Has Our Government Become Dysfunctional?

Has Our Government Become Dysfunctional?

This a.m. we comment on president Obama’s state of the union message from last evening. Perhaps the most obvious impact of the speech was the potential for further intrusion of government into our lives and the pledge that that intrusion would cost “not one dime.”

Any reasonable person will know that pledge cannot easily be fulfilled.

The top five elements of the speech according to this morning’s Wall Street Journal were:

- A Strong push for gun control.

- A call for smarter government that sets priorities.

- A climate change initiative he said he will do on his own if Congress doesn’t do it.

- A nonpartisan commission to improve the voting process.

- The President called on Congress to avoid to sequester said the devil is in the details and then failed to provide any (details) thus failing to advance the debate.

Completion of these five elements is highly suspect. Gun control, as proposed by Sen. Feinstein, cannot pass. Second, it is unlikely that the government bureaucracy is smarter than the individual nor can it increase its level of “intelligence” easily due to political dynamics. Third, there is significant evidence that climate change is not caused by humans and therefore cannot be changed by humans. Change to the voting process will be a strawman issue and difficult to achieve. And finally it’s beginning to appear likely that we shall have a Sequester as proposed over a year ago and extended in the recent fiscal cliff compromise.

Very clearly the president thinks he can roll the Republican House and he is indeed on a roll. To date he has had the upper hand in this regard.

Most important it is difficult to see how these top five issues can be accomplished in a “not one dime” fiscal scenario. We all know taxes must increase, but if these top five priorities are to be attained, government spending must increase. Thus far president Obama has proven very adept at assembling a power.

The assault on our lifestyle is well underway in Washington D.C. It is evident everywhere in every administration policy. It is evident to everyone. It is also evident that the Republican Party is badly split and may be unable to arrest the intrusion. While the president’s focus was on the middle class he continued to refer to “billionaires and high-powered accountants” again demonizing those in the country, many of whom have taken risks and created great wealth for hundreds of thousands of people.

This is a president that is expert in polarization of the electorate. He believes in assembling power by broadening the entitlement economy through wealth transfers. He also is convinced that government is smarter than the individual; that individual freedom must be constrained and be subservient to government fiat.

For example, last evening the president called for higher minimum wages ($9.00 an hour up from $7.25 a 24% increase) a sop to immigrants designed likely to accumulate their votes. Increased minimum wages will impact service industries and also, to a large extent, small businesses owners. So the assault is not just on ALL taxpayers. The assault is yet to be felt on business also in small business is critically important to the U.S. economy.

As we write this a.m., we admonish our readers to realize that revenues, known as taxes, must increase significantly. They must increase across the board. We do not doubt that. However taxing the rich only will not produce enough revenue to deal with the current deficit. So we shall all bear the economic problems (slower economic growth, stagnant real income, frustratingly high unemployment) arising from higher taxation. In itself this is a major issue fomenting austerity, what Bill Gross of PIMCO calls the “New Normal” American lifestyle.

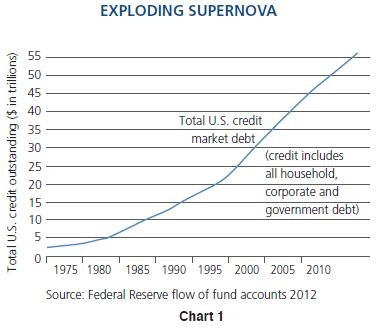

The U.S. economy is driven 70% by the consumer. It has morphed into that framework over the past 60 years, since 1952. American consumerism is a well-entrenched culture that has driven growth in the U.S. and the world. China relies on the U.S. consumer. Because the country that controls the Reserve Currency may borrow at will the U.S. government has continued to borrow to sustain the American lifestyle. The U.S. has continued to run increasingly large annual deficits to the extent that now our children and grandchildren are saddled with a huge debt that likely can never be repaid.

Last evening I was interviewed by The Gold Report. One of the many questions related to the moribund natural resource market. I told the interviewer my views. I believe that we are on a downward slope in terms of our quality of lifestyle. In truth this is necessary and unavoidable. It has impacted investment dramatically.

The programs emanating from this administration, the Congress, the inability of the Republican Party to mobilize and define itself appropriately and the apparent felicity of an electorate willing to believe in every gift they are to receive from a “lame duck” President indicate that a vast wealth transfer is underway and that the endgame must be a reorganization of the economy to accommodate our grandchildren’s unsolvable debt problem.

This view may seem extreme. But you must look at the facts and decide for yourselves. No government or central bank can electronically create $85 billion a month to support paper markets. In other words, you cannot support paper debts by printing paper. Interest rates must increase at some point in the future, perhaps the near future. At that time the Federal Reserve and the Treasury will no longer be able to control interest rates at zero.

This scenario will unfold, deflation a central banker’s real fear, notwithstanding. No one yet knows the outcome. Gary Shilling believes that deflation is inevitable and must last for years as it has in Japan. Others, such as Mr. James Sinclair, believe we must see hyperinflation in our economy as soon as this year. There is no reason we cannot see both in succession. History tells us it is happened in the past. In any case the American citizen, perhaps the citizen of the world, must realize a declining lifestyle.

For example, last evening the untouchable “Third Rails” were hardly mentioned. Very clearly there are serious sustainability problems with Social Security, Medicare and Medicaid. Very clearly, mom-and-pop now to must consider postponing retirement. Obviously such considerations add to the unemployed, unemployable and under employed strata of our society. 43 million people (13%) now rely on food stamps in the United States of America and yet the Administration tells us we are not spending enough on food stamps.

In the past four years the President has pandered to the student population (the young voting population) now a $1 trillion problem of bad student loans beginning, in size, to challenge the housing problems of 2008 at 2009.

Meanwhile the emerging world is awakening from hundreds of years of poverty and economic malaise. Digital technology has served as a “Professor to the World.” The rapid distribution of cell phone technology, iPads and iPods has created an awareness of the potential increase in quality of life that is possible and highly desired. This is no longer the Third World but now the Emerging and Powerful World. It is the emerging world, largely free of the debt accumulated in the West that will, in the next two decades, lead global economic growth.

Emerging world infrastructure buildout will swamp the size of the infrastructure creation in the United States between 1950 and 2000. All sorts of commodities and hard assets will be required in quantity. Food, fertilizer, potable water, lifestyle metals such as graphite, and monetary metals will be in demand.

These have not yet been discovered.

Because they will be in short supply many will become good discovery investments. You must discuss your investment plans with your financial planner. 0% interest rates creating financial repression for your portfolio must be countered. You should consider an allocation to hard assets and in my case Discovery Investing.

Discovery investing it is risky and not for the faint of heart. However it is a socially responsible investing discipline as we have defined it using our 10 factors to analyze companies. Great discoveries create jobs and increase lifestyle through education and infrastructure for individuals.

Last evening in The Gold Report interview I reviewed a number of discovery companies mostly from Nevada a mining friendly state in a relatively mining friendly jurisdiction that I am considering at this time. They include International Enexco (see Monday’s Morning Note), Pershing Gold, Valor Gold, Almaden, Terraco Gold, NuLegacy Gold, Quaterra’s Yerington copper district, Corvus Gold, Geologix, Grande Portage is Herbert Glacier project, Quaterra’s Nieves project in Mexico and Gold Standard Ventures.

Chris and I are performing due diligence on all these names and more so these are not yet recommendations on the weekend positive Pershing Gold, Terraco Gold and Quaterra’s Yerington recently. We own shares in Pershing Quaterra, Terraco currently.

Please consider some allocation to gold and silver as we believe these prices must increase due to the current mercantilism of fiat currencies in the world. Your allocation may be to the metal itself to ETF’s or to discovery stocks. Please consider lifestyle discovery investments. The food space fertilizer space water spaces present some very attractive investment opportunities at this time.

And so we move forward with tepidity into a new economic era. It will be the era of our grandchildren and their generations. Our investment strategies today must keep pace and adjust to this rapidly changing and new economic environment.

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. We own shares in International Enexco Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin. We own shares International Enexco, Quaterra Resoruces and Terraco Gold