Real Estate

An apartment already rented long term for $525 a month with a purchase price of only $31,900! Now that is a hot property, the cash return is huge. Imagine if you finance it. That is not all from Ozzie Jurock either, he wraps up this segment with Michael Campbell with another Hot Property below:

An apartment already rented long term for $525 a month with a purchase price of only $31,900! Now that is a hot property, the cash return is huge. Imagine if you finance it. That is not all from Ozzie Jurock either, he wraps up this segment with Michael Campbell with another Hot Property below:

{mp3}grant/041616oj{/mp3}

Systemic Risk is Rising Quickly…

The Federal Debt:

The current amount The U.S. Government owes is over $19 trillion and therefore it is mathematically impossible to pay back. They will never be able to pay this back. Central bankers are in uncharted waters. They do not know how to create economic growth and fight deflation in some areas of the market. They do not know how to even return to a time of “normal” monetary policy. Their pretense of knowledge, of being able to effectively control currencies used by billions of people, is coming to an end.

The amount of debt only continues to grow and people think that somehow, governments are beyond the laws of mathematics. Things are fine until they are not. This is not an issue that will just go away or disappear, but rather continue to build until it reaches a breaking point.

Labor Force Participation:

We have close to 10’s of millions of Americans that are flat out not part of the labor force (not including children). The argument that this is only being made up of recent retirees is not true. First, many cannot retire because they need to work until they die. Another point is the rate is going up much faster than the number of people hitting old age.

Homeownership:

The homeownership rate has fully collapsed. Since the Great Recession hit, a large part of buying came from Wall Street and institutional investors. They bought homes to convert into rentals since this was how they used their bailout savior money. The money kept them afloat and what do they do? Buy up homes in a tight market and drive prices higher when working Americans already have declining incomes. The net result is that fewer people/families own their property and owning your home has always been traditionally viewed as the American dream. This has been the one vehicle where most Americans build wealth and equity and it’s not happening at nearly the same rate as it one was.

The problem is that people do not have $20,000 or $30,000 to make a down payment. I see a smaller number of Americans making their home the ultimate financial goal which is a good thing. It forces saving via having equity in their home. Let’s face it, you don’t hear all the retired and wealthy people saying they made their big money in a retirement account. In almost every case they earned their wealth through real estate investments in their own home and/or rental properties over time.

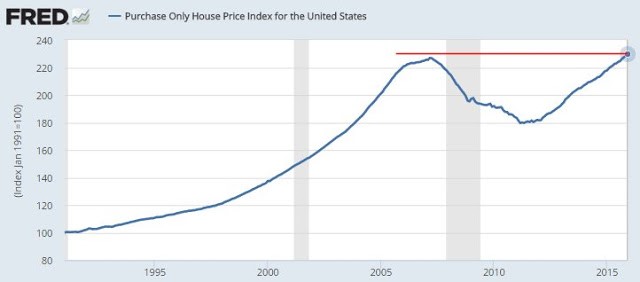

There are currently signs of another new housing bubble emerging. The current home price data shows that across the country we have now surpassed the last bubble peak. Incomes are not keeping up with wild movements in home prices. The end result is that the work force incomes are decreasing so creative financing is necessary to buy more expensive homes.

Homes homeownership rate has collapsed because of the higher priced housing market. How can prices go up with fewer families buying homes? Easy, since the bailout funds allowed banks, hedge funds, and investors to pick up foreclosed homes from families and then turned them into rental income properties. Today, we have many more people living in rental apartment and rental homes accumulating no equity and barely scraping by. Yet somehow housing prices soaring, college tuition at crazy levels, all while we have lower incomes. The current model of the American Dream involves no homeownership for the already shrinking middle class.

The upper-income, educated, married with children class are still not buying!

A strong middle class has been at the core of what has been promoted as the American Dream. How would America look like if the middle class simply vanished? We may not need to wait too long at the current rate since we are quickly siphoning people off the middle class and throwing them into lower Income brackets. The vast majority of Americans do not buy into the propaganda promoted on the mainstream media.

Housing prices have now reached an all-time peak. This is worth noting because the last peak was clearly at a point where we were massively overpriced, as seen in the chart below, and the entire world economy came close to experiencing the next Great Depression. There is nothing remotely “normal” about the current housing bubble’s rise and we can anticipate that its deflation could be equally abnormal and abrupt if the financial markets start to implode.

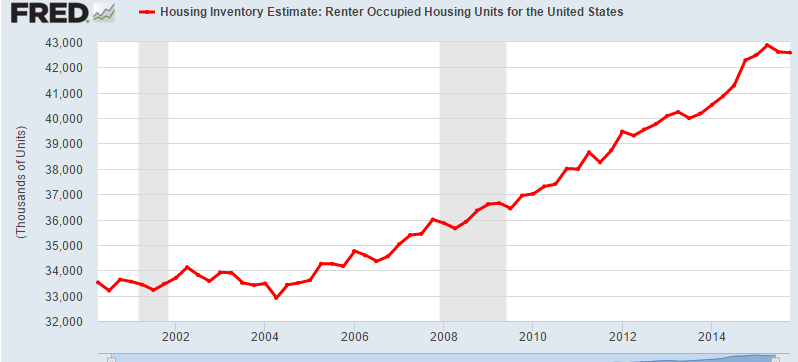

Homes were being bought by large investors to convert into rentals because money is almost FREE with rates so low, and the return on capital with rental properties is more than you will get anywhere else, plus you have a real asset, not paper money. This is where the bulk of the price increase occurred. This is why while net household’s information for owners is neutral, the country added 10,000,000 more reenter since 2004:

In short, real estate continues to provide the best return on investment.

Chris Vermeulen

related:

Negative Rates Could Trigger Another Housing Bubble

I recently purchased a large property, demolished the house, and am in the process of building a multi-family high-end retirement four-plex. I believe my area which is the www.CollingwoodRealEstate.net market will generate the best return on investment (cost of one property paying 4 rental income).

With low-interest rate it can make a business venture like this very profitable and is a solid long term strategy. The key with real estate though is to not get over extended with borrowed money. Own properties well within your financing capabilities factoring some worst case scenarios.

Eventually, certain areas of the financial system will crumble while others become favorable from stocks, bonds, currencies, to real estate. Each of these provide great opportunities to profit from through various investment vehicles like Exchange Traded Funds.

Follow my lead as I navigate the financial market and profit using ETF’s at TheGoldAndOilGuy newsletter.

“From top to bottom of the ladder, greed is aroused without knowing where to find ultimate foothold. Nothing can calm it, since its goal is far beyond all it can attain. Reality seems valueless by comparison with the dreams of fevered imaginations; reality is therefore abandoned.” ~ Emile Durkheim

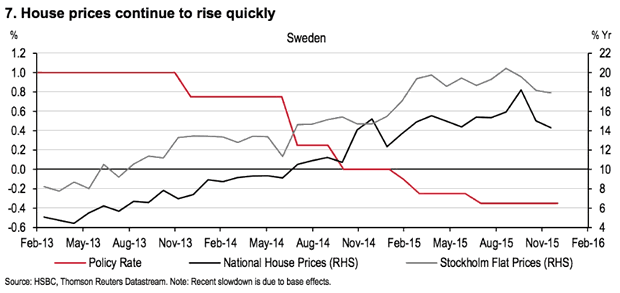

Sweden is already in the mature stages of experiencing a housing crisis. Take a look at the chart below. Home prices are surging simply because it is cheap to borrow money. The lower the interest payments, the more you can borrow. Hence, individuals throw caution to the wind and start chasing property because they believe prices will continue trending upwards. What they forget is that no market can trend upward forever.

More and more nations are embracing negative rates so as rates move into negative territory it will have the unintended consequence of fuelling another housing bubble, and suddenly property that appeared to be out of reach could be within reach, only because the monthly payment seems affordable. Eventually, the U.S is going to lower lending standards and when they do, expect the housing market to explode as there is a lot of pent-up demand. The public has been shut out of the markets for a long time, and when you give someone freedom after locking them up for a lengthy period, they go insane, and that is what lies in store for the housing market. The Fed has laid the path out, and this was planned years in advance. Take a look at the Swedish housing market as depicted in the chart below. The Chart for the US and UK housing markets will look 5 to 10 times worse.

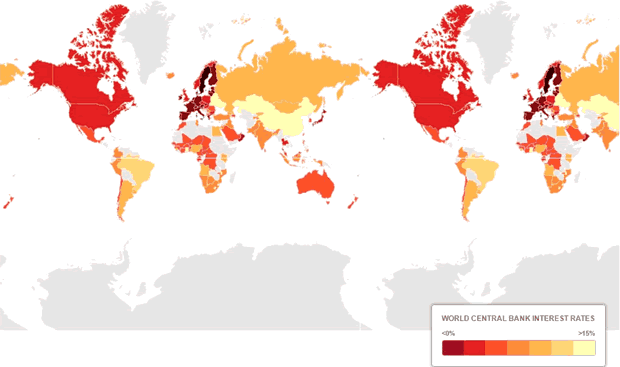

The map below illustrates that the war on interest rate is gathering momentum

Source: The Telegraph

Additional dangers of negative rates

As more nations embrace the era of negative rates, no nation is going will be in a position to resist. The slogan will be “surrender or die” and nations will opt for surrender as no one wants to die. Negative rates will also fuel a massive new round of share buybacks. The Fed is trying to put on a brave act, but you can already see them backtracking from the strong stance they took last year. Now they are stating that all is not well, and the economic outlook is weaker than expected. They will have no option but to join the rat pack; in this instance, resistance is futile.

The corporate world has gone a massive share buyback binge, and this binge is not showing any signs of letting up. It allows corporations to borrow money for next to nothing and then use these funds to buy back massive amounts of shares and in doing boost the EPS (Earnings per share). Negative rates will provide rocket fuel to the share buyback programs. Corporate debt will soar to insane levels; if you think today’s levels are insane, you are in for a rude awakening as debt levels will soar beyond anyone’s imagination.

This video illustrates property prices surged an average of 50% in the past ten years; this how bubbles start

Suggested Plan of Attack

We live in a world of extreme greed, and our government seems to favour corporation fraud; against this backdrop, you need to do that which seems insane from a logical point of view. All strong Market corrections should be viewed as buying opportunities. From a mass psychology perspective, this is still the most hated bull market in history and until the masses embrace, it is destined to run a lot higher than most envision.

Additionally, it would be advisable to hold a core position in Gold; at some point in time Gold will start to react strongly to this massive form of currency debasement. Currencies are being destroyed on a global basis at a level never seen before. This will not end well, but as we have pointed out many times before, being right does not equate to market success. One has to look at the time factor, and most individuals do not have the staying power to bet against the Fed. Wall Street is full of tombstones of good men who were right but could not stay solvent long enough to benefit from their insights. Hence, we would not bet the house on Gold and nor should you. No matter how good an investment appears to be, one should never put all of one’s eggs in one basket

“Avarice is the sphincter of the heart.” ~ Matthew Green

In March 2016, average Vancouver housing prices hit another record scorching hat trick on a sales breakout and listings dearth. Buyer mania continues to bid up anything that poses as shelter as it rides the 39 month momentum wave of single family dwelling prices that have been increasing at a 1.3% clip per month.

In March 2016 total residential sales in Calgary continued up on seasonality after hitting a new low this past January in this data-set. Bulls are still juggling with knives… er, I mean bids in all three housing sectors as listings and sales climb out of the seasonal lows.

If your portfolio lacks yield and you’re ready to do something about it, then you’ve come to the right place. I’ve scoured the real estate investment trust (REIT) industry and selected three high-quality stocks with yields of 3-8%, so let’s take a quick look at each to determine which would fit best in your portfolio.

If your portfolio lacks yield and you’re ready to do something about it, then you’ve come to the right place. I’ve scoured the real estate investment trust (REIT) industry and selected three high-quality stocks with yields of 3-8%, so let’s take a quick look at each to determine which would fit best in your portfolio.

1. InnVest Reit Trust Units

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair