Personal Finance

Diversification is generally considered one of the basic tenets of investing and financial planning. Owning a mix of assets, ideally with a low correlation – including, stocks, bonds, real estate and gold, for example – is Investing 101.

Diversification is generally considered one of the basic tenets of investing and financial planning. Owning a mix of assets, ideally with a low correlation – including, stocks, bonds, real estate and gold, for example – is Investing 101.

That is… unless you’re one of the world’s most famous investors.

I recently sat down with Jim Rogers and asked for his thoughts on global markets, what he’s buying now, where bubbles might be forming and… asset allocation.

Jim doesn’t buy into the cult of asset allocation.

“Well, I know that people are taught to diversify. But diversification is just that’s something that brokers came up with, so they don’t get sued,” Jim told me. Then he added, “If you want to get rich… You have to concentrate and focus.”

This obviously goes against conventional thinking. But this kind of thinking is what made Jim one of the world’s most successful investors. He co-founded the Quantum Fund – one of the world’s most successful hedge funds – which saw returns of 4200 percent in ten years.

He quit full-time investing in 1980 and went on to travel the world a few times. He also wrote several books about what he saw and learned. Even if you’re not a travel or money junkie and know little about finance, these are some of the most educational and entertaining books you’ll ever read about investing.

…also from Martin Armstrong: The War on Cash – One Giant Leap Forward For Government

When you think of the top 1 percent of all income earners in American households, how much do you think this group rakes in? Millions? Tens of millions? What about the top 10 percent?

On the contrary, to be considered in the top 1 percent of taxpayers US nationally, you’d need an annual income of $480,930. The top 10 percent of taxpayers make at least $138,031. These figures are based on 2015 income tax data, the most recent year available.

This income level varies widely by both state and city. In San Jose, California, the top 1 percent income threshold is close to $1.2 million, almost double the level for Los Angeles. As seen in the chart below, the spread is fairly wide between the top 10 most populous cities in the U.S. In San Antonio, Texas – home to U.S. Global Investors – you’d need to make $416,614 annually to be considered in the top 1 percent, slightly below the national threshold of top 1 percenters.

Earning enough income to be in the top 1, 10 or even 20 percent is no small accomplishment, but chances are good that many people you know, and may not think of as wealthy, fall into the top 1, 10 or 20 percent.

Is the Top 1 Percent Paying Their Fair Share?

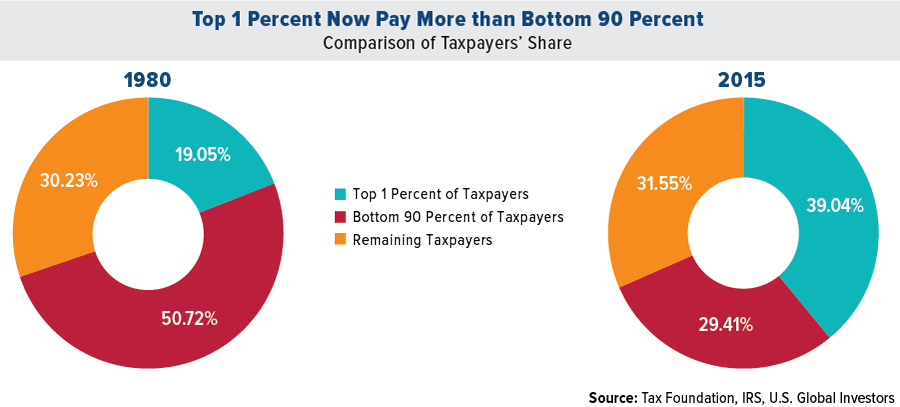

Contrast the above income statistics with the picture often painted in the media that the wealthiest Americans aren’t paying their fair share. According to the Tax Foundation, the top 1 percent of households collectively pay more in taxes than all of the tax-paying households in the bottom 90 percent.

Take a look at how much this has changed over the past few decades. In 1980, the bottom 90 percent of taxpayers paid about half of the taxes. The top 1 percent contributed about 20 percent.

Now, the top 1 percent pays more than the bottom 90 percent. Perhaps this is more than their fair share?

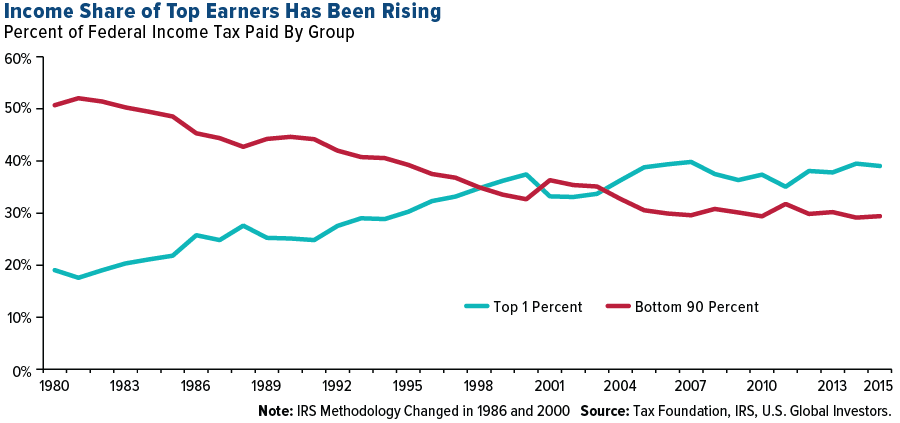

Below is the line chart from the Tax Foundation showing how the income tax share for each category has changed since 1980. For the majority of years, the share of the bottom 90 percent fell while the share of the top 1 percent rose.

Individual Tax Rate Cuts Take Effect in 2018

Taxpayers in the highest bracket should see a noticeable change when filing for the 2018 tax year since the top rate fell from 39.6 percent to 37 percent. President Donald Trump’s administration passed the Tax Cuts and Jobs Act in late 2017, which included small reductions to income tax rates for most individual brackets plus changes to exemptions, deductions and more. The average top 1 percent taxpayer will get a tax break of over $50,000 in 2019, according to estimates.

The new tax bill, however, eliminates the ability of taxpayers to deduct more than $10,000 in state and local taxes from their federal tax returns. This could significantly increase the tax burden of top earners who itemize their deductions in high-income tax states such as California and New York. One possible solution for these investors could be to take advantage of municipal bonds, which are often exempt from local, state and federal taxes.

Maximize Tax-Advantaged Investment Vehicles

Although it can be discouraging to see how top earners pay the majority of income taxes, there are still tax advantages for hard-working Americans who make saving and investing a priority in their lives.

How can you help make sure less of your money is going to the government and more of it is working for you in your investments? One way is to maximize your contributions to tax-advantaged investment vehicles such as an individual retirement plan, a 401(k), individual retirement account (IRA) or simplified employee pension (SEP) for the self-employed, all of which offer tremendous tax benefits.

To make it easier to have the discipline to set money aside, try an automatic plan that invests a fixed amount at regular intervals, such as the U.S. Global Investors’ ABC Investment Plan.

Wealth Isn’t Just a Number

No matter how much you earn, wealth is determined by how much you keep. My friend, Alexander Green, chief investment strategist of the Oxford Club, is a great source of inspiration for me and for many investors with his uplifting, holistic articles that relate to both health and wealth. Alex says wealth isn’t necessarily determined by an income figure. Instead, real wealth is determined by looking at your balance sheet. Here’s his formula:

“Maximize your income (by upgrading your education or job skills). Minimize your outgo (by living beneath your means). Religiously save the difference. (Easier said than done.) And follow proven investment principles.”

What matters most is being grateful for what you have. I’m a big believer that wealth is not a number or an amount, it’s an attitude and the umbilical cord to attitude is gratitude.

Take a look at my 10 favorite wealth and prosperity affirmations in this slideshow!

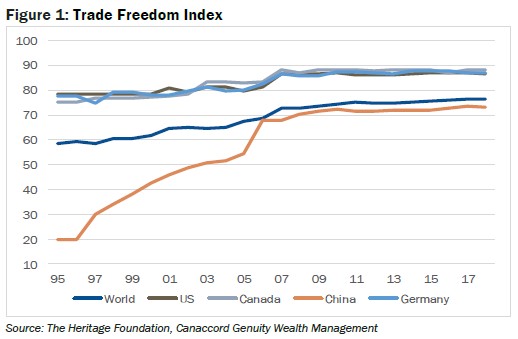

Trade freedom has been dominating the headlines and adding to the growing economic risks and market volatility. Trump’s tariffs on steel and aluminium imports have prompted fears of a trade war, albeit with a low probability and with some comfort offered with the exemption clauses. This does, however, remind us that negotiating with the US is difficult and that NAFTA negotiations have yet to be resolved. A more important and difficult issue is that of intellectual property rights in relation to China. For now, markets seem to be looking through the bravado because it is mutually beneficial for all sides to avoid a trade war which would negatively impact global economic growth prospects. This week we quantify trade freedoms to validate that seemingly prosaic position.

Using data from The Heritage Foundation, we see there have been notable reductions in trade barriers across the world over the past twenty or so years. Figure 1 highlights the Trade Freedom Index – for the world and four major economies. The Index is a composite measure of the absence of tariff and non-tariff barriers that affect imports and exports of goods and services. Trade freedom for the world has improved from under 60 per cent in 1995 to just under 80 per cent in 2018. The US along with Canada and Germany are close to 90% on the trade freedom score. In the case of China, there has been significant improvement from 20 per cent in 1995 to over 70 per cent in the latest measure. The rhetoric really does seem to be misplaced.

If Trump wants to bash China, maybe he should be focusing on investment freedoms (constraints on the flow of investment capital, and financial freedom which is a measure of banking efficiency and independence from government control). Measures that track investment freedoms have deteriorated over the past twenty years. We suspect that common sense will eventually prevail and that the market is correct to heavily discount the prospect of a trade war and focus instead on the improving fundamentals.

The US economy created 313,000 new jobs in February which was the biggest gain since mid-2016 according to the non-farm payrolls, a key leading indicator of economic activity. Jobs created in January and December were revised up to 239,000 and 175,000 respectively. The unemployment rate was unchanged at 4.1% last month. Average hourly earnings, which had spooked market fear of heightened inflationary pressures, rose by just 2.6 per cent year-on-year in February down from 2.8 per cent in January (which in turn was revised down from 2.9%). The inflation scare seems to have passed, but growth remains buoyant with the University of Michigan Consumer Sentiment Indicator coming in strong and with the economy projected to grow by some 2.8% annualised in Q1 2018 from 2.6% in Q4 2017 according to the Atlanta Federal Reserve GDPNow model.

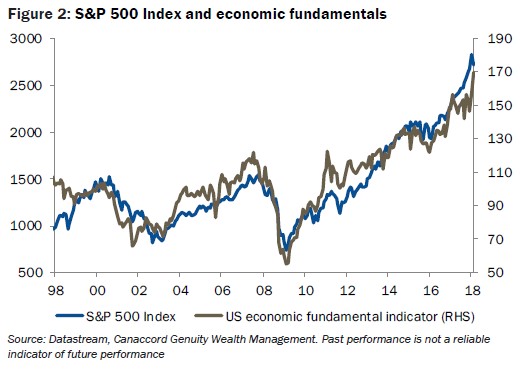

The economic fundamentals are important and we validate that in Figure 2 which highlights the close relationship between the S&P 5000 Index performance versus an economic composite indicator since 1998. The economic composite indicator is a blend of the Michigan Consumer Sentiment Index, the initial jobless claims and the CRB Spot Index. As George Michael might have said, “I think there’s something you should know…”, we should be focussing on the fundamentals and discounting the rhetoric for now.

Brent Woyat, CIM, CMT

Investment Advisor, Portfolio Manager

Canaccord Genuity Wealth Management

T: 604.699.0869 | F: 604.643.1802

All information is given as of the date appearing in this document and Canaccord Genuity Wealth Management (CGWM) does not assume any obligation to update it or to advise on further developments related. All this information has been compiled from sources believed to be reliable, but the accuracy and completeness of the information is not guaranteed, nor in providing it do CGWM assume any liability.

All views expressed in this document are provided for informational purposes only and does not constitute an offer or solicitation to buy or sell any securities. The statements expressed herein are not intended to provide tax, legal or financial advice, and under no circumstances should be construed as a solicitation to act as a securities broker or dealer in any jurisdiction. All views are intended for general circulation to clients and do not have any regard to the specific investment objectives, financial situation or general needs of any particular person.

Forward-looking statements and past performance are not guarantees of future results. To the fullest extent permitted by law, neither CGWM nor its affiliates or any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of the information contained in this document. Canaccord Genuity Wealth Management in Canada is a division of Canaccord Genuity Corp. Member – Canadian Investor Protection Fund and the Investment Industry Regulatory Organization of Canada

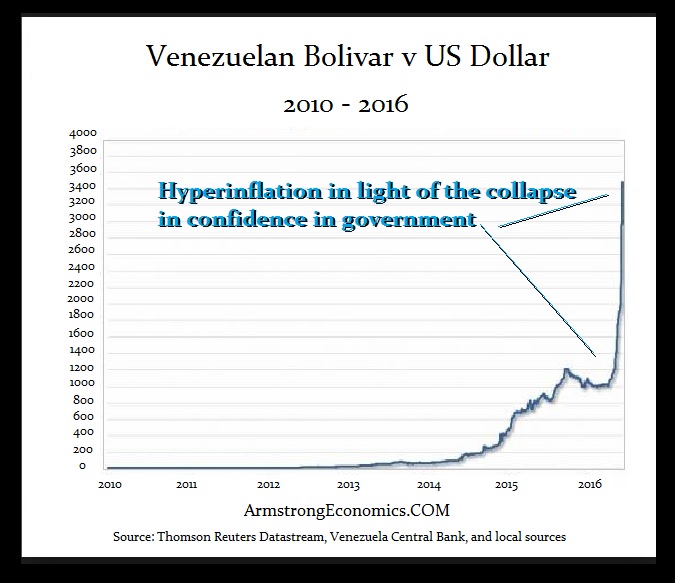

Martin Armstrong gives advice to a Venezuelan gentleman whose pension payout no longer can buy him a hamburger. A circumstance no longer an impossibility with the pension crisis unfolding as we speak in Canada & the US . Great advice for those expecting a pension – R. Zurrer for Moneytalks

COMMENT: Mr. Armstrong; I just wanted to comment that I am from Venezuela. My father came here to visit me in Florida where I live with a Green Card. Everything he saved in life for his retirement is now worthless and it does not even pay to travel back to collect his pension. The hyperinflation is a collapse in the confidence of government as you have explained. Those who saved for their retirement and had pensions, lose everything. They will be paid the amount that they were promised, but it will not even buy a single night’s dinner and soon a beer.

Thank you for your contribution to society. I wish more people would listen to you. Experience is the root of knowledge. Opinion is the root of bias. You have proven that

JE

REPLY: To survive hyperinflation requires the holding oftangible assets and never cash or pensions. The way pensions can be devalued is through inflation over the course of time and circumstance. What I paid into Social Security will never come back to me in terms of real purchasing power and that is without hyperinflation. I have stated before, I met with the Treasury back during the Reagan Administration and said these insane levels of interest rates will triple the national debt in less than 10 years. They simply responded; Yes but we will be paying back with cheaper dollars.

All promises of government are simply eroded with inflation. That is why Southern Europe fell into such chaos. The currency doubled instead of declining when the joined the Euro. That is why Europe has been a failure under this political-economic philosophy. The Euro first crashed, and then doubled in value. Southern Europe was used to deflation always reducing their debts. Suddenly, their debts doubled. And people cannot figure out why the Euro is in such trouble?

I do like your saying though. It is spot on.

….also from Martin: When Timing is Everything – The Failed Graf Zeppelin Venture

QUESTION: You do not believe in wide diversification?

QUESTION: You do not believe in wide diversification?

ANSWER: No. Wide diversification is only required when the investor does not have a clue about what is going on in the markets. We have asset allocation models for Institutions who simply believe they must have some diversification. The main objective is to limit the areas they will take losses on because of diversification. Why buy government bonds when you know we are at a 5,000 low? I am sorry, but sometimes the allocation to a particular segment should be ZERO!

….also from Martin:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair