Uncategorized

High-performance magnet producers in the US are calling on the government to unite federal agencies in tackling a perceived looming rare earth metals “supply crisis”.

This follows the decision by Arnold Magnetics to sell one of its Chinese businesses to invest in rare earth production in a venture with Chevron oil offshoot, Molycorp Minerals, in the US. Arnold also plans to increase magnet production in Europe (Metal Powder Report, February 2010).

….read more HERE

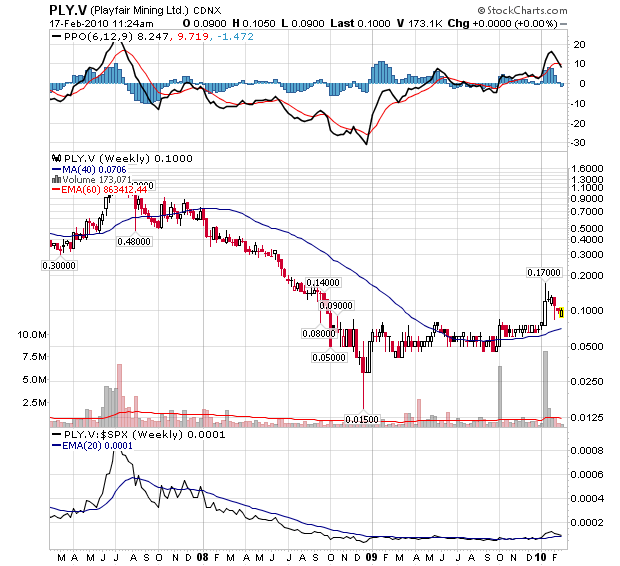

Playfair Mining Ltd. (CA:PLY 0.10, 0.00, 0.00%) is pleased to announce that it has entered into an option agreement with Rare Earth Metals (TSX.V-RA) on its six large claim REE blocks in central Labrador. The six Playfair claim blocks, containing 313 claims covering a combined 7,825 hectares, are located in the Letitia Lake – Red Wine region covering highly prospective ground which is enriched in both rare metals and rare earth elements (REE).

…..read more HERE.

“Newcrest also announced an updated indicated and inferred resource for its O’Callaghans deposit of 78 million tonnes containing 260,000 tonnes of tungsten and 220,000 tonnes of copper.

Mr Smith later told journalists the deposit had a fair bit of importance strategically, given only 100,000 tonnes of tungsten was produced each year and 80 per cent of the market was controlled directly by China.

‘‘So they basically control the market.‘‘

It’s been declared by China as a strategic metal.

‘‘There are companies around the world who need tungsten but are finding it difficult at the moment to find access to long-term supply.’’

…..read more HERE and HERE. (Newcrest is an Australian Stock which engages in the exploration, development, mining, and the sale of gold and gold/copper concentrate in Australia, Fiji, Indonesia, Papua New Guinea, Peru, Canada, and the United States. It also involves in the exploration and sale of silver ores. The company primarily owns and operates six mines, including five located in Australia and one in Indonesia. As at June 30, 2009, it had gold reserves of 42.8Moz and copper reserves of 4.67Mt. Newcrest Mining Limited was founded in 1966 and is headquartered in Melbourne, Australia.

AlphaNorth Asset Management runs a Canadian small-cap, long-biased hedge fund that tries to maximize the risk-reward ratio on its investments.

How?

“We evaluate all the investments in the portfolio every week and if something comes along that offers more attractive upside versus the downside risk, we’ll swap it out,” said AlphaNorth President and Chief Executive Steven Palmer.

The fund – called AlphaNorth Partners Fund – offers tax-deferred investment returns, thanks to a forward agreement with TD Global Finance, part of Toronto-Dominion Bank (TD), meaning unitholders pay no tax until unit redemption.

The fund tends to focus on companies with a market capitalization of less than C$100 million. “Banks’ small-cap funds usually have a cut-off of around C$100 million so

they’re not looking at the companies we’re looking at; there are a lot of opportunities to get involved prior to the company going mainstream,” he said.

Aeromechanical Services, Puget, Colossus Stand Out. The fund is diversified, less than C$50 million in size and comprises some 50 names. Roughly half the fund revolves around resource-based stocks, with the rest a mixture of technology, biotech and special situations, the latter being companies that are, say, sitting on a unique or niche product.

Palmer likes Aeromechanical Services Ltd. (AMA.V), which provides real-time data communications for the aerospace industry by using the Iridium satellite network. It has also recently launched a fuel-management program to help airlines optimize fuel consumption.

“They just turned cash-flow positive in the last quarter, which is a good milestone,” Palmer said. “They’re getting traction in the market and bidding on a lot of new business.”

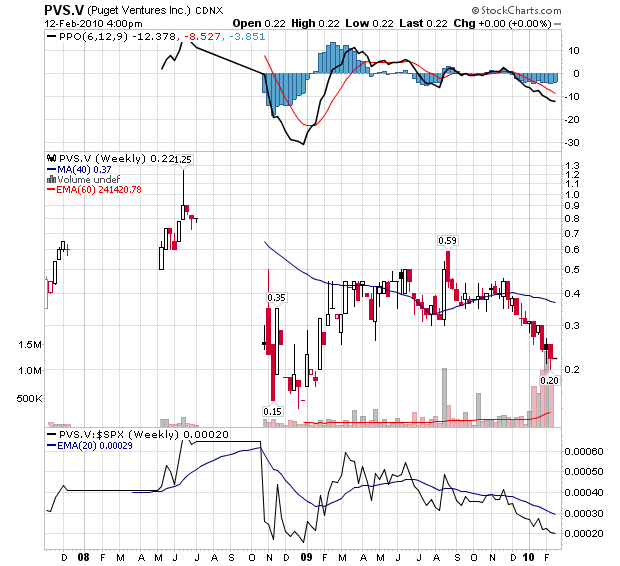

Puget Ventures Inc. (PVS.V), an early-stage cobalt company, is in the portfolio, in part because AlphaNorth has been watching how electric-car initiatives have ramped up demand for viable electric batteries. While this has pushed valuations for lithium-based companies higher, Palmer said the market hasn’t fully realized that three times as much cobalt as lithium is used in electric batteries.

“(Puget) is much closer to production than some lithium companies; the property produced cobalt in the 1940s,” Palmer said. “It has a unique deposit; it would be the only primary cobalt operation in Canada.”

And then there’s Colossus Minerals Inc. (CSI.T), an exploration company focused on developing Brazilian gold deposits. “They’ve had some phenomenal results on the property, some of the best drill results I’ve ever seen in terms of value,” Palmer said. “They will continue to put out good results and the company will eventually be taken over.”

Company Web site: http://www.alphanorthasset.com

-Brian Truscott, Dow Jones Newswires; 604-669-1595;

brian.truscott@dowjones.com

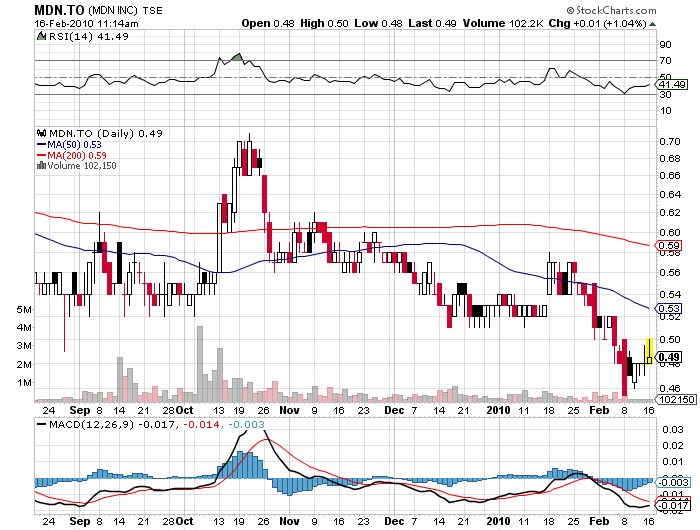

MDN Inc. (CA:MDN 0.49, +0.01, +2.08%) is a mining exploration and development company having adequate financial resources to develop its promising projects in Quebec and in Tanzania.The company also owns a 67.5% interest in Mineraux Crevier, which owns a property with a NI 43-101 niobium and tantalum resource located in the Lac St-Jean area of Quebec. MDN has an option to increase its equity participation in Mineraux Crevier up to 87.5%. Additional information is available on MDN’s website at www.mdn-mines.com. MDN also remains active in the search for new business opportunities that can raise shareholder value. In addition to its 30% participation in the Tulawaka Gold Mine, MDN is the operator and owner of a majority interest in mineral licenses totalling 621 sq km around the Tulawaka gold mine in Tanzania.

MDN Inc. (CA:MDN 0.49, +0.01, +2.08%) announces that it has increased its participation in Mineraux Crevier Inc. (MCI) from 38.5% to 67.5% by acquiring the equity interests of minority shareholders. The two shareholders of MCI are now MDN with 67.5% and IAMGOLD with 32.5%.

The acquisition was paid in cash for an amount of $582,750 and by the issuance of 3,349,777 common shares of MDN Inc.

As a reminder, MCI holds 100% of a niobium and tantalum project, located north of Lac St-Jean in the province of Quebec. A feasibility study on the project is currently ongoing.

Additional information is available on MDN’s website at www.mdn-mines.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair