Timing & trends

Soros Reports Over $239mm In Gold Positions, Buys $25mm In Call Options On Juniors

In a 13-F release issued by the SEC after market close yesterday, it was reported that Soros Fund Management LLC, founded and chaired by billionaire financier George Soros, significantly increased its gold related holdings, most notably, through the purchase of over $25 million dollars worth of call options on the GDXJ Junior Gold Miners index.

……read more HERE

Washington this week has been engulfed in the natural gas export conundrum, with a Senate energy committee’s first in a series of natural gas forums starting off on 14 May. They’re just testing the waters here, but next week we’ll get down and dirty on this one: the entire meeting will be devoted solely to the natural gas export question.

What we’re really waiting for here is the confirmation of Ernest Moniz as the new energy secretary. This will be the decisive moment, and the confirmation hearing is next week. While Moniz has remained tight-lipped on the issue, the general consensus among analysts is that the new secretary will support an expanded US natural gas export initiative. Things will become clearer next week … so stay with us.

On the crude oil side of this equation, the International Energy Agency (IEA) has also weighed in: The verdict: the US should stop dragging its feet and let the crude flow as US oil production continues its sharp ascent.

It’s a bit of a regulatory dilemma, since the 1979 Export Administration Act banned the sale of US crude abroad, with the exception of exports to Canada and Mexico. But it’s not 1979 anymore, and the shale boom has rendered these old restrictions unsuitable. If crude export restrictions aren’t addressed, the IEA says, the industry will find a way around them at any rate. The loopholes start with processed products that can no longer be considered “crude”.

The world of big energy acronyms had more in store for us this week, with the US Energy Information Administration’s (EIA) release of new data showing that developments in hydraulic fracturing and horizontal drilling have contributed to the rise in US oil output to 6.5 million barrels/day in 2012 from just under 5.7 million bbls/d in 2011.

Back to the IEA’s 2013 Medium-Term Oil Market Report … the agency is boosting its forecast for non-OPEC oil supply growth to 3.9 million barrels/day from 2012 to 2018, with the US accounting for 1.4 million bbl/d and Canada 1.3 million.

But we’re not just talking about quantity. The US oil boom is taking an unexpected turn towards quality, as well. The boom is actually boosting production of light, sweet crude and field condensate, not just heavier, sourer grades. Of course, this also means a bit of a headache for refineries that were putting all their eggs in the heavy crude basket.

And if you haven’t been following our coverage of the conflict in Syria, you should. This is all about petro-politics, the more so with the passage on Tuesday of a dubious Qatari-Saudi-sponsored resolution that will effectively rule out any dialogue with Assad.

In this week’s special report below we borrow from our premium publication and look at why Geothermal is starting to really heat up and a couple of stocks that investors should be keeping an eye on. More below…

I hope you find the below piece of analysis interesting and once again I urge you to take a look at our presentation on the value of energy intelligence over energy “information” and why there really is no comparison between the two when you have access to genuine on the ground intelligence – you can see the presentation here (again I urge you to read to the end to get a full understanding of the benefits.)

Have a great weekend.

Best regards,

James Stafford

Editor, Oilprice.com

I would say the answer is a resounding maybe!

I once said that John Percival, editor of the Currency Bulletin, has likely forgotten more about currency trading than most of us will ever know. I have been a reader of John’s newsletter for over 20-years. I have learned a great deal from him, through his writings. Here is an example of his insights which I took from a very beaten up copy of his book, The Way of the Dollar, published back in 1991.

In all markets, price extremes are usually attended by a consensus that the trend, be it up or down, will continue; and by a peak of speculation in line with the trend. Hence the excruciating paradox of financial markets, that sentiment is most bullish at the peaks when prices have only one way to go which is down; and most bearish at troughs vice versa: at the top there’s no one left to buy, and at the bottom no-one left to sell. This paradox is absolutely central to working of financial markets and we need all the help we can get to understand it so thoroughly that it becomes part of our nature. The more bullish things are, the more bearish they are.

Bullishness is born as hope in the midst of despair. Hope swells to confidence and confidence swells to euphoria, and the process contains the seed of its own destruction and the birth of the opposite, fear. Fear is nurtured by falling prices and the two feed on themselves until they swell to despair. And so the cycle is completed—and ready to begin again with the birth of hope. This is the way things are and the way they have to be. We haven’t understood the process until we have grasped that. The despair creates the price trough: the price trough creates the despair. The price extreme is the definition of the extreme of despair, which is in turn, by definition the moment when hope comes to prevail; hope feeds and is fed by rising prices until the peak of price and euphoria leave prices with only one way to go, which is down. This circular process underlies every price fluctuation in free markets from the smallest one measure in seconds or minutes to the largest measured in years or decades. So it has always been and so it will always be, because it must be.

Why am I sharing this? It’s the pre-requisite for my little quiz. Can you think of a currency now that seems to fit within John’s paradigm of a price extreme? If you said the Japanese yen, I would agree. Here’s why…

1. Every commentator worth his “gift of hindsight” now thinks the yen is toast into eternity. Keep in mind, eternity is a long time and there can be a lot of ebb and flow in between.

2.

I am not sure it is accurate to say that “everyone who wants to be short yen is already in the trade,” but I think we are darn close to some type of sentiment extreme based on open interest levels in the Japanese yen currency futures.

a.

Two points to consider in the Japanese yen futures chart below:

i. Remember how the EVERYONE told us that it was a virtual “layup” trade to go short the yen and use those funds to buy some other higher yielding vehicle, aka the yen carry trade? Well, those “gift of hindsight” commentators failed to see the global credit crisis dead ahead. Before this carry trade viciously unwound, we saw an all-time high in open interest levels in Japanese yen futures; that did indicate that everyone that wanted to be short really was short.

ii. Fast forward to today. Everyone seems to hate the yen. And though the open interest positioning is quite as extreme, it is the highest on record except for the carry trade unwinding period. So, it is fair to surmise we are near some type of extreme. Mr. Market loves extremes. Mr. Market loves one-way bets. Keep this in mind the next time Kyle Bass tells you it is “guaranteed” the yen will weaken more. He may be right. But during a trend it’s often difficult to separate luck and brains. That is not to suggest Mr. Bass isn’t brainy. Indeed he is. He tries hard to prove it, as he talks about such things as duration and convexity in Japanese government bonds. And if that doesn’t impress you, I don’t what would.

Is that it Jack? Is that all you got? Well, no. I have a little chart that I shared with the Members of my Black Swan Forex service today that indicates just maybe something called “yield differentials” are changing in favor of the yen. We can’t forecast interest rates, as Mr. Percival is fond of saying. And even if we could, we can’t be sure of the currency reaction. That being said, this correlation change in US versus Japan yield spread is interesting and should give all those yen bears something to think about:

Keep in mind the chart below is in $-yen terms (spot forex market); that is opposite to the chart above which is the futures market, which is in yen-$ terms…

US 10-yr – Japan 10-yr Yield Spread versus $-yen: This chart shows the yield differential is still positive for the US but now moving in the Japan’s favor. Also notice till recently the tight correlation between USD/JPY (yellow line) and this spread? Is it time for $-yen to catch up on the downside?

Is it time to buy Japanese yen futures or sell USD/JPY in the spot market? The short answer is a resounding maybe. I think we can say a few things with some confidence (but never with as much confidence as the “gift of hindsight currency analysts” that don’t really trade currencies for a living):

1) 2) 3) 4)

We are either at, or very close to, a sentiment extreme in the Japanese yen. The yield differential for the yen is improving based on the 10-year benchmark The Japanese economy is growing again and faster than expected Money is flowing into Japan to get access to Japanese stocks and growth

Given that set of variables, the probability of at least some multi-week change in trend could be in the making. And that’s all we can ask for. For in the end trading is simply a probability bet. Nothing more and nothing less…

Jack Crooks Black Swan Capital www.blackswantrading.com info@blackswantrading.com

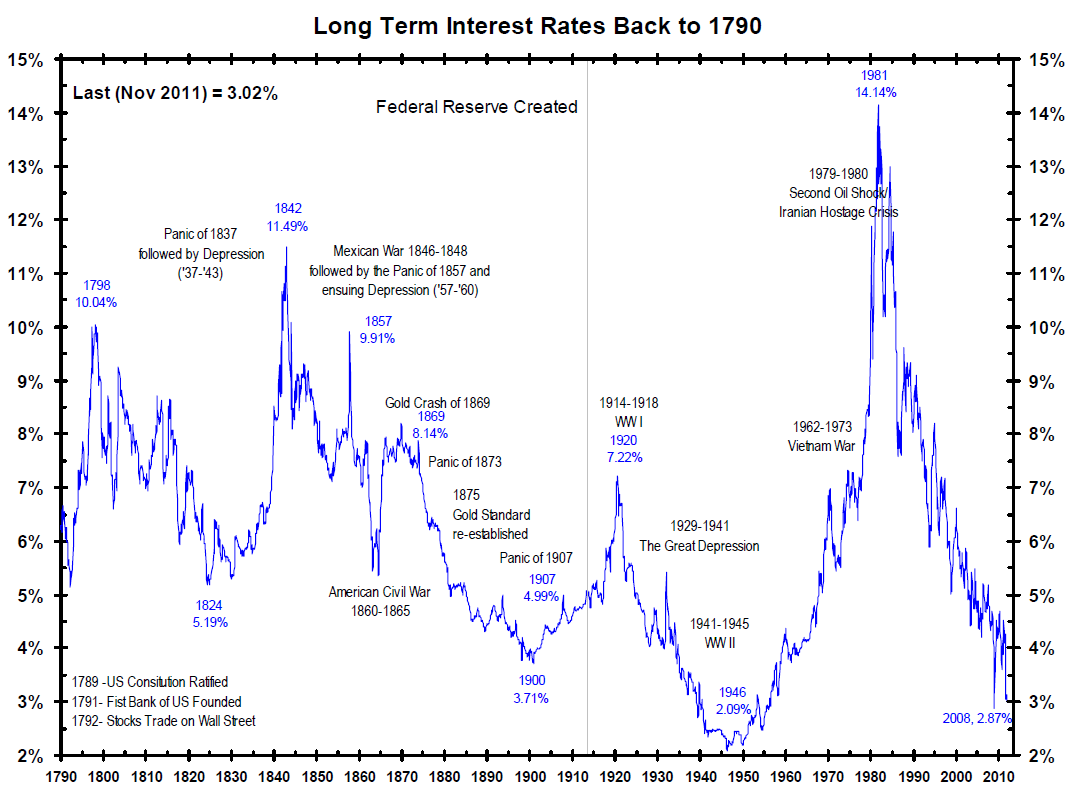

Bill Gross, who manages the world’s largest bond fund, has indicated that the 30+ year old super cycle bull market in bonds has ended. This is very bad news for the markets.

Bill Gross, who manages the world’s largest bond fund, has indicated that the 30+ year old super cycle bull market in bonds has ended. This is very bad news for the markets.

First and foremost, if bonds fall, rates will increase. With higher rates, it will be harder to meet debt obligations. This will be the case for corporations as well as sovereign nations.

For the former, this means that more money going towards paying off debt and less going to shareholders. For the latter, sovereigns, this means default. Most sovereign nations in the developed world are sporting Debt to GDP ratios above 100%. These levels are justmanageable with interest rates at record lows. When interest rates rise, default becomes a very real possibility.

In the case of the US, a 1% rise in interest rates means more than $100 billion more in interest payments. That money has to come from somewhere… which means either taxes going up, or the Government spending less on various programs.

For Europe, a 1% rise in rates can be almost deadly. Italy and Spain were both thought to be rock solid members of the EU. Once their ten year rates rose to 7%, they were suddenly on the verge of default.

And for Japan, if rates rise just a few percentage points, the entire system collapses.

For investors trying to navigate this market, it’s critical to note that the last bear market in bonds ended over 31 years ago.

This means that there is an entire generation of investment professionals and money managers who have never invested during a bear market in bonds. So many of these folks will be in a totally new environment.

Investors, take note… stocks are always the last to “get it.” This bubble will end as all bubbles do: in disaster.

If you are not already preparing for a potential market collapse, now is the time to be doing so.

I’ve been warning subscribers of my Private Wealth Advisory that we were heading for a dark period in the markets. I’ve outlined precisely how this will play out as well as which investments will profit from another bout of Deflation.

As I write this, all of them are SOARING.

Are you ready for another Collapse in the markets? Could your portfolio stomach another Crash? If not, take out a trial subscription to Private Wealth Advisory and start protecting your hard earned wealth today!

We produced 72 straight winning trades (and not a SINGLE LOSER) during the first round of the EU Crisis. We’re now preparing for more carnage in the markets… having just seen another SIX trade winning streak…

To join us…

Best Regards,

Graham Summers

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair