Timing & trends

Produced by McIver Wealth Management Consulting Group

Mark Jasayko, CFA,MBA, Portfolio Manager with McIver Wealth Management of Richardson GMP in Vancouver.

A quick message from Michael Campbell

A quick message from Michael Campbell

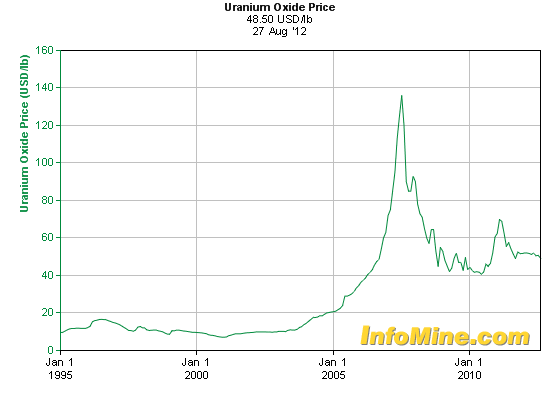

Currently at $44/lb – Ed

What’s the easiest way to track the ups and downs of energy markets? Watch what governments are doing rather than what they are saying, says S&A Resource Report Editor Matt Badiali. He has been watching behind-the-scenes nuclear energy importing in Germany and Japan and has concluded that the uranium market has hit bottom and is coming back up. What companies could benefit from these gyrations? He has an answer to that one in this Energy Report interview, plus some words of wisdom on U.S. oil and gas bottlenecks.

The Energy Report: In a recent piece for the S&A Resource Report titled “Government Lies and an Emerging Resource Opportunity,” you said that statements by German and Japanese officials that they plan to be nuclear free in the next two decades were a cover-up for what they’re really doing, which is importing nuclear power from other countries and secretly developing uranium supplies in former Soviet countries. How long can they hide these energy sources?

Matt Badiali: It’s not a case of hiding them. In both cases, the governments are playing politics. In Germany, the government was reacting to negative press and in Japan, which had just experienced a serious natural disaster. The Japanese government told people for decades that nothing of that sort could ever happen, that the nuclear reactors were completely impervious to natural disasters. That put them in a position where if they tried to make any improvements, they would lose face. They backed themselves into a corner and the only solution seemed to be to turn off the reactors. But the reality is that Japan needs nuclear energy. Without it, liquefied natural gas (LNG) imports have soared and the country doesn’t have the infrastructure to move it around. The result was a horrendous summer of spiking electricity prices and rolling brownouts; it was bad news.

Germany used the Fukushima disaster and the negative sentiment that followed to push through a carbon-free agenda. What is really ironic is that Germany is not in a place that gets earthquakes or tsunamis. It is not at any risk for that. It also isn’t a place where solar power works really well. Turning off the nuclear plants leaves the country without adequate energy generation infrastructure, so they increased imports of electricity from France. However, over 75% of France’s electricity is generated by nuclear power plants. So really all they did was outsource their nuclear reactors. At the same time, they brought on an enormous amount of coal power, which is the single-worst contributor of carbon dioxide. It was politics at its finest.

TER: Is the German press not reporting on this? Are people not wondering where their energy is coming from?

MB: I don’t read the German press, but what I do see is that the Germans are paying an enormous surcharge for a modest amount of carbon-free electricity. I don’t know why there has not been a massive backlash in Germany. If I lived there, I would be furious about the costs. In France, it costs about €0.14 per kilowatt hour (KWh) of electricity. In Italy it costs about €0.20/KWh. In Germany it costs €0.25/KWh. That’s an 85% increase in the cost of electricity. It’s really amazing, and I haven’t seen any pushback.

TER: Is the public as accepting of the higher prices and rolling brownouts in Japan?

MB: In Japan, we’ve seen a massive pushback. Shutting down nuclear reactors imposed an almost $56 billion ($56B) loss to the four major Japanese electric companies. That is not economically sustainable. You can’t bankrupt your power companies. On the supply side, think about Tokyo: It is an electric-centric life. Rolling brownouts and soaring power prices had an enormous impact on individuals. They reacted by electing a pro-nuclear government.

Even before that, the state-owned Japan Oil, Gas and Metals National Corp. (JOGMEC) was spending a significant amount of money exploring for uranium deposits in Uzbekistan. The government was saying one thing and doing another.

TER: After Shinzo Abe was elected prime minister at the end of December, the price of uranium bumped up. Was that just a coincidence? Is that a sustainable increase or just a temporary headline reaction?

MB: That was absolutely a market response to the idea that Japan is not shutting down nuclear reactors. It is also a reflection of the supply reality. Prices in the $40 per pound ($40/lb) range are significantly below production costs That led to many big projects being shut down, delay of BHP Billiton Ltd.’s (BHP:NYSE; BHPLF:OTCPK) Olympic Dam (Australia) project and AREVA’s (AREVA:EPA) Trekkopje (Namibia) and Imouraren (Niger) projects, to name a few. A total of 65 million pounds (65 Mlb) has come off of the market or will be delayed because the companies can’t justify the cost at these prices.

TER: How much of an impact could a loss of 65 Mlb in planned supply make on the price? Will we see $130/lb again?

MB: It’s not just supply loss in reaction to a real or perceived decrease in demand in Germany and Japan. We also have increasing demand from Russia, which has 33 operating reactors and 10 more under construction. Globally, another 65 reactors are under construction and 167 are in planning. Unfortunately, companies can’t just jump back in and turn on these new supplies of uranium.

The Olympic Dam expansion will take 3–5 years once the budget is approved. However, this is an 11-year, $20–33B project that requires some confidence that the price of uranium will be enough to pay for the investment. There is a lot of wiggle room for price increases. In the big picture for nuclear reactors, the price of fuel is a very small part of the operating cost. You can double the price of uranium with very little impact on a nuclear power plant’s bottom line.

TER: If uranium is ~$42/lb today, do you think it could be $84/lb in 2013?

MB: I have looked at the numbers for all the big public miners and the average cost to run the businesses is about $106/lb. So at $40/lb they are losing about $66 on every pound they sell. You can’t make that up without the price going up. So, yes, I think we are going to see the price come up. I absolutely think that we’ve seen the bottom. I think $80/lb is not unreasonable and $100+/lb is more likely.

TER: How much would the price have to go up in order to turn on some of those projects that have been put on hold, like Olympic Dam?

MB: I think it’s going to be more about sustainable prices. When you are spending billions of dollars, you really need to be making a good profit to pay those loans back. We have to see the prices go up and stay up and then three to five years later we could see production increase.

TER: If the supply and demand equation you’re outlining here comes about, what companies are poised to profit from that?

MB: We have actually already seen some. In my December 4 newsletter, I recommended Cameco Corp. (CCO:TSX; CCJ:NYSE), Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT) and Uranium One Inc. (UUU:TSX). Recently, Uranium One’s partner, the Russian state-owned nuclear power company, Rosatom Nuclear Energy State Corp. (ROSATOM), which owns 51% of Uranium One through a holding company called ARMZ, decided to take the whole thing off the board. That put investors up 46% in five weeks. We also saw earlier this week that Denison Mines has acquired Fission Energy Corp. (FIS:TSX.V; FSSIF:OTCQX), a junior exploration company with a nice discovery in the Athabasca Basin in Canada. It was the other half of Hathor’s Rough Rider, which was bought by Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) in 2011. We saw a nice premium for that takeout. I thought Denison did a good job acquiring Fission. The Athabasca Basin is basically Saudi Arabia for uranium. These are high-grade, high-quality uranium deposits in a very safe jurisdiction.

TER: Do you think there will be more M&A?

MB: I do because the companies see that we are coming off the bottom and in order to buy low, now is the time to do the acquisition.

TER: Who, in your view, are the likely acquirers and acquirees in 2013?

MB: I think Cameco will likely go shopping. Some of the Chinese companies have been aggressive over the last couple of years. I wouldn’t be surprised to see them get involved in this too. And Russia is clearly acquiring new assets and moving into new areas.

One promising exploration project that could get taken over is Uranium Energy Corp. (UEC:NYSE.MKT) in Texas, Amir Adnani’s company. It is an in situ leach mining company that is just starting production in the Texas uranium belt right now. The company injects water that is enriched with oxygen into a uranium-heavy sand body. As the water moves through this sand body, it dissolves the uranium. The liquid is pumped out on the other side of the sand body and the uranium is extracted. The company has been successful doing that and the low-impact method could be attractive to an acquirer.

TER: What other acquisition candidates are out there?

MB: UEX Corp. (UEX:TSX) has some projects partnered with AREVA doing exploration work so that is a potential acquirer.

TER: Do you like the project or the partnership?

MB: I like both. UEX has two good projects in the Athabasca Basin, Shea Creek and Hidden Bay. I’m interested in companies with assets in the Athabasca Basin.

However, I haven’t put UEX or Uranium Energy Corp. in any of my letters yet. I told my readers about the big, safe assets first and looking back, we did a pretty good job, timing wise. Now that we have established the trend, we will start to pick off the best of the exploration plays because I think that that’s a good place to make some money over the next year or two. I will definitely look at Athabasca Uranium Inc. (UAX:TSX.V; ATURF:OTCQX) and Energy Fuels Inc. (EFR:TSX). But I’m not going to overpay or rush into these because we are already making money on the producers.

One company I was concerned about was Paladin Energy Ltd. (PDN:TSX; PDN:ASX). I told my readers that they should be very careful. It has some great assets and a long-term supply contract with one of the French utilities, but it’s experienced some problems turning a profit. So going back to acquisitions, it might make sense for a big mining company to take over Paladin. It has a lot of debt. It’s a $712 million ($712M) market value with $830M in debt. In addition, the company has $125M of convertible bonds coming due in two months, which will lead to converting up to 147M shares. That’s a big dilution. This might be something for readers to look at down the road after these bonds convert. If the share price sinks below a significant point where the dilution’s not going to hurt quite as badly, that could be a possibility. It may be that Paladin is worth a flyer for its assets after the dilution happens.

TER: The other energy play you have written about is shale oil and how it could flood the market with cheap gas. You sold a number of your oil and gas positions over the summer. What is your oil and gas outlook for 2013?

MB: I’m staying out of North America; I really am. A number of problems are going on right now that make me bearish on these companies. There are so many bottlenecks involved in getting oil from the new shale plays to the refiners. You can’t get your oil out of the Bakken. Producers are getting paid a discount to West Texas Intermediate (WTI), which sells at a discount to Brent. Companies are drilling lots of wells and producing lots of oil but they are getting beaten up on price. Meanwhile, companies are paying a lot of money to ship on railcars. It is twice as expensive to put a barrel of oil on a railcar as it is to put it in a pipeline. I’m keeping my eye on a few places. I like some of the emerging shale plays like the Tuscaloosa marine shale. It’s brand new. I’m looking for small caps. But I haven’t made any investments in oil and gas yet. I’m just playing the field right now. I want companies that are exploring outside of North America that are getting paid on Brent prices. It is just easier for companies in Australia, New Zealand and Africa to make a profit because they can charge $20/barrel higher than companies stuck in the Bakken.

TER: What companies outside the U.S. do you like?

MB: One company that is trading at a premium now, but that I like very much is Africa Oil Corp. (AOI:TSX.V). I also like Lundin Petroleum Corp. (LUPE:OMX; LUP:TSX). I don’t have either one of those stocks recommended in my letters right now. Africa Oil was a great buy and then it just took off and I’m waiting for that one to come back to us. But I think Lundin’s a great one.

TER: Streetwise President Karen Roche recently interviewed Porter Stansberry and he’s pretty excited about the idea of American oil independence. Do you think that he’s more upbeat than you are on oil in the U.S.?

MB: He’s playing it a different way. Porter’s investments are different than mine. I’m strictly a resource stock investor. I don’t get into the infrastructure so much. Some of our other guys like Porter and Frank Curzio have both done very well. Frank did really well with an investment in Westport Innovations Inc. (WPT:TSX; WPRT:NASDAQ), a natural gas engine company. It converts long-haul trucks so they can run on natural gas engines. I am incredibly bullish on North American petroleum. I am a geologist; I have seen these oil kitchens first hand. The shales are where the oil resource formed before it migrated to the oil fields. Years ago, these were interesting but not really useful. You wanted to drill the sands that made up the oil fields. But now we can go back and actually drill the “kitchens,” these giant shale deposits. It’s an enormous, game changing thing.

Some of the largest shales in North America haven’t been tapped yet. The Monterey shale in California is going to blow people away. The Mancos shale in western Colorado has huge potential. The Tuscaloosa shale stretches from Louisiana to Florida. There are more in Texas. The question is whether people will take the time to understand the techniques that the industry uses to crack the rocks and make it happen, or will the emotional reactions take over and the energy, jobs and investment potential be left in the ground?

TER: So you’re bullish on the amount that’s there but not on the price that companies are going to get pulling it out?

MB: Exactly. We need to get out of our own way and build the pipelines to move enormous volumes of oil out of the middle of the country.

TER: Are you a fan of investing in the infrastructure plays such as MLPs, pipeline companies and service companies?

MB: There are definitely opportunities there. I like some of the midstream companies, but they fall outside of my bailiwick. Gathering the gas is a pretty good place to be because they are getting paid for the quantity they move and aren’t reliant on the price of the commodity itself.

TER: Any final advice for energy investors?

MB: I’m pretty excited about the developments that are going to happen, but you have to be careful.

TER: Thank you for your time.

MB: Thank you.

Matt Badiali is the editor of the S&A Research Report, a monthly investment advisory that focuses on natural resources, including silver, uranium, copper, natural gas, oil, water and gold. He is a regular contributor to Growth Stock Wire, a free pre-market briefing on the day’s most profitable trading opportunities. Badiali has experience as a hydrologist, geologist and consultant to the oil industry. He holds a master’s degree in geology from Florida Atlantic University.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

As GDP Drop Sees US Fed Press On with QE, Investors “In Great Danger” If They Don’t Own Gold Warns Faber

![]() The PRICE of GOLD held onto most of yesterday’s $15 jump at $1676 per ounce Thursday morning in London, ticking back as Asian and European stock markets fell after Wednesday’s surprise drop in US economic output figures.

The PRICE of GOLD held onto most of yesterday’s $15 jump at $1676 per ounce Thursday morning in London, ticking back as Asian and European stock markets fell after Wednesday’s surprise drop in US economic output figures.

Silver also eased back, but held at 1-week highs above $32 per ounce after rising yesterday in gold’s “slipstream” as one bullion-bank analyst put it.

“This Friday’s [non-farm US payroll] report remains crucial,” says a note from Swiss bank UBS – currently encouraging its institutional clients to buy gold outright rather than as a credit-risk deposit.

“Some adjustments to [gold] positioning are likely to emerge” after Wednesday’s ‘no change’ decision from the US Federal Reserve on zero interest rates and quantitative easing.

“But overall, the gold market should resume subdued trading,” says UBS, “as is typical ahead of a key event” such as the monthly jobs report.

Russia’s foreign ministry meantime condemned a reported Israeli air-strike on a military research unit inside Syria, saying Thursday that – if confirmed – this “unprovoked attack [would] blatantly violate the UN Charter.”

Shares in Italy’s struggling Banca Monte dei Paschi di Siena – founded in 1472 – steadied as the Italian central bank weighed MPS’s second bail-out request in four years after it hid losses of €500 million on a 2008 derivatives deal.

German banking giant Deutsche Bank lost €2.2bn ($3.0bn) for the last 3 months of 2012, it said today.

“A year ago, the mood in Europe was horrible and nobody could see how on earth stocks could go up,” says Gloom, Boom & Doom author and money-manager Marc Faber, who urged CNBC anchor Maria Bartiromo to buy gold earlier this week.

“Now since May 2012, less than a year ago, Portugal, Spain, Italy, France, are up between 30 and 40% and Greece has doubled…!”

Factory-gate prices across France and Italy fell in December from November, new data showed today.

House prices in the year to October fell 2.5% across the 17-nation Eurozone, with Spain’s home-price drop accelerating to 15.2%.

“For the first time in four years,” Faber continued Wednesday, pointing to the US stock market, “since the lows in March 2009, I love this market. Because the higher it goes the more likely we will have a nice crash, a big time crash.

“You are in great danger if you don’t own any gold,” Faber had earlier told Bartiromo.

Near-term, reckons Deutsche Bank analyst Xiao Fu – and despite Wednesday’s $15 rise on poor US growth data and the Federal Reserve’s no-change decision on zero rates and QE – “Gold lacks a convincing catalyst near term to take it convincingly higher and instead remains susceptible to opportunistic selling.”

But “Any thought given to reining in some of the Fed’s buying power will now be shelved,” counters Ed Meir in his daily note for INTL FCStone.

“[Wednesday’s] GDP number clearly shows that the US economy is still far from capable to muster its own momentum without key fiscal and monetary stimulus.

“In the least, this should provide an element of support to the precious metals group, at least over the short term.”

After creating and spending first $1.4 trillion on mortgage and Treasury bonds in 2008, and then a further $600 of T-bonds starting in 2010, the US Fed will likely acquire a further $1.1 trillion of US government debt with its current program of quantitative easing, according to a Bloomberg survey of analysts.

“Given the sluggish [US] economy,” says precious metals strategist Eugen Weinberg at Commerzbank, “it would be premature to discuss [the Fed] abandoning the quantitative easing programme.

“Despite the noticeably higher risk appetite displayed by market players of late, gold demand is thus unlikely to ebb away completely. On the contrary, high sales of US gold coins in January, and renewed inflows into the gold ETFs recently, point to relatively robust demand for gold.”

Over in India – most likely the world’s #2 gold consumer market in 2012 behind China – the economic affairs secretary contradicted the finance minister yesterday over plans to raise gold import duties again, in a bid to curb household appetite to buy gold, widely blamed for India’s yawning trade deficit.

Two days after Palaniappan Chidambaram told the Financial Times that New Delhi is considering “some other steps to moderate the import of gold” further, Arvind Mayaram told Reuters that “I don’t think there is any plan as of now.”

Adrian Ash

BullionVault

Adrian Ash is head of research at BullionVault, the secure, low-cost gold and silver market for private investors online, where you can buy gold and silver in Zurich, Switzerland for just 0.5% commission.

(c) BullionVault 2013

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair