Timing & trends

A shallow correction between now and the end of March will provide an opportunity to accumulate sectors on weakness that have a history of outperformance into spring. Sectors include energy, retail, steel and auto & auto parts.

North American equity markets continue to track their historic trends set in a U.S. Post Presidential Election year implying a correction that started in the second week in February followed by shallow weakness until the end of March followed by resumption of an intermediate

….read more and view 44 Charts & Sector analysis HERE

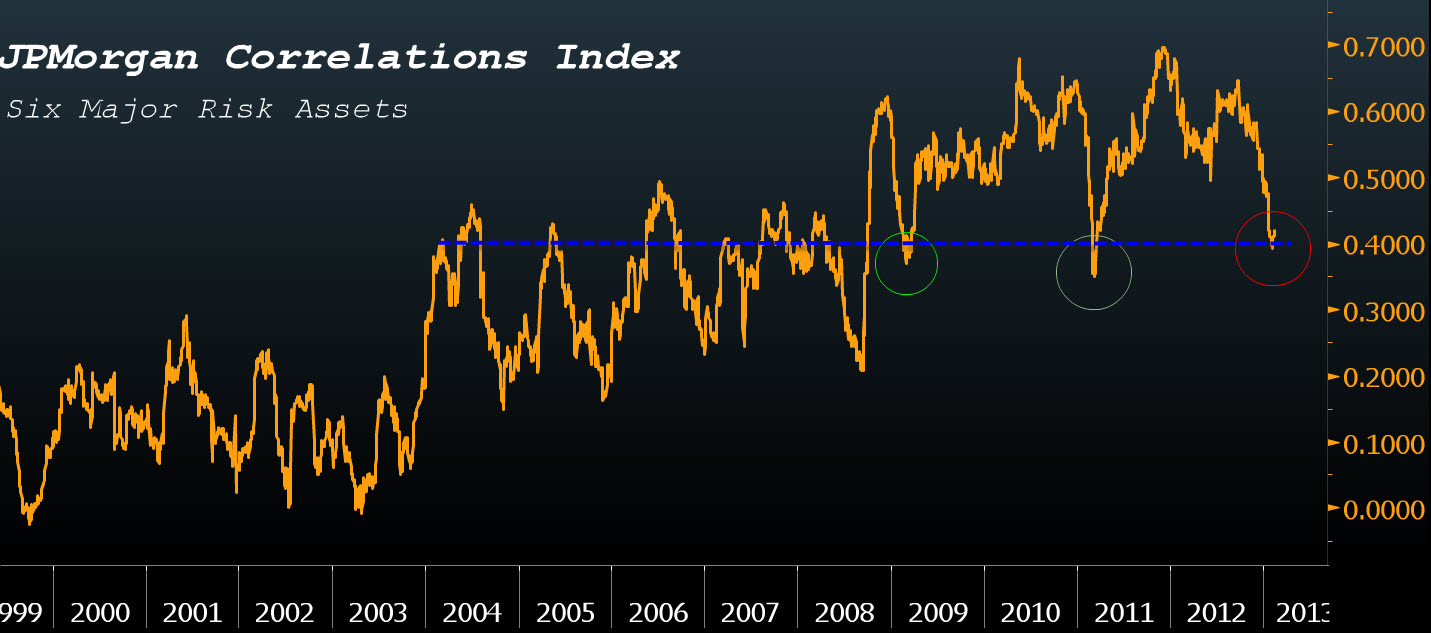

Simply put, this is a chart of the victory of central bank largesse over human common-sense and logic. We suspect – just as we have seen before – this cloak of invincibility will be lifted once again very soon.

…..read more HERE

Chart: Bloomberg

Registered retirement savings plans (RRSPs) are one of the most popular investment vehicles for Canadians. Contributing to an RRSP is one way to reduce the amount you owe at tax time.

Registered retirement savings plans (RRSPs) are one of the most popular investment vehicles for Canadians. Contributing to an RRSP is one way to reduce the amount you owe at tax time.

March 1, 2013, is the last day you can contribute to an RRSP for the 2012 tax year.

The amount you can contribute to your RRSPs each year without tax implications is determined by your RRSP deduction limit, or contribution room, which can be found on your 2011 notice of assessment.

The Tax-Free Savings Account (TFSA) allows Canadians, age 18 and over, to set money aside tax-free throughout their lifetime. Each calendar year, you can contribute up to the TFSA dollar limit for the year, plus any unused TFSA contribution room from the previous year, and the amount you withdrew the year before.

The annual TFSA dollar limit for 2013 is $5,500.

All income earned and withdrawals from a TFSA are generally tax-free. Plus, having a TFSA does not impact federal benefits and credits. It’s a great way to save for short and long-term goals.

Avoid the Annual Mistake!

Every year around this time, our phones begin to ring off the hook. With RRSP deadlines and new TFSA room, investors become fixated on the investment industry for a few months. This is a mistake.

Don’t get me wrong. It’s great to be in demand and busy. And for the average investor, we are pleased with the level of engagement we see at this time of year. But the mistake is trying to cram a year or more worth of investment decisions into a week or even a day around RRSP/TFSA season.

Contributions are made and securities are purchased all within a rushed day or so. Then the investor exhales and goes back to the regular routine with the occasional gander at the portfolio through the remainder of the year. Use this strategy at your peril!

By all means, make the appropriate contributions to your RRSP if its suits your investment situation. We are big supporters of TFSAs and encourage investors to pair a self-directed TFSA with our annual research service to build their own Small-Cap Portfolio. What we do not advise are contributions followed by immediate buys to create an “instant portfolio.”

Why? We advocate creating an 8-12 stock portfolio with profitable, growing, and value priced small-cap stocks for the growth area of your portfolio. In this context, there are two major problems with investors who myopically focus on RRSP season.

Number one is that creating a portfolio at one set time immediately locks you into to that point in a market cycle. If it is near a top and a meaningful correction follows, it can take years to recover. Number two is that, quite frankly, it is difficult in most markets to find 10 great stocks to buy at any given time.

It’s all about quality over quantity and often investing success is as much about the stocks you don’t buy as it is about the ones you do. We encourage Canadians to consult with their financial advisors and make the appropriate contribution decisions this month. But remember that those funds do not all have to be deployed the day, week, or month after you make those contributions.

Be patient and create the small-cap growth area of your portfolio over one to three years and review and rebalance over that time. Given the fact that at 18.86 and 17.09 times earnings respectively, the S&P/TSX Composite Index and the S&P 500 are trading above historical P/E multiples, it is likely time to leave some powder dry to employ in the event of a pullback during 2013.

KeyStone’s Latest Reports Section

An interesting/funny/historical manner just how much tax you actually pay, once you factor in Direct Taxes, Indirect Taxes, excises, tarrifs, duties, business compliance costs, failed Green schemes, industry subsidies, carbon taxes, gas taxes, liquor taxes, provincial taxes, municipal taxes, property taxes, recycling taxes, CCP, Employment Insurance deductions, Government permits, fishing licenses………. and there is so much more -Ed

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair