Wealth Building Strategies

‘Discipline yourself and others won’t need to.’

‘Discipline yourself and others won’t need to.’

– Coach John Wooden

Everybody needs a plan! Coaches have a game plan. Pilots have a flight plan, investors have an investment plan, architects create a building plan, and the list goes on. Nothing of great substance happens without a plan. Of course, plans are not worth the paper they are written on if they don’t elicit action.

Losers plan, plan, and plan some more. Winners Plan for success, Do something, Check the results, Act again to make the plan better, and then repeat the whole cycle.

Plan-Do-Check-Act

The first time I came across this concept when I was learning Statistical Process Control (SPC) as a young engineer with the Ford Motor Company. At the time, Ford was embracing the teachings of Edward Deming and instructing every employee on the fundamentals of statistical measure and process improvement. We quickly implemented statistical analysis on key processes to compare the actual process performance with the planned performance. Using this technique, we quickly discovered any deviation from the plan and took the necessary steps to understand the problem, correct it, and improve the process. This rapid plan, do, check feedback struck me intensely. I realized if this could work so effectively at a small level, surely it could work on a big level.

In subsequent companies, I used this concept at a strategic level. I would ensure a strategic plan was in place, execute the plan with the right level of detail, commitment, and infrastructure to do a great job, measure our results and then modify accordingly. Over time, this simple cycle became embedded into the culture until it became a habit. If it works for some of the biggest, most profitable companies in the world, then it can work for you.

When planning for a project, do the following:

Plan: Make a clear, concise and action-oriented plan of what you intend to achieve including specific goals, measures, and resources and steps necessary to obtain success.

Do: Execute the plan immediately, ensuring you have the right resources in place, coordination of activity, incentives, alignment, and accountability. Focus and play to win.

Check: Measure the results of your action in a clear, accurate and timely manner, and communicate those results with all who need to know.

Act: Determine how your results vary from the plan, and then take the action necessary to make improvements, based on this deviation.

This simple Plan-Do-Check-Act routine can be applied to all types of organizations, and even at a personal level, in order to focus actions and improve results.

related:

Recently the Stock Market moves down are fast and deep. This shows a way to make money from falling stock prices, and the process of identifying stock market dogs to protect yourself from a rising market – Ed.

I get a lot of questions about short selling, probably because most investors have never done it.

Short selling is the sale of a stock that is not owned by the seller in anticipation that the stock’s price will decline, enabling it to be bought back at a lower price to make a profit. If you can identify stocks before they fall, you can make a bundle of money via short selling.

To help you understand the mechanics and opportunity of short selling, I want to walk you through my most recent successful short sale to help you decide if short selling is right for you.

On April 7 of this year, I sent out this alert to my Rational Bear subscribers, telling them to “short” Conn’s, Inc. (CONN).

Conn’s is a large furniture and appliance retailer, but what’s unusual about it is the fact that it both sells furniture/appliances and loans its customers the money to buy its furniture/appliances. Sort of like General Motors and General Motors Acceptance Corporation (GMAC).

On the surface, Conn’s appeared to be growing quite well by selling an increasing number of products, but it was doing so by extending credit to just about any deadbeat that walked through its doors.

You and I may not need to borrow money to buy a washing machine or a color TV… but 80% of Conn’s customers do. Those are the kind of people I grew up with, and while they may be decent people, they are not the kind of people I’d want to loan money to.

That strategy started to backfire when the Conn’s finance division reported a massive $43.2 million quarterly loss. At the time, I said, “Those credit losses are going to get worse.”

How did I know that?

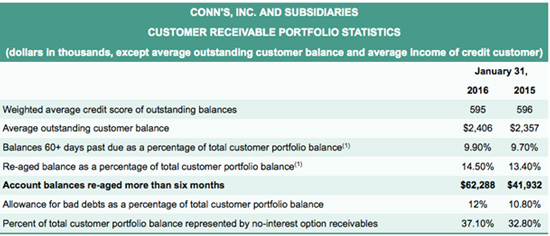

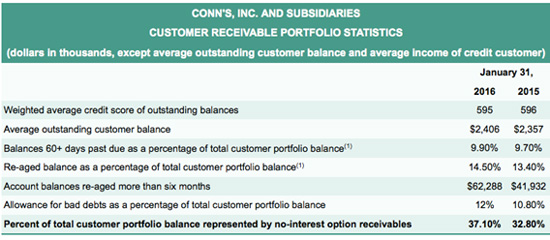

- The number of loans that were more than 60 days past due jumped to 9.9%.

- Most businesses reconsider their lending practices when bad loans skyrocket, but not Conn’s. Instead, it was loaning more than ever; accounts receivable increased by 16% to $743.9 million at the end of the first quarter.

- Conn’s increased its provision for bad debts by 11% to $64.8 million, but that wasn’t enough, considering the pace its customers were defaulting.

Those were serious red flags, but the biggest warning sign was the “creative accounting” Conn’s used to make its business appear better than it really was.

Accounting Trick #1: Re-Aging Bad Debt. There is a little-used but legal accounting practice called “re-aging” debt. It is used to reclassify deadbeat loans into not-deadbeat loans. Basically, when an account is re-aged, it is no longer considered to be past due.

In the first quarter of 2016, Conn’s “re-aged” $21 million worth of loans—from $41.93 million to $62.29 million.

Accounting Trick #2: No-Interest Option Receivables. A typical loan payment is part principal and part interest, just like a home mortgage. However, when a struggling customer can’t afford to make the full payment, a loan company may let the customer get by just paying the interest on the loan.

But when a customer is really in trouble, a loan company could temporarily waive both principal and interest payments. In short… pay nothing!

Why would a loan company do this? Because it keeps the loan from being reclassified as a bad debt, which makes the loan portfolio look better than it really is.

In the first quarter of 2016, the percentage of Conn’s loans converted to no-interest loans rose from 32.8% to 37.1%.

Okay, here is what really counts: Nearly 80% of Conn’s sales are financed through its own in-house credit business.

My expectation was for one of two things to happen… and both of them were very bad:

Bad (but Fast) Outcome #1: Conn’s would tighten up its credit practices and extend much less credit. In that case, the 80% of its customers that couldn’t pay cash simply wouldn’t buy. Revenues would collapse, and Conn’s would report massive losses.

Bad (but Slow) Outcome #2: Conn’s would continue to make loans to anybody that could fog a mirror, and its credit losses from bad loans would skyrocket. Revenues would continue to show modest growth, but Conn’s would report massive losses from massive defaults.

Conn’s sort of let the cat out of the bag when it told Wall Street to tone down its full-year expectations. The company now expects revenues to grow by mid- to high single digits, well below Wall Street’s insane expectations for 13% sales growth, but I thought even that was too high.

Conn’s closed at $10.48 the day I sent out my trading alert, but its stock dropped like a rock on June 2, 2016, when it reported a much-bigger-than-expected loss of $0.31 per share—which shocked the Wall Street crowd that was expecting only a $0.06 profit!

The problem (no surprise) was that the number of deadbeat loans had increased and generated a $21 million operating loss, which pushed the bad-debt ratio from 14.25% to 15.25%.

That’s a huge number of deadbeat loans, which is why CEO Norm Miller said that Conn’s would have to make a commitment to “increased investment in credit risk management.”

Conn’s expects the rest of the year to get even worse. It lowered its mid-to-single-digit revenue growth forecast to low to mid-single digits.

And just for good measure, Conn’s fired its CFO and brought in a fresh face to tackle its financial woes.

Conn’s shares plummeted on that news, and we closed out the Conn’s short sale with a 21% profit, which is pretty darn good considering that the stock market had done nothing but pretty much go straight up during this time (April 7 to June 2).

That’s a fat gain, but short selling can be even more lucrative when the next bear market comes around.

My goal of showing you the anatomy of the Conn’s short sale is not to pat myself on the back, but to show you the process of identifying stock market dogs and a way to make money from falling stock prices.

Short selling isn’t a complicated, esoteric practice reserved for hedge funds and institutional investors. It’s not only a valuable diversification tool that helps you make money, but a defensive bear market insurance policy. Give Rational Bear a risk-free 3-month try and see for yourself.

Tony Sagami

related: Short Selling: A Trader’s Guide

Understanding the New Competitive Landscape in a World of Significant Change.

Understanding the New Competitive Landscape in a World of Significant Change.

“Competition is on for discretionary dollars, as growth of real after-tax income of middle class Canadian families has stalled”

Mobile internet, combined with cloud technology, has enabled US mobile e-commerce (m-commerce) revenue to grow from $13.6B in 2011 to $155B in 2015, and is on track to grow at an annual rate of 28%. Amazon and Walmart now both offer free shipping and same day delivery in some cities. For businesses, Amazon Supply is quietly targeting the fragmented trillion-dollar US commercial and industrial B2B wholesale and distribution market.

Competition is also on for discretionary dollars, as growth of real after-tax income of middle class Canadian families has stalled, and grew by only 7% (0.2% per year) from 1976 to 2010. With globalization, capital has become more mobile, increasing income at the high end, driving the annual global demand for luxury goods to outstrip annual GDP growth by almost 50%.

Finally, technological substitution solutions are significantly disrupting entrenched competitors. Think of what Lyft and Uber are doing for on-demand car service, Google is doing for semi-autonomous vehicles, and Tesla doing to the traditional automotive sales, service and distribution value chain.

Your biggest competitor is not likely the traditional foe in your sector, but from e-commerce enabled global companies, competition for shrinking discretionary spending, technological substitution from new entrants, and existing players that are aggressively deploying technology to provide innovative low-cost and high-service solutions. Don’t be blindsided, be prepared.

Always operate from a strong base. Get your business fundamentals right, so you can grow from a strong base with a safety margin to withstand shocks. This includes scalable systems, access to capital, multi-channel business models, and solutions that serve an evolving market. Don’t leave anything to chance.

Plan to dominate, not just compete. Technology and globalization are massively expanding choice while lowering costs, so simply competing is no longer good enough. Intend to dominate your sector aggressively by building a strong market niche, selling globally, executing M&A options, innovating new product or service revenue streams, and owning the customer relationship.

Build a clear competitive advantage. Warren Buffet likes to buy companies that have a wide economic moat, i.e. a competitive advantage, such as low-cost production, brand name, or pricing power that enables a sustained market positon. Know your economic moat, and invest in it. If you don’t have one, figure it out quickly before your competition does.

Be fanatical about hiring service oriented staff. Hiring top talent is always a sure bet, however, opportunity is being created at the service-centric high end of the income scale, while Amazon is driving cost out of the low end. Make a service mindset a requirement for hiring all new staff. Cultivate a service culture at all levels.

Sell more, especially to your current customers. Make “More Sales” your mantra, and communicate its importance regularly. Ensure each employee knows and executes on his or her role in supporting sales. Start by selling more to existing customers, through new product and service offers, while constantly developing new markets that align with your unique value proposition. If you are the CEO, dedicate at least 50% of your time to new or existing customers.

Probe for flaws and then improve. Each day your competitors are planning to put you out of business, so you should think like them. Probe your systems for weaknesses and fix them immediately. For instance, failed employees are not failed people, but a failure in your leadership or system. Work on the business, as well as in the business, and embrace a continuous improvement philosophy.

While changes are shifting the competitive landscape dramatically, well-positioned, innovative and agile companies can leverage these changes to build a better company by being proactive, service oriented and innovative.

also from Eamon: 10 Easy Steps For More Cash Flow

During a phase of rapid growth, don’t focus on keeping a tightly knit workforce, rather focus on keeping a tightly knit mission to dominate the sector, and then align the workforce to that mission.

During a phase of rapid growth, don’t focus on keeping a tightly knit workforce, rather focus on keeping a tightly knit mission to dominate the sector, and then align the workforce to that mission.

To achieve this, do the following three things:

1/ Focus on a core competency

The mission to dominate a sector will ensure the company stays focused on market needs, pushing it to innovate new offers, develop new business models, and clearly define the core competency necessary to deliver ongoing value. A tightly knit workforce can then be built and focused upon this core competency (e.g. technology, design functions, engineering expertise).

2/ Make change the new normal

High growth companies are in a state of constant change. This state needs to be defined and communicated by the business leader as normal, healthy, and lower risk than the status quo. All sacred cows should be offered up for slaughter as necessary, so the cultural expectation becomes the willingness to change internally in order to dominate the space externally.

3/ Outsource heavily, hire selectively

Nothing will stall the high growth company faster than the combination of negative cash flow and job loss fear. Heavily outsource non-core functions, so you can move quickly, focus your limited resources on what you do best, while building and protecting your core workforce during periods of volatility. Hire only in functions that support your core competencies, and make the retention of your key employees a high priority.

By Eamonn Percy

Business Tip of The Week:

Never take your employees or the culture for granted. Make it a habit to connect with them, and communicate on a daily basis. This way, they will know you care. If they only hear from you when things are really good or really bad, it will undermine your integrity as a leader and erode their committment to the mission.

…also from Eamonn: 10 Easy Steps To More Cash Flow

Step 1. Know your numbers – The best business leaders are able to describe their business, market and future plans, numerically. Exceptional growth comes from the precise understanding of all aspects of your business, including key metrics (e.g. sales funnel health, CAGR, and gross margins) and the status of current resources such as cash. I am not suggesting you lack emotion or passion, but rather complement it with objectivity.

Step 1. Know your numbers – The best business leaders are able to describe their business, market and future plans, numerically. Exceptional growth comes from the precise understanding of all aspects of your business, including key metrics (e.g. sales funnel health, CAGR, and gross margins) and the status of current resources such as cash. I am not suggesting you lack emotion or passion, but rather complement it with objectivity.

Step 2. Embrace low-cash, growth strategies – Often a company in growth mode will get a rude awakening when the sales plan actually succeeds, only to discover cash consumption, for working capital, can vastly outstrip cash generation. One of the better problems to have, but don’t let it become fatal. Build low cash growth strategies upfront such as: non-core outsourcing, well negotiated deal terms, low cost technology platforms, and scalable, multi-channel business models

Step 3. Maintain control of your financial systems at all times – Build strong and robust financial systems lead by competent and trusted financial managers. Never, ever lose control of your financial systems. When in growth mode review your financial statements frequently (monthly) and cash position weekly. Audit your systems regularly and keep a constant lookout for incompetence, deception, and fraud. Leave nothing to chance here.

Step 4.Deeply understand your sources and uses of cash – If your understanding of accounting is weak, get up to speed fast. Learn how cash flows in your accounting system, and what drives cash generation and consumption. For instance, if revenue increases, but accounts payables or inventory increase to service that revenue, cash will initially be consumed, not produced. You run the business, not the accountants.

Step 5.Be fanatical about improving margins – Top line growth must be converted into cash through effective margin management. Know your margins to one decimal point, set targets for each product and sector, cull the lowest 10% margin customers per year, and constantly test and iterate your offers to improve future margins.

Step 6. Manage working capital well – Run an aggressive accounts receivables strategy (i.e. prepayment, large deposits, automated billing, and improved collections) and mitigate payables. Work strategically to reduce working capital through new business models, and outsourced fulfillment.

Step 7. Play cash offense by driving sales – Start by selling more of your current offers to existing customers, then new offers to current customers, and finally develop new offers to sell to everyone. Selling more to your existing base is one of the best ways to juice up cash flow, since it requires modest new investment and can be ramped up quickly.

Step 8.P lay cash defense through cost containment – Implement a system like Lean, which focuses on the functions that deliver value directly to the customer. Invest in those steps and massively reduce the non-value added activity and waste. Reduce discretionary spending by creating a culture of frugality and always ask, “How will the customer benefit from this expenditure?”

Step 9. Be ROI driven – Focus all your key investment and time in the areas that will give you the biggest cash return. This usually starts with more sales, so as CEO you should be spending 50% of your time on sales. Also invest in hiring employees that create value for the customer, restructuring processes to reduce cost or cycle time, and new capital projects that build future cash streams.

Step 10. Use cash to dominate your sector – Use your newly minted cash to dominate a sector, not just compete in it. Sectors with too much competition will drain cash resources. Do this by regularly reviewing your strategic growth options and ensuring cash is diverted to the most promising areas. Don’t get complacent by the status quo and invest strategically to dominate.

…be sure to read the Eamonn Percy’s How The Power of Compounding Can Make You Wealthy and Want To Get Rich? Go Where The Money Is

also:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair