Bonds & Interest Rates

Last night, six of us went out to dinner at one of the nicest restaurants in Salta. We ordered two bottles of good Laborum cabernet sauvignon. We had beefsteaks, dessert and coffee. The bill came to 1,058 Argentine pesos (about $200).

Was that a lot… or a little?

It depends. If you traded your money at the official rate, the meal would have been priced at around $200. Very reasonable.

But if you had traded your money at the rate quoted yesterday on the black market, the dinner would have been even more reasonable – barely more than $100.

This morning, the cab ride from the airport into Buenos Aires cost 50 pesos. At the official rate, that’s about $9. At the “blue” – or free-market – rate, the ride cost only $5.

The alert shopper can save a lot of money. The dull one gets ripped off.

All governments engage in larceny and fraud, using their authority to transfer wealth and power from the outsiders to the insiders. But the clever government does so by deception… while the clumsy one does so with no pretense or excuses.

In the US, for example, the feds deny savers any financial return from their economies under the pretense of “economic stimulus.” Wage earners get nothing, while bankers, speculators and zombie grifters are rewarded with ultra low-cost financing, capital gains, bailouts and giveaways.

The scale of this wealth transfer is the greatest in all history. Trillions of dollars are changing hands… But not one voter in 1,000 understands what is happening to him.

Writes Tyler Durden of Zero Hedge:

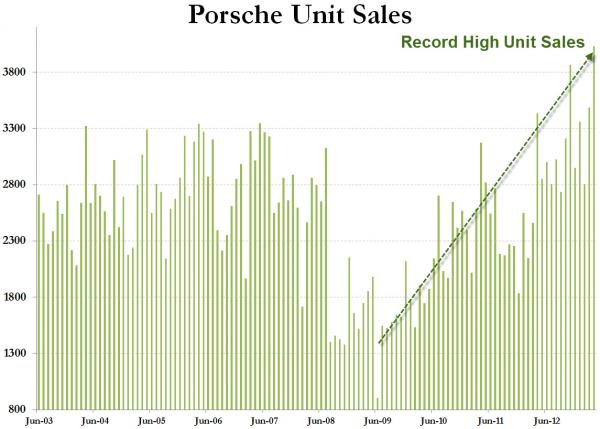

Curious where the always elusive “wealth effect” is going? It’s going here:

PORSCHE REPORTS BEST SALES MONTH IN HISTORY; DELIVERIES UP 29%

The typical American is not buying a Porsche. Relatively, he’s getting poorer. But his brain has gone soft, shrunken by TV news, elections and deadhead commentaries.

He believes Hillary Clinton when she says, “The government is all of us.” He thinks the Fed really is bringing a “recovery.” And he imagines that an economy can get richer when it prints more money and gives it to other people.

Sharpened by Adversity

Here on the pampas the Argentines know better. Their brains have been sharpened by adversity and enlarged by necessity.

“Every day, it is a struggle to keep up with it,” says a friend who runs a small business in Salta. “You have to figure out what the peso is worth… and you have to decide if you’ll do a deal in pesos or dollars. And if you do it in pesos, you have to figure out how to trade dollars for pesos… or vice versa.”

This week, the peso dropped to nearly 10 to the dollar. Officially, the rate is only 5.5 to the dollar. Big difference.

We need to buy a new hay baler. The price is quoted in dollars – about $50,000. You pay in pesos at the official rate… so that’s about 250,000 pesos. But wait – if you have dollars and can trade your money on the black market, you will save $25,000.

“The trouble is, the government is watching,” says our informant. “They’ll want to know where you got the 250,000 pesos… it can get very nasty if you don’t have your paperwork in order.

“But there are ways.”

The Argentines know they’re getting ripped off by the government. They find ways to protect themselves.

“There are invoices… and there are invoices. You can get an invoice at the official rate… or one at the unofficial rate. Or one that is not at any rate at all. The government rigs the system to cheat us. We rig it right back. You just have to make sure you have the right invoice for the right transaction. At the end of the year, people buy and sell invoices…

“I bought a new truck recently. But I made a bargain with the dealer. He delivered a new truck to me. But then he waited eight months to write up an invoice. By then, he was able to call it a used truck… and cut the invoiced price by half. It looked like I was paying full price for a used truck… I was actually paying full price for a new truck, but with money traded at the unofficial rate.

“Everybody’s got a trick or two. You have to. Otherwise, you’re a sap.”

The Argentines know they can’t trust their money… or their government. In comparison, Americans are saps. They don’t know whom to trust.

But we’ll make a prediction: Americans will be a lot less sappy… and a lot less wealthy… when they finally realize what the feds are doing to them.

Regards,

Bill

Bill Bonner started Diary of a Rogue Economist to share his over 30 years of economics and market experience with as many interested readers as possible.

Diary of a Rogue Economist is always free, and it’s delivered to your email each business day.

Like Bill’s Diary?

Republish our articles on your website or blog for free. Learn How

Have a question for our editorial team?

Contact Us

Want More?

You can also find us at:

Will the Breakout in the USD Index Hurt Gold?

We haven’t touched on currencies for quite some time (our latest essay was dedicated entirely to gold: Gold Price in May 2013) now but last time we did, we mentioned the long-term breakout in the USD Index, which at that time was starting to take shape, but as the time wore on it became more and more significant. This is why in today’s essay we’ll focus mostly on the U.S. currency, review its current technical situation and its implications for gold and silver. Let us then jump straight into the chart analysis – we’ll start with the very long-term chart where the breakout is most clearly visible (charts courtesy by http://stockcharts.com.)

The index has actually confirmed a breakout above the very long-term resistance line. It has closed above it now for three consecutive months (yes, months). While a correction to the 80 level is still possible in the short term, an eventual move to the upside is now more likely than not. The closest target level seems to be slightly above 85 and although the 90 level could be in the cards as well, for now, we will focus on the first target level at this time.

The situation in the United States has not improved dramatically and the value of the dollar will have to go down eventually because of the massive amounts thereof that were created in the recent months and years. However, please remember that the USD Index is a weighted average of currency exchange rates, so if other currencies depreciate faster relative to tangible assets such as gold, the USD Index could actually rally. Another possibility is if the US situation is bad but it is worse everywhere else, the index could also rally. Anyway, the above chart suggests the USD index will move higher in the weeks ahead, though not necessarily immediately.

Let us move on to the medium term now.

In this chart, the picture is not as clear. The bearish head-and-shoulders formation could still be completed here, but the index would need to move below 79 and then hold this breakdown. If it moves above 84, the bearish pattern would be invalidated. Since the long-term picture is more important and carries greater weight than the medium and short-term outlooks, it is more probable that a rally will be seen, although this may not happen right away.

Finally, let’s zoom in even further and see how the short-term situation looks like.

In the short-term USD Index chart, we see that the index declined immediately after the cyclical turning point. A sharp move lower has been seen over the past few days, though this did reverse on an intra-day basis on Thursday (perhaps forex traders acted on the bullish 3-month confirmation of the long-term breakout). This could in fact be a reversal, as moves to the upside appear possible now. It is, however, a bit unclear at this time. What should have happened due to the bearish impact of the cyclical turning point has probably already been seen. All-in-all, the situation is unclear for the short term.

In the long-term Euro Index chart, we see that the index bottomed within our target area and then moved higher. What’s ahead for the Euro Index is a bit unclear right now. An analogy to previous patterns suggests a move to the upside here.

With respect to gold, previous similar Euro Index trading patterns (such as in late 2010) coincided with gold moving lower initially and then rallying strongly (note the decline in late 2010 and early 2011). It seems that gold could once again move lower before rallying significantly.

Now, let’s take a look at the intermarket correlations to see how the situation in currencies may translate into the precious metals market.

The Correlation Matrix is a tool which we have developed to analyze the impact of the currency markets and the general stock market upon the precious metals sector, (namely: gold correlations and silver correlations). The short-term impact on the precious metals by other markets has been very unclear. On a medium-term basis, the impact from the currency markets is negative. The final bottom for gold, silver and the mining stocks may very well be ahead. In the long run, the effect of these other markets is close to zero, and we expect the secular bull market for precious metals to continue even though the rally may not be seen right away.

Summing up, the long-term outlook for the USD Index is now bullish, and this could damage the precious metals markets, at least temporarily. The very long-term correlations between the dollar and the precious metals have been pretty non-existent. A medium-term impact will likely be seen however if the USD Index rallies (expect “there was no bull market in gold, only the bear market in the dollar which just ended” and similar comments – look at the non-USD gold chart for proof that there was much more to gold’s rally than dollar’s decline). The metals will probably respond negatively at first, and then go along with their main secular trend, which is to the upside.

Thank you for reading. Have a great and profitable week!

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Trading & Silver Trading Website – SunshineProfits.com

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

“As in life, nothing in the markets seems to change in a hurry. But when an item finally changes, it tends to make up for lost time … What do they call it when you don’t trust anything? Oh yeah, they call it “Life in the markets under Ben Bernanke.” Will Ben continue to buy one trillion worth of bonds and assorted vehicles through the end of the year?

… Now the whole daffy world is following Bernanke’s lead. Japan has had it with two decades of deflation, and Japan’s new central bank head vows to double Japan’s monetary base within two years — or, at least buy bonds until deflation in the Land of the Rising Sun turns to inflation of at least 2%. In the meantime, Japanese stocks are surging under Japan’s new super brand of QE.

I have to wonder how long US stocks can continue to climb on the basis of quantitative easing? I don’t know, and I don’t think anybody else knows either. The strategy now seems to be — you buy blue chip US stocks or the DIAs and stay with them until the market turns sloppy — or until it actually turns down. Forget values, forget sentiment, forget risk, forget the charts, forget caution — stay with blue chip dividend-paying stocks for as long as they continue to climb, and when they halt their climb, give ’em back to Wall Street and await further developments.

But what about the “depression” that Nobel Prize winner Paul Krugman insists we’re now in? The hell with the depression, the stock market is going up, and maybe when it turns down we’ll have his depression. Until then, “What, me worry?” No chance, I’ve got my gold. And if the end of the world arrives, I’m betting gold will be my savior (that is, if Uncle Sam doesn’t take it away from me at gun-point).

Most professionals and fund managers are worried about a hurricane of inflation showing up somewhere in the not-too-distant future. After all, inflation is always a monetary phenomenon, and God knows we’ve had our turn at money creation. In fact, there’s never been anything like the current worldwide explosion of currency creation.

Then what’s stopping inflation? It’s the over-supply of commodities that’s been pouring into the West out of Asia. Too much copper, too much tin, too much zinc, too much in the way of merchandise, too much of almost everything. It’s a world avalanche of “too much,” and not enough demand. But central banks come to the rescue. They’ll print us out of deflation. And somewhere ahead, worry the money managers, the whole thing will catch fire, and we’ll end up with a sudden tidal wave of inflation. If so, then why isn’t gold at new highs? Patience, the markets always do what they’re supposed to — but never when.

The Fed is buying a trillion dollars worth of Treasuries and mortgage-backed securities so they’d drive the yield on 10-year Treasuries down to a ridiculous 1.67%. So where does the money go? Into blue chip stocks that are now the new safe havens. In the meantime, the US dollar gets whacked. Below we see the US dollar down heavily today and closing below its 50-day MA. Note that MACD is just turning down. (Ed Note: the next day’s rise in the USD was sharp, rising nearly 2/3 of a penny or .61)

But the S&P is at a new record high, and the TREND of the stock market is up, so I’m staying with the DIAs until I receive the first bearish signals … Summing up, the Bernanke Fed has succeeded in driving everybody into the stock market or back into real estate … It’s great to make money in the stock market, and your only worry is when the Federal Reserve’s punch bowl crashes … I still like gold, and as far as I’m concerned, it’s the only real safe haven.”

To subscribe to Richard Russell’s Dow Theory Letters CLICK HERE.

Useful articles:

“Rich Man, Poor Man (The Power of Compounding)“

Russell began publishing Dow Theory Letters in 1958, and he has been writing the Letters ever since (never once having skipped a Letter). Dow Theory Letters is the oldest service continuously written by one person in the business.

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

The Letters, published every three weeks, cover the US stock market, foreign markets, bonds, precious metals, commodities, economics –plus Russell’s widely-followed comments and observations and stock market philosophy.

In 1989 Russell took over Julian Snyder’s well-known advisory service, “International Moneyline”, a service which Mr. Synder ran from Switzerland. Then, in 1998 Russell took over the Zweig Forecast from famed market analyst, Martin Zweig. Russell has written articles and been quoted in such publications as Bloomberg magazine, Barron’s, Time, Newsweek, Money Magazine, the Wall Street Journal, the New York Times, Reuters, and others. Subscribers to Dow Theory Letters number over 12,000, hailing from all 50 states and dozens of overseas counties.

A native New Yorker (born in 1924) Russell has lived through depressions and booms, through good times and bad, through war and peace. He was educated at Rutgers and received his BA at NYU. Russell flew as a combat bombardier on B-25 Mitchell Bombers with the 12th Air Force during World War II.

One of the favorite features of the Letter is Russell’s daily Primary Trend Index (PTI), which is a proprietary index which has been included in the Letters since 1971. The PTI has been an amazingly accurate and useful guide to the trend of the market, and it often actually differs with Russell’s opinions. But Russell always defers to his PTI. Says Russell, “The PTI is a lot smarter than I am. It’s a great ego-deflator, as far as I’m concerned, and I’ve learned never to fight it.”

Letters are published and mailed every three weeks. We offer a TRIAL (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

IMPORTANT: As an added plus for subscribers, the latest Primary Trend Index (PTI)figure for the day will be posted on our web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

The JPMorgan Global Manufacturing PMI shows Global manufacturing growth slows to near-stagnation.

At 50.5 in April, the JPMorgan Global Manufacturing PMI™ – a composite index* produced by JPMorgan and Markit in association with ISM and IFPSM – signalled expansion for the fourth straight month. The rate of expansion decelerated slightly during April, meaning that growth so far in 2013 has remained, at best, only marginal.

Japan, South Korea, Indonesia and Vietnam were the only nations to report a faster rate of improvement in operating conditions during April. Europe remained the main drag on the global aggregate, with the euro area contracting at the sharpest pace in the year-to-date and the UK stagnating.

The US PMI fell sharply to signal the slowest growth for six months. There was further stagnation in neighbouring Canada, while Mexico expanded at the weakest pace in 20 months in Mexico. Growth of manufacturing also slowed to near-stagnation in China, Russia, India and Brazil.

Global PMI April vs. March

Every facet of global manufacturing is slowing and global growth will follow. A global recession is certainly baked in the cake, if indeed a recession is not already in progress.

Shock and Awe: ECB Prepared to “Cope With Consequences of Negative Deposit Rates”; Dancing in the Dark Experiment

….read it all HERE

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

Tming is everything in financial markets.— Among the many lessons to take from former New Jersey Governor and banker Jon Corzine’s fall from grace….or Consider your position when the music stops.

Tming is everything in financial markets.— Among the many lessons to take from former New Jersey Governor and banker Jon Corzine’s fall from grace….or Consider your position when the music stops.

If Corzine had merely delayed his forays into euro-zone markets, he might now be celebrated as a hero by shareholders of MF Global rather than hounded by their lawyers. That hypothetical helps put into perspective the profound shift in investor sentiment now sweeping through Europe.

MF Global’s bankruptcy in October 2011 was triggered by a panicked rout in Italian bonds, in which Corzine had concentrated most of a $6.3 billion bet he’d built up in euro-zone debt over the preceding year. Yet if he had placed that same bet a month later, MF Global’s Italy play may well have gone down as a truly savvy bet.

…..read more HERE

\

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair