Timing & trends

U.S. stocks sold off late in the day to close at session lows on Wednesday as talks to avert a year-end fiscal crisis turned sour, even as investors still expect a deal.

The S&P 500 ended after a two-day rally that took the benchmark index to its highest close in two months. Defensive-oriented shares led the decliners, including health care and consumer staples.

Obama threatens veto

Boehner and Obama have each offered substantial concessions that have made a deal look within reach. Obama has agreed to cuts in benefits for seniors, while Boehner has conceded to Obama’s demand that taxes rise for the richest Americans.

However, the climate of goodwill has evaporated since Republicans announced plans on Tuesday to put an alternative tax plan to a vote in the House this week that would largely disregard the progress made so far in negotiations.

On Wednesday, Obama threatened to veto the Republican measure, known as “Plan B,” if Congress approved it.

Jobs, the Fed… and Silver

…some picks from this mornings 5 Minute Forecast

![]() We interrupt the Santa Claus rally in the stock market with this foreboding announcement: The businesses responsible for nearly all “job creation” in the U.S. economy are pulling in the reins.

We interrupt the Santa Claus rally in the stock market with this foreboding announcement: The businesses responsible for nearly all “job creation” in the U.S. economy are pulling in the reins.

As the unemployment rate is key to several factors, not least of which are Fed policy and the long-term price of gold, today we take a closer look…

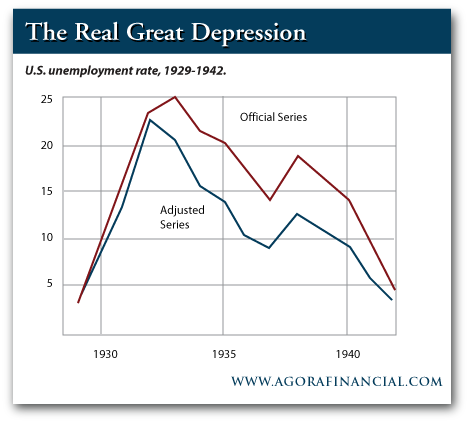

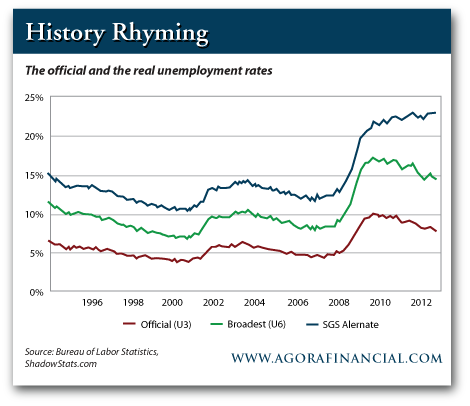

![]() Four years ago, the day before Election Day in 2008, we noted “the data point to watch [for whomever occupies the White House] will be unemployment. The real danger economically, socially or politically speaking in the ’30s was loads of young men without jobs.”

Four years ago, the day before Election Day in 2008, we noted “the data point to watch [for whomever occupies the White House] will be unemployment. The real danger economically, socially or politically speaking in the ’30s was loads of young men without jobs.”

Unemployment leapt up to 25% in a very short amount of time between the stock market bust in 1929 and 1934… the end of the official recession:

Now, five years after the start of the “official” 2007-09 recession, the real unemployment rate as charted by John Williams at Shadow Government Statistics remains stuck at 22.9%:

We might have been treated to a statistical reprieve during the campaign this year. We watched U-3 unemployment miraculously drop to 7.8%. But our forecast remains: As long as the quants can keep their grubby mitts off the figures, we expect unemployment to lurch its way back toward 10% before this time next year.

![]() Silver dropped to $31.18 yesterday, too. If you’re tracking the Midas metal’s less famous cousin, you can be forgiven for thinking it’s 2008 again — the price has been beaten down, but the actual metal is hard to come by.

Silver dropped to $31.18 yesterday, too. If you’re tracking the Midas metal’s less famous cousin, you can be forgiven for thinking it’s 2008 again — the price has been beaten down, but the actual metal is hard to come by.

The U.S. Mint has informed its network of dealers that inventory of 2012-dated Silver Eagles has been cleaned out… and the 2013 model won’t be available for order until Jan. 7. “This leaves a three-week void for the Mint’s most popular bullion offering,” Coin Update points out.

Silver Eagle sales to date this year total 33,742,500 — considerably less than last year’s record of nearly 40 million. Gold Eagle sales total 715,000 ounces so far in 2012 — the weakest pace since 2007.

[Ed. Note: Our friends at First Federal have already secured access to the coveted “first releases” portion of the Mint’s 2013 Silver Eagle issue. These beauties will be ready for shipment to your door as soon as they’re minted and certified MS70 by independent grading firm NGC. Get yours here.]

……..read more 5 Minute Forecast HERE

The one resounding thing that emerged from this world tour and holding conferences in US, Asia, and Europe, was that there is a universal rising tide that realizes something is seriously wrong. In having our computer forecast every market around the world, the benefit was that the analysis is the same, without emotion, and void of human opinion. You just cannot forecast anything any more in isolation. The year 2013 came up in just about every market from Asia to Europe as a profound turning point on a global scale. There is nothing that could cause such a unified correlation but the Sovereign Debt Crisis. Governments are desperate for cash and beware. Anyone who thinks buying gold is the answer, realize one thing. Sales are recorded so many ways so it would not be hard for government to figure out who has gold and who does not. It is not just so easy. They know everything about everyone. Privacy no longer exists.

The one resounding thing that emerged from this world tour and holding conferences in US, Asia, and Europe, was that there is a universal rising tide that realizes something is seriously wrong. In having our computer forecast every market around the world, the benefit was that the analysis is the same, without emotion, and void of human opinion. You just cannot forecast anything any more in isolation. The year 2013 came up in just about every market from Asia to Europe as a profound turning point on a global scale. There is nothing that could cause such a unified correlation but the Sovereign Debt Crisis. Governments are desperate for cash and beware. Anyone who thinks buying gold is the answer, realize one thing. Sales are recorded so many ways so it would not be hard for government to figure out who has gold and who does not. It is not just so easy. They know everything about everyone. Privacy no longer exists.

Governments everywhere are desperate for cash. The German socialists have blocked a tax deal with Switzerland because they want to know who has accounts there. It is no longer good enough for Switzerland to collect the tax and hand it in bulk form while protecting the names of individuals that was has been their law created back in 1934 when Hitler demanded the same information and was hunting the assets of any German outside the country. We are following the same policies as Hitler invoked. Anyone with an account out the country is a criminal. This has become about retribution – not just money. The hatred is just oozing out of every socialistic crack.

German Senate blocks divisive Swiss tax deal

The US Presidential elections were the nastiest perhaps in history with Obama practically spitting at any household that earns $250,000 or more and Joe Biden calling these people the “Super Rich”. These are the same rantings of those who followed Lenin and Mao. It is all about retribution. They say whatever they need to say to win even if they do not believe the bullshit they are saying. But the problem emerging is they are stirring the masses who are devolving into class hatred that can only lead to class warfare. When you cut a tree, in which direction it falls depends on the angle of the cut. If you just cut it straight with no angle, then the decision may be just the wind. Life as we know it is being tested. Can we avoid the hatred and civil unrest that this bullshit is stirring up or must we sink into squallier?.

Because of the seriousness of what we face and the number of people asking for a conference not on trading, but just of surviving, we will try to arrange a conference in Philadelphia for the general public one day with a seat price of just $200 as a public service. Those interested should reserve a space so we can determine how big a room to provide. The date will be in March 2013.

Reserve your Space at: SovereignDebtCrisis@gmail.com

The Fed continues with its “QE forever” easing program. But something new has been added. The Fed now wants the unemployment rate to be at 6.5%, and they’ll keep rates around zero until that happens.

Bill Gross is founder and co-CEO of Giant PIMCO. Gross is a member of BARRON’S Roundtable and is highly respected on Wall Street. Gross is a bond-man, and I don’t ever remember him saying anything about gold.

Bill Gross says only gold and real assets will thrive in fiscal ‘ring of fire.’

By Claudia Assis – The latest round of quantitative easing made gold “even more attractive” and owning the metal should be considered as part of a diversified portfolio, analysts at bond giant Pacific Investment Management Co. said in a white paper posted Tuesday on the company’s website.

Pimco founder and co-chief investment officer Bill Gross, in his separate monthly investment outlook also posted Tuesday, said only gold and real assets would thrive in a “ring of fire” of U.S. fiscal problems.

Gold GG elicits black and white responses, the Pimco analysts said. Some investors “have a deep, almost religious conviction that gold is a useless, barbaric relic with no yield,” while others “love it” and see it as “the only asset that can offer protection from the coming financial catastrophe” always just around the corner, they said.

“Our views are more nuanced … Our bottom line: given current valuations and central bank policies, we see gold as a compelling inflation hedge and store of value that is potentially superior to fiat currencies,” the analysts said. “We believe investors should consider allocating gold and other precious metals to a diversified investment portfolio.”

Other investments, such as Treasury Inflation-Protected Securities, offer an inflation hedge. TIPS are also less volatile than gold. History shows, however, gold’s high correlation to inflation and gold’s unique supply-and-demand characteristics may lead to attractive valuations, the analysts said.

In his piece, Gross warned the U.S. would no longer be “the first destination of global capital” seeking safe returns if it doesn’t address its fiscal gap. The U.S. “will begin to resemble Greece before the turn of the next decade” if it continues to close its eyes to deficits, Gross said.

“Unless we begin to close this gap, then the inevitable result will be that our debt/GDP ratio will continue to rise, the Fed would print money to pay for the deficiency, inflation would follow and the dollar would inevitably decline. Bonds would be burned to a crisp and stocks would certainly be singed; only gold and real assets would thrive within the ‘ring of fire,’” Gross said.

A financial Armageddon is not around the corner, Gross said. “I don’t believe in the imminent demise of the U.S. economy and its financial markets. But I’m afraid for them,” he said. Gross runs the world’s biggest bond fund, Pimco Total Return Fund. The fund in August took in $1.3 billion in new cash, bumping total inflows for the year to $9.3 billion. -Claudia Assis

Below we see five years of gold. Big correction below 1800. If gold breaks out of this correction on the upside, we should see fireworks.

To subscribe to the 88 Yr Old Godfather of newsletter writers. Richard Russell’s Dow Theory Letters CLICK HERE.

About Richard Russell

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

It appears that a positive catalyst for higher uranium prices has unfolded as the citizens of Japan have voted to put the Liberal Democratic Party (LDP) back in power by a large margin. This is significant as the party has voiced support for a return to nuclear energy in the country (as well as aggressive monetary policies which should be positive for commodity demand).

Only two of the 50 reactors in Japan are currently operating, but given the high cost of importing fossil fuels (estimated to be ~ $100 million per day), once can see why a return to nuclear- generated electricity holds an appeal. Nuclear generation costs are largely sunk. Plants, though aging, have been built and the typically large up front capital expenditure for new technology and extensive regulatory delays are not a deterrent in Japan as they are elsewhere in the world.

Not So Fast!

To be clear, if and when a re-start of the Japanese reactors commences, it may take longer than many anticipate as each nuclear plant must be inspected and cleared to resume operations. Reportedly, the Japanese Nuclear Regulation Authority is actively inspecting six plants to determine if they were built on active fault lines. Additionally, there is still ardent opposition to restarting the nuclear power plants in Japan.

From a recent Bloomberg article:

“People who voted for the LDP are supporting their economic-stimulus measures, not nuclear power policy,” said Toshihiro Inoue, a member of the “Goodbye Nuclear: the Action of 10 Million” civil movement, whose online petition to stop atomic reactors in Japan has so far received about 8.2 million signatures.

The fact that there is still opposition to reactor restarts is something investors should not dismiss in formulating an opinion on investing in uranium. Could local opposition to nuclear energy be the “black swan” for the uranium business the same manner that local opposition continues to hamper Lynas in the rare earth business? While we think it is too early to know for sure, any balanced appraisal of uranium investing must consider this.

That said, we are of the belief that it’s not a matter of if but when and how many of Japan’s reactors are restarted. A country such as Japan that must generate such a large portion of its electricity via nuclear power cannot afford not to.

Two other issues with the nuclear industry circle in our minds. We are concerned that the continual “refit” of old technology is one of the most dangerous issues. This is the current case in Japan as well as the U.S. It is, of course, prohibitively capital intensive to build new large scale reactors. Modular, lower cost reactor technology in the field still seems a few years away. Second, storage of spent uranium byproducts is still a problem without a solution. Would a transition in Japan (and elsewhere) to a thorium fuel cycle make more sense?

However Other Uranium Catalysts Are Lining Up

In a recent presentation at the San Francisco Hard Assets Conference I made the case for higher uranium prices in 2013 based on a looming supply and demand imbalance comprised of:

1. The “producers” are headed to the sidelines. These include BHP Billiton, Areva, Paladin, and Cameco who are either delaying or mothballing projects due to a low U3O8 price rendering projects uneconomic.

This trend collectively removes at least 20 million pounds of uranium from the market. A higher U3O8 price will, no doubt, bring many of these companies back into the market. However will they be able to do so in time to satisfy increased demand from countries such as China, India, the UK, the UAE, Slovakia, and Poland? There are ~ 436 nuclear reactors on line globally with 63 under construction and another 150 planned. The need for additional uranium to power the existing reactor fleet plus the additional reactors coming on-stream paints, we think, a particularly bullish picture for uranium exploration and production plays in 2013 and beyond.

2. The looming end of “Megatons to Megawatts” – the agreement between Russia and the United States to use uranium from Russian nuclear warheads a fuel in the 104 nuclear reactors in the United States. The agreement is set to expire at the end of 2013 and if it is not renewed, wholly or in part, could remove 24 million pounds of U3O8 from the market. This is 50% of USA consumption in a given year (a good sign for US-based uranium producers). While we cannot speculate as to whether or not the M-to-M Agreement will be renewed under different terms or at all, one must consider the possibility of a uranium supply disruption here.

3. As we mentioned above, Japanese reactors coming back on line will require additional uranium supply – reportedly 10% of global supply (approximately 15 million pounds). Again, when, not if this occurs, this will be bullish for uranium investors.

Uranium Is One of Our Top Picks For 2013

The uranium sector has been punished since the accident in Fukushima in 2011 and we submit that investing in junior miners involved in uranium is one of the great contrarian investment themes for 2013. A beaten down sector, unloved by the investing populace at large and shunned by major producers in the space is poised for a spike in demand. How that spike

in demand will be met is unclear. The low cost exploration and near term production stories would appear best positioned to deliver above average returns in the coming months.

Ideally, choosing a basket of stocks with different risk profiles would seem to offer the optimal risk-reward profile. We have written on and still like European Uranium Resources (EUU:TSX-V) as an early stage developer in Slovakia and also view favorably UR-Energy (URE:TSE) and Uranerz (URZ:NYSEAMEX ) for their low cost near term production profiles in the Western United States.

Source: u3o8.biz

As you can see above, despite the general downward trend in the U3O8 spot price, the election results in Japan have helped the price tick upwards. We think this could be the turning point in the sector many have been waiting for and reiterate our affinity for select uranium names in 2013.

Chris Berry of Discovery Investing

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. I own shares in EUU. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

Accordingly, one of the great questions on everyones mind is simply – what are the consequences going to be of Central Bankers being so involved in the marketplace?

Accordingly, one of the great questions on everyones mind is simply – what are the consequences going to be of Central Bankers being so involved in the marketplace?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair