Uncategorized

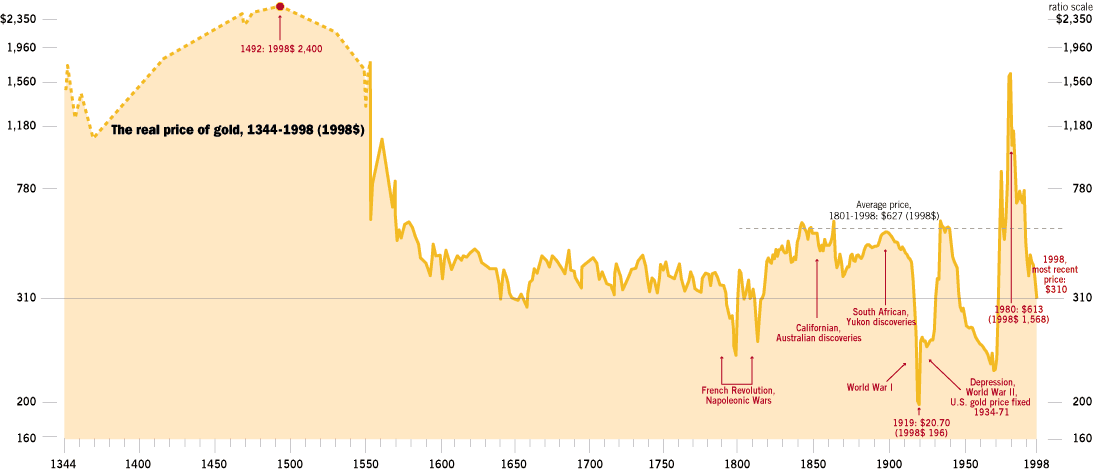

Click on image for Larger view Acquire gold, accumulate silver:

Gold is an expensive commodity and the most demanded precious metal. The measure of risk in Gold is bare minimum in longer run and is almost negligible in shorter run as investment compared to other investment tools such as currency & stocks. Even compared to other consumable precious metals, gold has stood its worth for centuries and persevered the tides of time. Many experts convert their fixed assets or long term investments in gold so that they can hedge timely against the inflation.

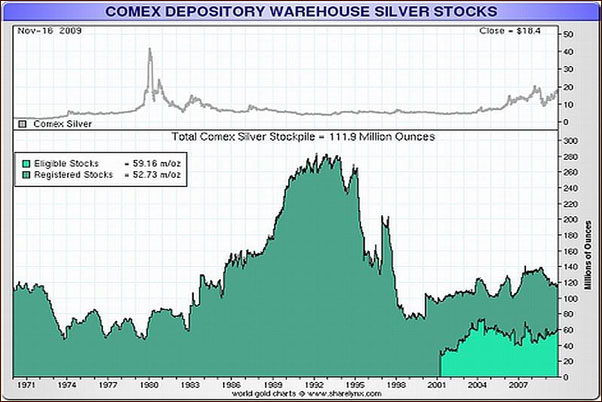

Silver on the contrary has a lesser price bracket but there is tremendous potential present in silver due to its widespread demand. People want to now accumulate silver for various reasons. One particularly is due to the fact that citing reference to the worst economic/hyperinflation scenario in Zimbabwe people have taken notes for a situation where the currency will lose all it purchasing power and then silver will be used as trading commodity for every day consumption. In this event the demand of silver is on an upward consistent curve and supply is speculated to drop due to its high demand in hi-tech IT & electronic industry. Thus silver is considered to carry more potential thus for price shoot.

Click on image above for Larger view

History of Gold & Silver:

Experts call Gold & Silver real money; which itself is based on their long history of serving as currency & a mode of exchange. Since ancient times these two precious metals have been treated as something related to value or worth, whether it is religious purity or jewelry for the purpose of fashion & beautifying, these precious metals were always meant for valuables.

It could be their shine, color or shape that attracted human beings towards it but it was the people in the regions of Transylvanian Alps or in the territory of Mount Pangaion in Thrace who started mining it to use them for decorative purpose that exhibited their prosperity. Till today the financially educated and elites use it to ensure their continuous well-being.

The greatest opportunity in history – Gold Silver Mania:

The recent economic recession has raised concerns for many who thought that they fell prey to unsupervised economic plans and yet there were others who were shielded against it through precious metal buying which always indicated and preached about long-term profits.

Triggered by the success of the precious metal owners; now there is gold & silver buying mania everywhere; as they see these times as the greatest opportunity ever to rebuild on the mistakes of US & western fiscal policies. This way people were not only able to guard themselves but they were also able to capitalize on the profits created by the real intrinsic worth of precious metals.

Now people are converting and securing all their cash and liquid assets into precious metals by buying precious metals such as silver and gold, and there is a world-wide awareness campaign through which people are preparing themselves for future profits while covering up past losses.

Silver will play as the major currency worldwide due to its low price (as compared to Gold), easily exchangeable feature and ability to purchase everyday consumables. It’s demand is going to be much more vast as compared to gold, particularly in developing economies silver is going to be replace gold and will be main mode of exchange even on the higher level. Gold will be fundamentally used as saving instrument which will be cashed (for a smaller currency bill) to silver in order to make it viable/convertible for every day buying. Therefore the excruciating demand and limited availability and supply of silver are going to drive its value manifolds and its price will show dramatic movement in the times to come.

This article provided by Dr. Atif Khan, Ph.D of Sunshine Profits

We are investors, who take this profession very seriously. We spend a LOT of time doing various researches, finding correlations and investigating historical patterns, so that you don’t have to. Przemyslaw Radomski, Sunshine Profits’ main editor, founded this Website, as he felt that although there are numerous valuable services on the Internet, investors, could use some additional guidance, especially when it comes to timing these volatile markets.

Here, at Sunshine Profits we believe that we are in a secular bull market in all commodities and that precious metals will be among its greatest beneficiaries. Once established long term trends, our investment strategy focuses on evaluating low-risk entry points, as well as timing potential tops.

…..read more HERE

What If the U.S. Dollar Crashes Overnight?

One of the questions that we’ve received last week was about the possible non-confirmation between gold at new highs and both silver and stocks lagging well beneath their old highs. The question is if such a non-confirmation becomes a source of worry at some point, since these three sectors traditionally move together.

The answer is the one that every economist likes to give when being asked just about any question – it depends. In the long run fundamentals drive prices of assets and the precious metal market is not an exception from this rule. As long as fundamentals are in place, the bull market in the precious metals will continue. There are several signs (as featured in the “Top or Not?” list in the Tools section on our website) that will tell us that this is indeed the ultimate top – we don’t see them yet.

The declining general stock market may continue to put a negative pressure for mining stocks and (especially) silver until we get to the final stage of the bull market (actually, we expect high rates of return even from stocks that don’t mine gold nor silver, but that are just named “golden something” or “silver something”.) In case of silver, we might also see sharply higher values in case of a problem with delivery of silver on COMEX. However, until either of them takes place, we might continue too see underperformance of these two parts of the precious metals market if the world stock indices move lower.

In case of silver, we don’t think it would invalidate its final rally or make it anything less than breathtaking, but it could certainly delay it. In a way, lower values of the main stock indices are good for long term silver investors, because they would allow to buy as much silver as possible at relatively low prices before the silver market takes off.

As for the mining stocks, the situation is quite different, as they are not that likely to outperform metals during the final stage of the rally. However, in case of gold and silver stocks, the history suggests that the positive correlation with the general stock market is likely to wear off sooner or later. Please note that from 2001 to 2003 gold stocks managed not only to rise, but also to outperform gold along with declining stock market.

Therefore, the disproportion between gold’s performance and the one of silver and mining stocks does not change the fundamental situation for the whole precious metals market, and consequently, does not make us concerned, as there is a good explanation behind it in the form of declining stock market.

There’s one more thing that we would like to comment on in this essay, as we’ve been also asked about the final stage of the rally, and what would be the use of the having massive gains on one’s mining stocks, if they would be priced in the U.S. Dollar that could be worthless at that time. That is true that the final stage of the bull market in the precious metals market could correspond to a financial instability to say politely, but fortunately we are in this market to maximize our chances of even increasing our wealth during these difficult times.

Let’s split the above question into two separate matters. The first one is “how do I know that I won’t lose everything I have if the U.S. Dollar collapses overnight” and the second one would be about the gains in mining stocks when the U.S. Dollar is worthless.

The first question is all about owning physical metals. If you own physical metals, keep them in a safe place, or even better it is spread among several “safe places”, it seems that you could sleep well at night. If the USD collapsed overnight, the increase in the value of the precious metals holdings would be so massive that just a 10% in gold/silver should more than make up for the losses in your “paper wealth.” So, by following the rules listed in the Key Principles section you would have about 20%-25% of your portfolio in physical metals and an overnight dollar collapse could in fact massively increase your wealth. Therefore, you’re protected at all times.

The second question is about protecting one’s profits in mining stocks or from other speculative vehicles. Generally, it does not need to overly concern you either, because – as mentioned above – mining stocks are not likely to outperform metals during the final stage of the bull market. Therefore, we will strive to detect when it is not likely that mining stocks’ outperformance will not return soon, and we will suggest switching directly to metals, just like we are now suggesting owning gold instead of silver and mining stocks (of course this is because of the short-term uncertainty regarding the last two markets, not because we believe that the bull market is close to being over.)

This is not recommended for most Investors, because could decrease one’s profitability, but if you are particularly afraid that you could lose your speculative capital because of the death of the U.S. Dollar, you might want to put 10-90% of your profits from each trade (depend on how afraid you are) in mining stocks directly to physical gold or silver. In this way you will be sure that the relative amount of physical metals in your possession is constantly rising, and at the same time the amount of “paper wealth” at risk (here: stocks) decreases. Again, the price here is limiting your exposure to profits from speculation on mining stocks, so it’s a trade-off.

Summing up, the long-term direction in which the precious metals is likely to go is still up, and if you prepare yourself accordingly, you should be able to preserve your wealth, and probably even increase it, even if the current financial system would cease to exist in the current form. Meanwhile it might be a good idea to earn money along the way by trading gold, silver and mining stocks.

To make sure that you are notified once the new features are implemented, and get immediate access to my free thoughts on the market, including information not available publicly, I urge you to sign up for my free e-mail list. Sign up today and you’ll also get free, 7-day access to the Premium Sections on my website, including valuable tools and charts dedicated to serious PM Investors and Speculators. It’s free and you may unsubscribe at any time.

Thank you for reading. Have a great weekend and profitable week!

P. Radomski

Click HERE to test the Premium Service FREE of charge

The USD Index and gold both moved slightly in the past few days, while stocks moved relatively higher – does this mark a significant change in the previous trends, or was this just a small pause? In addition to providing you with extensive answer to this question, we discuss gold role as an inflation hedge, and the meaning of the current divergence between gold, silver and mining stocks. We also explain, which part of the precious metals market is currently most appealing to precious metals Traders.

This week’s update includes 19 charts/tables including i.a.: the USD Index, the Euro Index, general stock market, gold, silver, the HUI Index, GDX ETF, precious metals correlation matrix, the Broker-Dealer Index, and the GDX:SPY ratio. Additionally, this week’s Premium Update includes the ranking of our top gold, and silver juniors. We encourage you to Subscribe to the Premium Service today and read the full version of this week’s analysis right away.

Patience and bravery are key to reaping the metal’s rewards

Not too long ago, analysts were cheering the metal’s prospects in the face of a recovering global economy and strong prices for gold, but the metal has so far failed to perform as well as many expected.

Silver “has the most potential of the metals and will … outperform gold — but it will take time,” said Julian Phillips, an editor at SilverForecaster.com.

Analysts remain upbeat about the longer-term potential, but warn that the short-term journey will continue to be rough.

“Silver, like all investments, will reward those who are patient and who have a long-term view,” said Mark O’Byrne, a director at GoldCore, an international bullion dealer.

That patience has already been sorely tested.

Late last year, analysts were touting the metal’s promise as a much cheaper investment alternative to gold that was poised to see higher industrial demand. Some even predicted a price climb above $20 an ounce by the end of 2009, but instead, prices dipped below $15 in February. See previous Commodities Corner on poor man’s gold.

“The overall demand for silver is down compared to gold,” said David Beahm, a vice president at precious metals retailer Blanchard & Co. “Since silver’s price is driven much more strongly by global industrial demand rather than investor demand, it has underperformed as compared to gold.”

‘Silver, like all investments, will reward those who are patient and who have a long-term view.’

Silver has “underperformed significantly over the long term,” said O’Byrne. But “this under performance will be rectified in the coming months and silver will also reach the record highs that gold has reached.”

In the meantime, silver’s short-term performance hasn’t been too shabby.

O’Byrne pointed out that in the past year, silver prices have climbed more than 31%, much larger than gold’s more than 19% rise, and while gold prices fell almost 1% in the past month, the price of silver rose 1.7%.

Potential shine

From here, it’s anyone’s guess where silver prices will go.

True, if there’s another deflationary crash and equities come under pressure again or if the U.S. fiscal position were to “miraculously” improve in the short term and the U.S. dollar again be the trusted safe-haven currency in the world, silver could again fall, said O’Byrne.

And “if the global economy does not improve over the next two years, silver will remain range bound,” said Beahm. “If the global economy further deteriorates, silver will struggle.”

On that same note, the global economy would need to improve further in order for silver to move significantly higher, given that silver is used primarily as an industrial metal, as well as for investment purposes, he said.

……read Page 2 HERE

Click on Chart for Larger version

Gold vs. silver –Silver has been known as the “poor man’s gold.” Silver used to be treated as a monetary metal. No more. Today no central bank holds silver as part of their reserves. However, silver has an historical relationship to gold. The historical average is that one ounce of gold would buy around 15 ounces of silver. The ratio is now out-of-whack at around 69, which means that compared with gold, silver is “dirt-cheap.” Richard Russell

Silver is closing higher last week at 18.25. Silver has alternated between up

and down weeks for the past 7 sessions. It is interesting to note the 7 week

moving average is near at 18.30. Silver lacks direction, but Gold is in a bull

trend, so we would expect the Gold Silver ratio to drift higher. The Gold Silver

ratio has actually dropped this week from 69.64 to 67.27. The ratio has

alternated in direction for the pasfor a move higher next week. – Scotia McLeod Gold & Silver Marketwatch From Commodity Online – Silver is closing higher the week at 18.25$. Silver has alternated between up and down weeks for the past 7 sessions.

It is interesting to note the 7 week moving average is near at 18.30$. Silver lacks direction, but Gold is in a bull trend, so we would expect the Gold Silver ratio to drift higher.

The Gold Silver ratio has actually dropped this week from 69.64 to 67.27. The ratio has alternated in direction for the past 6 weekly sessions so if this continues look for a move higher next week.

An unprecedented crisis in the silver marketcould easily hand you a long series of double… triple… even quadruple investment gains.

Here’s how…

You probably already know that every commodity fortune ever made was created by an imbalance of supply and demand.

When the demand for a certain commodity is high and supplies are low, prices skyrocket. And investors holding the commodity in question get rich.

This is exactly what has happened in the case of many natural resources just in the past decade alone:

- Crude oil shot up 620% in 6 years

- Gold is now up over 380% since 2001

- Natural gas soared more than 550% in 4 years

- Uranium spiked 830% in 4 years

- Copper increased nearly 530% in 7 years

- Palladium more than tripled in 3 years

- Platinum prices grew 430% in 6 years

- As demand grew and supplies dwindled, the prices for these natural resources ballooned in value.

But none of these commodities experienced the supply/demand crisis that silver is currently facing.

Take a moment to chew on this…

According to GFMS Limited — the world’s leading authority on precious metals markets — the total amount of above-ground silver supplies dropped by 86% last year.

This left the world with just about 20 million ounces of silver reserves.

At the same time, the world demands about 2.5 million ounces of silver per day.

That means the entire global supply of above-ground silver could be completely wiped out in just eight days!

Fortunately, silver production companies have been able to keep up with demand — but just barely…

Last year, silver miners were only able to increase production by just over 3%. And for the past 10 years, there has been no surplus in silver supplies.

This extremely tight supply/demand dynamic of the silver market has been terrific for investors that own the physical metal. Silver prices have increased nearly 350% since 2002.

But shareholders of the companies that pull the silver out of the ground have done even better. Here are three recent…

Silver stocks beating the markets

Silver Wheaton is the largest precious metals streaming company in the world. The company has thirteen long-term silver purchase agreements and two long-term precious metal purchase agreements.

These agreements allow the company to purchase all or a portion of the silver production at a low fixed cost from high-quality mines located in Mexico, the United States, Greece, Sweden, Peru, Chile, Argentina, and Portugal.

For 2010, Silver Wheaton expects to produce 22.2 million ounces of silver and 20,000 ounces of gold, for a total production of 23.5 million ounces of silver-equivalent.

By 2013, annual production is expected to increase significantly to 38 million ounces of silver and 59,000 ounces of gold, for total production of over 40 million silver-equivalent ounces.

Pan American Silver is the second largest primary silver producer in the world. The company owns and operates eight silver mines and four development projects in Peru, Mexico, Bolivia, and Argentina.

Pan American’s growth strategy is based on the continued increase of low cost silver production through the efficient operation and expansion of its existing mines, an aggressive exploration program, and the acquisition and development of new silver-rich deposits.

The company has increased silver production by 105% since 2004. Last year, the company produced 23 million ounces of silver from its Latin American assets. For 2010, the company anticipates increasing production slightly to 23.4 million ounces.

According to the latest estimates, Pan American Silver has 234 million ounces of silver reserves and 940 million ounce of resources in the measured, indicated, and inferred category.

The company also mineral reserves of 679,000 ounces of gold, 717,000 tonnes of zinc, 302,000 tonnes of lead, and 67,000 tonnes of copper.

Fresnillo plc is the third largest silver producer in the world and Mexico’s second largest gold producer. The company operates four producing mines and one development project, all located in Mexico. In total, Fresnillo has mining concessions covering approximately 1.75 million hectares across the country.

One of the main drivers of Frenillo’s growth is the investment in exploration and the development of projects and prospects with the potential to become low-cost operating mines. The company’s disciplined approach to investment includes the evaluation of economic ore grades, maximum extraction costs, and an established reserve base.

In 2009, Fresnillo increased silver production by 9% to a record 38 million ounces. The company also increased gold production by 5% to 277,000 ounces.

The company plans to bring one new mine into production each year until 2014. As a result, Fresnillo anticipates increasing silver production by another 50% to over 56 million ounces in the next four years.

In my most recent Wealth Daily report, I give details on another company that is expecting to ramp up silver production this year by 66.7%.

This increase in production is expected to boost quarterly operating cash flow by over 650%, which is exactly why the world’s biggest investment and financial institutions have been hoarding this stock.

To read my latest report for free, simply click here.

Good Investing,

Luke Burgess

Editor, Wealth Daily

Investment Director, Hard Money Millionaire

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair