Uncategorized

As the excitement surrounding the $3.6 billion buyout of tiny Andean Resources by Goldcorp Inc. (GG) subsides, investors are wondering who’s up for grabs next among Argentina’s other emerging success stories.

The task has been simplified by the fact that only two gold juniors have, to date, made sufficiently impressive gold discoveries to attract takeover speculation. One is Mansfield Minerals (MFMNF.PK), which has been quietly developing its Lindero gold discovery since as far back as 1999.

The other is Extorre Gold Mines (EXGMF.PK), which burst onto the mining scene just over six months ago after it was spun-off from high-flying Exeter Resource Corp. (XRA). Extorre inherited the high-grade Cerro Moro deposit from its parent company. However, only a hostile takeover could wrestle Cerro Moro from Extorre any time soon, according to the company’s management.

Having just completed a $40 million equity financing, Extorre says it’s committed to building considerably more value into the project by way of drill-defining plenty more high grade gold and silver. To date, a total of 612,000 ‘indicated’ ounces of gold equivalent (gold and silver combined) have been found in just one of the deposit’s many veins. All told, Extorre is targeting a two-million ounce resource in the same proximity and geological environment as Andean’s richly mineralized Cerro Negro deposit.

A third company worth mentioning is Australia-based Troy Resources NL (TRYRF.PK), which is an existing gold miner in Australia and Brazil. Troy is gearing up for its first gold pour this autumn at its low-cost, high-grade Casposo gold/silver project in Argentina’s mining-friendly San Juan Province.

This new mine is now fully funded and is therefore not for sale, according to Troy’s president Paul Benson – at least not for now. With 70 more drill targets, there’s plenty more upside potential for the discovery of significant additional ounces in the ground, he says. Furthermore, with a current reserve base of only 341,400 ounces of gold and 11.2 million silver ounces, it almost certainly does not meet the minimum size threshold to interest much bigger gold miners at this time.

That leaves Mansfield Minerals sitting pretty. The company has long groomed its ‘company-maker’ Lindero deposit for the right suitor. With gold prices vaulting to record highs, the timing is excellent, according to Mansfield’s president, Gordon Leask. This is why a bankable feasibility study (a final blueprint for a mine) is underway.

However, the company has already published key independently-assessed financial projections by way of a pre-feasibility study. One that unequivocally attests to the viability of a future gold mine based on current reserves of 1.9 million ounces. There’s also a further drill ‘inferred’ resource of one million ounces. This needs to be more clearly defined by way of additional in-fill drilling to be considered completely reliable.

Hence, “advanced talks” with one or more sizeable, expansion-minded gold mining companies are making headway, according to Leask. This surely comes as no surprise to the various mining analysts who have been covering this low-key gold story for nearly a decade.

Among the more recent enthusiasts is Joe Mazumdar, a mining analyst for the Canadian stock brokerage firm Haywood Securities Inc. After having crunched the key metrics in Mansfield’s pre-feasibility study, Mazumdar wrote a research report last April on the company encouragingly entitled: “Low Hanging Fruit.”

“The quality of the asset has been underpinned by its simplicity and low technical risk. It is the equivalent of a ‘mine on training wheels,’” he asserted in a 39-page report. Hence, his conclusion that Mansfield is “a prime candidate for takeover” and that the company could fetch “premiums of up to 250 per cent from its current price” in a takeover scenario.

But Lindero’s allure hasn’t gone unnoticed by a number of gold-hungry producers, according to Leask, who declines to elaborate. But he notes that there’s a scarcity of bargains in the junior gold space.

At least seven potential suitors, including Yamana Gold Inc. (AUY) and Eldorado Gold Corp. (EGO), have been identified by Haywood Securities among the world’s relative few mid-tier gold miners. (Notably, Eldorado just lost out in the takeover battle for Andean Resources after its US $3.4 billion proposal was outbid by Goldcorp).

So what is it about Lindero’s economic modeling that gives it so much credibility? Apparently, the deposit can produce around 160,000 ounces per annum in the first few years at a modest cost of US $373 an ounce. This is because much of the high-grade mineralization is near surface. And this scenario would offer an anticipated payback on capital costs within two years, based on minimum gold prices of US $1,100.

Furthermore, the deposit also benefits from being well suited to an open pit (quarry-like) heap leach (low extraction cost) mining operation. All told, a minimum 9.5-year mine life will translate into average annual yields of around 150,000 gold ounces for the bulk of the mine’s life – and at an average cash cost of US $407 per ounce.

Additionally, the renowned engineering firm that conducted the company’s pre-feasibility study, AMEC Americas Ltd., calculated a pre-tax net present value of US $490 million for the Lindero deposit, assuming US $1,100 gold prices. (NPV is a pivotal decision-making metric that is defined as the risk adjusted value of the deposit once all the borrowed capital costs are repaid).

Another Canadian investment bank, Paradigm Capital Inc., also views Mansfield as an obvious takeover candidate. In a research paper discussing the company’s pre-feasibility study, senior mining analyst Don MacLean made a good case for a likely takeover.

The Paradigm report, which was published last March, noted that Mansfield only has approximately 44 million shares outstanding and a low market capitalization. The report’s takeover conjecture comes into clearer focus when considering the fact that Paradigm assigned an after-tax net present value (NPV) of US $242 million to Lindero, based on US $1,100 gold prices. By using a much more cautious after-tax evaluation than the pre-tax version assigned by AMEC, Paradigm still was able to deduce that Lindero is worth more than three times the actual value of Mansfield, itself.

The Haywood research report also points to the fact that geopolitical considerations also weigh in Lindero’s favor. In particular the project is located in a remote, economically underdeveloped region of Salta Province that is actively soliciting foreign investment. Hence, Salta’s pro-mining government is actively soliciting foreign investment and is therefore supportive of Lindero, according to Leask. Similarly, the federal government is also onside, he adds.

This favorable situation, along with the absence of any environmental challenges, explains why Leask expects a mining permit to be issued before year’s end.

Mansfield Minerals, Extorre Gold Mines and Troy Resources may be well ahead of the pack towards producer status. But a growing number of other ambitious gold explorers are aggressively working to validate their own gold discoveries in Argentina. All of which have a shot at becoming the next ‘home run’ takeover success story.

Marc Davis is the publisher of www.Top40goldstocks.com, a performance-oriented table for Who’s Who of junior gold stocks. This web site also offers plenty of data, analysis and news about top-performing gold stocks.

Marc has nearly a quarter of a century’s experience in the mining-oriented venture capital marketplace as a former professional trader and as a research analyst and journalist. He also currently manages www.BNWnews.ca

YOU PROBABLY don’t need me to tell you that it’s pretty risky out there, says Brad Zigler at Hard Assets Investor.

The market, I mean. Which market, you may ask? Increasingly, it doesn’t matter.

The zag of the gold market has come to look very much like the stock market’s zig. Over the past month, the correlation between the S&P 500 and gold has shot up 60 percentage points. The fact that the coefficient is now at 38% should tell you that it’s gone from a risk-neutralizing negative value to a tag-along positive.

The turnaround, too, followed a near-vertical trajectory. Not that this hasn’t happened before. Over the past two years, the correlation coefficient has dropped with equal velocity, but not risen.

“Britain under its new leadership is going the austerity route. Chancellor Osborne set plans for 81 million pounds sterling of spending cuts, all in an effort to erase Britain’s deficit by 2015. Osborne’s plan will entail the loss of 500,000 jobs in Britain’s biggest austerity push since World War II. Osborrn will require larger pension contributions, and higher retirement age, Conservatives in Parliament cheered Osborn, crying “More, more” as the word of the new austerity program emerged. There was no sense of panic on the part of the British public, perhaps because Brits remember the austerity and pain they lived through during the dark and horrific days of World War II.

Ed Miliband, leader of the British Labour Party opposition, called the austerity plan “The biggest gamble in a generation. — a gamble with people’s jobs and livelihoods. No other leading economy is trying anything like it.”

Mr. Osborne may have the nation behind him now, but in a year with unemployment climbing and living standards falling, sentiments may be a lot different. Osborne claims that the drastic cuts have removed Britain from the “danger zone” that once occupied along side of Greece and Ireland. Osborne told the MPs, “It’s a hard road, but it leads to a better future. Today’s the day when Britain steps back from the brink.”

But it’s very different in Greece and France, neither country known for their work ethic. In both countries, riots have broken out over austerity plans. When the age of retirement was increased in France from 60 to 62, literally the whole nation went on strike. The French famously don’t like to work, they love their vacations and their short work-hour weeks.

With Britain setting the tone, it won’t be too long before the austerity route hits the US. The American folks at home never suffered terribly during WW II, nor have they suffered through Korea, Vietnam, Iraq or Afghanistan. This will change drastically in the years ahead as the full force of the deficits hits Americans since the year 1939, Americans have enjoyed one long party, due to inflation, over-spending, borrowing and leveraging. In my opinion, the party’s about over. And Britain is leading the way for the English-speaking nations.”

Richard Russell Note — I think Britain’s new austerity is going to rub off on the US. This could be one of the reasons why gold is correcting. Gold may be looking ahead to the time when the US will cut out all the QE and stimulus stuff and start facing the pain of its disastrous deficits. Hard to believe that the US could actually choose austerity, but I think Britain is leading the way.

Richard Russell One of the best values anywhere in the financial world at only a $300 a year, to get his DAILY Dow Theory Letters subscription HERE

Austerity be damned, at this rate Mr. Bernanke will go down in the history books as one of the greatest money creators ever to have walked this planet!

Never mind sky-high deficits and a crushing debt overhang, at its most recent FOMC meeting, the Federal Reserve all but guaranteed another round of quantitative easing.

While the American central bank did not officially expand its quantitative easing program last month, it did reiterate its willingness to institute more aggressive monetary policy measures in order to combat the risks of deflation. Furthermore, Mr. Bernanke did officially downgrade the Federal Reserve’s outlook for inflation.

The truth is that the US is insolvent and its policymakers will stop at nothing in order to avoid sovereign default. So, it should come as no surprise that at its latest meeting, the Federal Reserve downplayed the risk of inflation, thereby setting the stage for another round of money creation.

Make no mistake; Mr. Bernanke has already created copious amounts of money. Granted, the Federal Reserve’s previous monetisation was highly secretive, but you can be sure that it did occur. Allow us to explain:

You will recall that during the depths of the financial crisis, the Federal Reserve expanded its own balance-sheet and bought all sorts of toxic assets from the financial institutions. By doing so, Mr. Bernanke created money out of thin air and bailed out the major banks.

Thus, the banks were able to dump their garbage assets on to the Federal Reserve and once they received the newly created cash in exchange for these securities, they loaned this money to the US government by purchasing US Treasuries. In summary, in the previous round of quantitative easing, the Federal Reserve created new money and instead of lending it directly to the US government, it used the banking cartel as its conduit. Back then, not only did the Federal Reserve create more than a trillion dollars, it also dropped its discount rate to almost zero; thereby allowing banks to borrow money cheaply! It should be noted that since the banks were able to obtain such inexpensive funding from the Federal Reserve, they had absolutely no qualms about re-investing this capital in US Treasuries.

At first glance, the Federal Reserve’s stealth monetisation plan seemed flawless. The banks offloaded their toxic assets on to the Federal Reserve, they made fortunes by investing in US Treasuries and the American government got access to a cheap source of funding. Magic!

Despite the fact that this financial wizardry was a lifeline for American policymakers and their banking cronies, let there be no doubt that it was an unmitigated disaster for the American public. Not only did the Federal Reserve nationalise the banks’ losses but more importantly, Mr. Bernanke’s money creation efforts have seriously undermined the viability of the US Dollar.

It is noteworthy that since bailing out the major banks and orchestrating the stealth monetisation, the Federal Reserve has been busy purchasing US Treasuries. Furthermore, it is now almost certain that in next month’s FOMC meeting, Mr. Bernanke will unleash yet another round of quantitative easing. In other words, in order to fund Mr. Obama’s out of control spending, Mr. Bernanke will create even more dollars out of thin air! Allegedly, this new round of money creation will drive interest-rates lower, thereby helping the US economic recovery. Or so the story goes.

Unfortunately, as any serious student of economic history knows, there is no such thing as a free lunch. By adding trillions of additional dollars to the monetary stock, Mr. Bernanke may succeed in bailing out his friends in high places but he is seriously jeopardising the US Dollar. In fact, bearing in mind the recent developments, it has become clear to us that the Federal Reserve wants to debase its currency. In our humble opinion, the US Dollar is a doomed currency and there is a real risk of an abrupt plunge in its value.

If our assessment turns out to be correct and Mr. Bernanke unleashes the second phase of quantitative easing, you can be sure that the US Dollar will slide against most un-manipulated currencies (which are few and far between) and hard assets. In fact, monetary inflation is the prime reason why we believe that the ongoing bull-market in stocks and commodities will continue for several more months.

Look. The US economy is swimming in debt and the total obligations (including social security, Medicare and Medicaid) now come in at around 800% of GDP! Furthermore, this year alone, Mr. Obama’s administration plans to spend another US$3.5 trillion, meanwhile the US Treasury will raise roughly US$2.2 trillion from issuing new government debt! Clearly, these numbers are unsustainable and you can bet your bottom dollar that the Federal Reserve will end up buying a large proportion of the newly issued US Treasury securities. As the American central bank funds more and more of Mr. Obama’s spending by creating new money, it will trash the value of its currency. In fact, given the growing imbalance between the government’s spending and tax receipts, very high inflation is inevitable and even hyperinflation cannot be ruled out.

For the sake of their financial well being, it is crucial that investors understand that inflation or even hyperinflation is a monetary phenomenon and a strong economy is not a pre-requisite for the debasement of a national currency. Whatever the reason, if a central bank decides to significantly increase the quantity of money in the system, that currency’s purchasing power will always diminish. This is how fiat-money regimes have operated since the beginning of time and this era is no different.

It is interesting to note that throughout recorded history, the worst excesses of inflation occurred only in the 20th century. Undoubtedly, this was a direct consequence of the adoption of fiat-money.

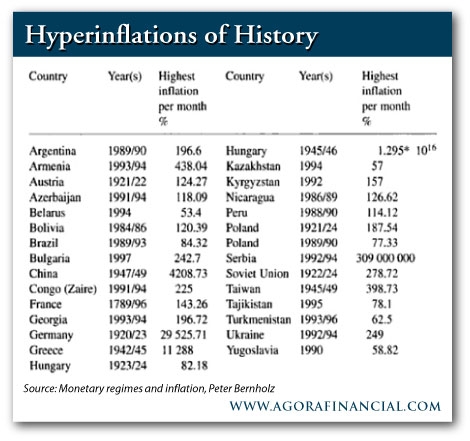

The following chart highlights all the hyperinflationary episodes in recorded history and as you can see, with the exception of the French Revolution (1789-1796), all of the other disasters occurred in the last century. In fact, it is an ominous sign that 29 out of the 30 recorded hyperinflations in human history occurred during the 20th century!

Let there be no doubt, a paper money system usually ends in the reckless destruction of money and it is no coincidence that all hyperinflations in history have occurred in the presence of discretionary paper money regimes. Furthermore, it is important to understand that a political system based on democracy is inherently inflationary and political leaders have been responsible for all major inflations in the past. Conversely, history has shown that monetary systems binding the hands of political leaders are essential for keeping inflation in check. If history is any guide, metallic monetary systems have shown the largest resistance to inflation and this is due to the fact that currencies anchored by a tangible asset cannot be inflated ad infinitum.

It is our conjecture that the current monetary system is absolutely pathetic; a system designed to enslave society. Unfortunately, the vast majority of humans do not understand the endless inflation agenda and this is why the perpetrators get away with this crime. Furthermore, let it be known that the Federal Reserve is largely responsible for the incredible inflation we have experienced over the past century.

The chart below plots the cost of living in Britain, France, Switzerland and the US. As you will note, the cost of living in these nations was relatively stable for over 160 years (1750-1913) but once the Federal Reserve came to power in 1913, everything changed. Suddenly, the cost of living exploded in these nations, so it should be clear that the Federal Reserve’s covert policy of currency inflation and debasement is solely responsible for this mind numbing inflation.

Unfortunately, the Federal Reserve and its allies have not finished inflating and over the following years, they will create even more confetti money. Under this scenario, cash will continue to lose purchasing power and the asset poor middle-class will get even more impoverished. If our assessment is correct, cash will prove to be a disastrous ‘asset’ over the next decade and once the Federal Reserve’s manipulation ends, fixed income securities will also depreciate in value.

Bearing in mind our grave concern about high inflation and the very real possibility of hyperinflation, we continue to favour hard assets such as precious metals and energy. At present, we have allocated roughly half of our clients’ capital to these sectors and it is our belief that this should be an adequate inflation hedge.

Regards,

Puru Saxena,

for The Daily Reckoning Australia

Puru Saxena publishes Money Matters, a monthly economic report, which highlights extraordinary investment opportunities in all major markets. In addition to the monthly report, subscribers also receive “Weekly Updates” covering the recent market action. Puru Saxena is the founder of Puru Saxena Limited, his Hong Kong based firm which manages investment portfolios for individuals and corporate clients. He is a highly showcased investment manager and a regular guest on CNN, BBC World, CNBC, Bloomberg, NDTV and various radio programs.

I probably don’t have to tell you that it’s pretty risky out there. The market, I mean. Which market, you may ask? Increasingly, it doesn’t matter.

The zag of the gold market has come to look very much like the stock market’s zig. Over the past month, the correlation between the S&P 500 and gold has shot up 60 percentage points. The fact that the coefficient is now at 38 percent should tell you that it’s gone from a risk-neutralizing negative value to a tag-along positive.

The turnaround, too, followed a near-vertical trajectory. Not that this hasn’t happened before. Well, in recent history; that is, over the past two years anyway. Check that. the correlation coefficient has dropped with equal velocity, but not risen.

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair