) explaining that one of the things the 70 Wizards he interviewed for his books had in common was their ability to have no loyalty to a position. (This is a fantastic insight – and great trading advice!)

Quotes From The Notebook

“Don’t count your chickens before they hatch.” My Grandmother kept telling me that from the time I was a little boy until she died.

My comment: My friend Peter Brandt likes to say that he never counts unrealized gains as “his money” it’s not his until he closes the trade. I can’t tell you how many times I’ve assumed that a trade would be a big winner – only to have it go sour on me.

Peter also likes to ask this question, “Let’s say you hold a position with an unrealized gain of $10,000. The market moves against you and you liquidate the trade to realize a $5,000 gain. Do you feel like you made $5,000 or lost $5,000 ?”

My guess is that if you feel like you lost $5,000 (because you didn’t get out at the top) you’re going to have an unhappy life as a trader. Have I mentioned before that trading is not a game of perfect?

“WHEN you make a trade is WAY more important than WHY you make a trade.” Raoul Pal, Founder of Real Vision TV, 2021

My comment: I agree 100%. Focusing on “why” you are making a trade may cause you to be too “loyal” to the trade. (Refer to Jack Schwager’s interview above.) Focusing on “when” you make a trade means you realize that there is a time to make the trade, and a time to NOT make the trade.

A Small Request

If you like reading the Trading Desk Notes, please do me a favour and forward a copy or a link to a friend. Also, I genuinely welcome your comments. Please let me know if there is something you would like to see included in the TD Notes. Thanks, Victor

Barney (now 12 weeks old) “Papa, leave your computers alone and play with me!”

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.

Each week Josef Schachter gives you his insights into global events, price forecasts and the fundamentals of the energy sector. Josef offers a twice monthly Black Gold newsletter covering the general energy market and 30 energy, energy service and pipeline & infrastructure companies with regular updates. We also hold quarterly webinars and provide Action BUY and SELL Alerts for paid subscribers. Learn more.

EIA Weekly Data: The EIA data of Wednesday November 17th was mixed. US Commercial Crude Stocks fell 2.1Mb (forecast 135K decline) as Net Imports fell 490Kb/d, reducing inventories by 3.43Mb. If this had not occurred there would have been a 1.1Mb build. The key subcomponent Exports showed a rise of 573Kb/d which indicates exports rose by 4.0Mb last week, lowering US Commercial Crude levels. Refinery Utilization Rose by 1.2 points to 87.9% from 86.7% in the prior week. Total Motor Gasoline inventories fell 0.7Mb while Distillate volumes fell 0.8Mb. US Crude Production declined 100Kb/d to 11.4Mb/d. Total Demand rose by 2.34Mb/d to 21.63Mb/d as Other Oils demand rose by 2.20Mb/d. Gasoline consumption fell 18Kb/d to 9.24Mb/d which is just above the 9.19Mb/d consumed in 2019 at this time. Jet Fuel Consumption rose 206Kb/d to 1.38Mb/d versus 1.66Mb/d consumed in 2019 at this time. Cushing Inventories rose 200Kb to 26.6Mb/d.

Baker Hughes Rig Data: The data for the week ending November 12th showed the US rig count rose by six rigs up by six rigs in the prior week. Of the total of 556 rigs working last week, 454 were drilling for oil and the rest were focused on natural gas activity. This overall US rig count is up 78% from 312 rigs working a year ago. The US oil rig count is up 93% from 236 rigs last year at this time. The natural gas rig count is up a more modest 40% from last year’s 73 rigs, now at 102 rigs.

Canada had a rise of eight rigs (a decline of six rigs in the prior week) to 168 rigs. Canadian activity is now up 89% from 89 rigs last year. There were six more oil rigs working last week and the count is now 101 oil rigs working, up from 39 last year. There are 67 rigs working on natural gas projects now, up from 50 last year.

The material increase in rig activity over a year ago in both the US and Canada should continue to translate into rising liquids and gas production over the coming months, especially with the DUC count (drilled but uncompleted well count) at very low levels. The data from many companies on their plans for Q4/21 and forecasts for 2022 support this rising production profile expectation. We expect to see US crude oil production reaching 12.0Mb/d before the end of 2021. Companies are taking advantage of attractive drilling and completion costs and want to lock up experienced rigs and crews as staffing issues are getting tougher for the sector.

Conclusion:

Bearish pressure on crude prices:

- Covid caseloads are growing around the world. In the US, the death rate is over 764K deaths (up 8,000 during the last week). Worldwide, the death count is now 5.11M. Deaths are rising in Europe particularly in Austria (imposing lockdowns on the unvaccinated with fines of $30K if they leave homes when not essential), Bulgaria, Croatia, Germany, Netherlands, Romania, Russia, Slovakia, Slovenia, and Ukraine.

- Many US corporate and government employees are not planning on getting vaccinated and are now being put on unpaid leave and may soon lose their jobs. Eighty million individuals have a shotgun decision by January 4th (delayed by one month to cover off Christmas deliveries) when the cut-off kicks in. NO JAB, NO JOB is the vaccination mantra. The US military, police and firefighters are being significantly affected.

- Energy demand is under pressure as high prices for most food, rent, taxes, child care, health expenses, auto costs and other daily necessities make spending decisions tougher for consumers. This gouge in prices will surely impact consumers’ buying behaviour in the coming months. The spending pie of consumers is shrinking and some spending habits of the past will have to be dropped. Demand destruction is on the way. Real US GDP grew 6.7% in Q2/21 and was seen at only 2% in Q3/21. Recent economic releases indicate that we may already be in the early stages of a recession. The US$1.2T infrastructure bill signed into law by President Biden will only add to US inflationary pressures.

- The UAE and the IEA now see 2022 as having sufficient supplies and that inventories will start to build after winter 2021-2022 is over. We concur!

- China has seen a rising wave of new infections in 19 of its 31 provinces. Many industrial plants in China have been closed due to the high cost of fuel and the Government’s plan to lower emissions in the Beijing area for the upcoming 2022 winter Olympics from February 4th to the 20th. Clean air is needed for the event and China wants to show it is making progress on its climate initiatives. China’s General Administration of Customs reported yesterday that imports of crude oil in October were down by 1.5Mb/d from 10.5Mb/d to 9.0Mb/d as the smog issue was being focused on. They are breaking US sanctions by buying 560Kb/d from Iran and 57Kb/d from Venezuela, leaving less oil to non-sanctioned OPEC members under the deal provisions. In Monday’s virtual meeting between President Xi and President Biden they discussed using their Strategic Petroleum Reserves (SPR’s) to lower prices in their domestic markets and send a warning signal to OPEC+ that current prices are unacceptable. If they cut back or ordered nothing from OPEC for some set period of time, OPEC would be in big trouble quickly.

- Iran is returning to the negotiating table on November 29th and if progress is made, then at some point in the future they may get sanction relief and be able to add 1-2Mb/d fairly quickly.

Bullish pressure on crude prices:

- Speculative long investors (options traders, hedge and commodity funds) and a short squeeze on bearish positions in the futures and options markets on crude have spiked up prices. Energy bulls like Bank of America see US$120/b by June 2022.

- Spot natural gas prices in Europe have backed off after President Putin confirmed that Russia would meet all European winter needs once they open the Nord Stream 2 Pipeline, which is now being filled and undergoing pressure tests before certification. This new pipeline doubles Russia’s annual export capacity to Europe. The most recent problem/delay is that German regulators want Nord Stream to set up a German company with a headquarters and manpower before completing the regulatory requirements. This was supposed to be completed in January 2022 in time for the worst of winter natural gas needs but may now be delayed by four months. Natural gas prices in Europe have lifted again and this is supportive of crude prices.

- In the US, NYMEX today is now at US$5.12/mcf – and in Canada AECO is C$4.37/mcf as storage levels have been built up sufficiently for a normal winter. US storage injections for the last six weeks have been above the five year average and over 2020 injection levels.

CONCLUSION:

WTI is down nearly 2.5% or US$2.03/b today to US$78.73/b as the US and China bring pressure on OPEC+. We see prices as having US$20-25/b of speculative value which should disappear as demand weakens in the US and China as they both could be headed into recessions. If the data comes out supporting recession conditions, the oil price slide could be quick and painful. Leveraged speculative longs in crude oil futures are vulnerable to nasty margin calls in the future.

Energy Stock Market: The S&P/TSX Energy Index currently trades at 165, flat with last week. The S&P Energy Bullish Percent Index backed off from the 100% SELL level to 80.9% now. Energy stocks could fall 30-40% in the coming months with leveraged entities the hardest hit.

Our November Schachter Energy Report Monthly comes out Thursday November 25th with details on the general stock market and its expected impact on the energy sector as well as reviews and updates on 25 companies that have released their Q3/21 report since our Interim Report.

We held our 90 minute Q4/21 quarterly Black Gold Webinar on Wednesday November 10th at 7PM MT. It was very well received. We discussed in detail our view on the general stock market, the energy market and our bearishness on both areas for the near term. We also discussed the companies that had already reported their Q3/21 results. They are broken up into presentations on those that reported good results (11 companies) and those with not so good reports (nine companies). We had two Q&A sessions to go over our presentation materials and subscriber questions.

Become a subscriber if you would like to access the archive of the webinar and all our previous SER reports. Go to https://bit.ly/34iKcRt to subscribe.

If you enjoy reading our weekly ‘Eye on Energy’ feel free to forward it off to friends and colleagues. We always welcome new subscribers to our complimentary macro energy newsletter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair