Gold & Precious Metals

Source: Special to The Gold Report from the Cambridge House World Resource Investment Conference (6/5/13)

Many investors are wondering if the words “gold” and “opportunity” can coexist in the same sentence. Michael Kosowan of Sprott Global Resource Investments answers with a resounding “yes.” He believes in the Pareto Principle—80% of the gain is derived from 20% of the stocks—and that contrarians will be rewarded in this “wonderfully miserable market.” To find that 20%, Kosowan outlines the criteria he uses when sizing up a junior mining company.

Watching gold prices these days has been an “exercise for the eyeballs,” similar to watching a rubber ball bounce around a concrete room. At times the price moves unnaturally, in fits and starts, according to broad economic policy statements in the marketplace and seemingly harmless comments right out of the Fed chairman’s office. How do we uncover opportunity amidst so much volatility in the marketplace?

Excellent gold stock opportunities are still available in this wonderfully miserable market. Gold stocks represent excellent opportunities to create wealth.

Most readers will fall into three categories: those who want to know how gold stocks and the word opportunity can coexist in the same sentence; those who have been swayed or afraid to invest in gold and are wondering what to do with their current portfolio; and those who recognize that they can be a contrarian or a victim in these markets and believe that there may be a turn in the market that can lead to wealth.

The history of this sector shows that there have been critical times to invest to produce life-changing wealth. Not surprisingly, this has typically coincided with times when public sentiment has been at all-time lows. At times like these the media tends to highlight the risk while ignoring the returns.

Today’s market is similar to a replay of a movie that we’ve all seen before. The low sentiment toward gold and gold stocks was also very prevalent in 1999, when I, Michael Kosowan, moved from the mining engineering side of the business to become a stock broker. At that time, like today, you were able to buy reality at a discount. The 1999 market gave rise to such success stories as Southwestern Resources Corp., International Uranium Corp. and AngloGold, all increasing tenfold or more.

Going back to the gold market in the 1970s, the price of gold moved up from $35/ounce ($35/oz) in 1970 to $200/oz by 1975. In the midst of that bull-run on gold, the price suffered a 50% retracement and moved back to $100/oz by August 1976—this was a cyclical retracement in a secular bull market. It was painful, but not debilitating to the bull market thesis.

During this tumultuous time the media had its own part to play. In August 1976, Time magazine proclaimed that “gold lately has had about as much luster as a rusty tin can.” Expectations were set very high on the initial run-up and the interim weakness was enough for the analysts of the time to discredit the entire gold thesis. Those swayed by the media were shaken out of that market and then missed the subsequent move from $100/oz in 1976 to $800/oz four years later. Time magazine was a very expensive subscription that year, to say the least. The investors who were swayed by the media missed astounding returns on gold as it moved through its bullish cycle.

So what do opportunities for gold look like now and how do I find them? A mine is a depleting asset; every day that goes by while it is in production reduces the size of the business.

The recent landslide at the Kennecott Utah Copper Bingham Canyon mine, located not too far from Salt Lake City, Utah, highlights this issue. This is the second biggest copper mine in the U.S. and one of the oldest—it started production in 1906. This mine as 107 years old and has been producing 200,000 tons of copper, 300,000 ounces gold, 3 million ounces (3 Moz) silver and 13,000 tons of molybdenum per year—truly massive!

Although it is very impressive to be pumping out this kind of tonnage at its age, Bingham Canyon is telling us legacy assets are becoming strained and long of tooth. They are dwindling, which spells supply disruptions, and therein lies the opportunity.

The costs associated with keeping mines in production are increasing and supply disruptions to such important assets are becoming more common place. The estimate for Bingham is that it may very well be off-line for the next two years.

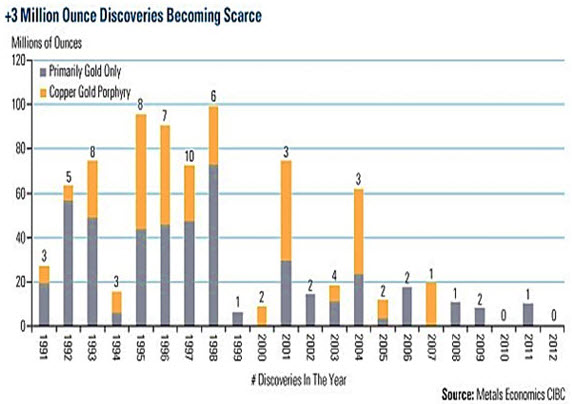

Our dwindling legacy mines are in urgent need of being replaced by new discoveries. So, where are they?

This chart depicts the 3+ Moz discoveries over the last 21 years.

The chart dramatically shows that this industry has seen an acute lack of significant discoveries in the recent past. Meanwhile, the industry is chugging through more than 80 Moz gold, 680 Moz silver, 15 million tonnes of copper and 90 million pounds of uranium annually. These depleted reserves need replenishment. And, in today’s challenging economic environment, the quality needs to be higher.

Discoveries made in the mid- to late 1990s are largely due to the increased financing activity that took place 10 years earlier. Funding comes 10 years ahead of discovery activity. The poor discovery rate of today is relative to the poor market conditions and lack of funding we suffered in early 2000s.

Since that time, funding has ramped up, notably between 2005 and 2007. If this cycle holds true—let’s call it the circadian rhythm of mining—then we may be directly in front of a renewed exploration and discovery cycle.

Here is a checklist for success with four factors:

The first factor is balance sheets. They can be intimidating for some investors, but they don’t need to be. Investors should look for whether the company has sufficient cash to cover its projected expenses for the next two years. Two years is important because finance continues to be tough in this market. If the capital raise is significant it will spell out heavy dilution and water down future positive price moves—if there are any. Small financings at these levels could be a warning of desperation as the company fights to cover incidental costs while adding no benefit to the exploration venture. These small raises could be going toward covering working capital deficits and salaries—basically keeping the lights on. Be wary of both large and small financings.

You don’t want a junior miner that has debt or high property payments in the near term. A company’s cash balance needs to be sufficient to take it to its next technical milestone. Companies add value by answering unanswered questions. How far will the company get to answering that critical question regarding its exploration program before needing to raise capital yet again?

The second factor is management. When it comes to junior mining stocks, management is key—and that can’t be stressed enough. Good management can make a lesser property viable. Make sure the people running the junior miner have a ton of experience, ideally directly related to the same commodity involved in the project at hand.

In an ideal world, management and/or the company’s geologists will have made significant discoveries in the past, bringing some of those deposits to production. Experienced management will also know how to navigate legal, political and financial issues and, especially important in many North American jurisdictions, the permitting process. Also, look for companies where the key people have plenty of “skin in the game,” ensuring their shares and stock options align their interests with those of shareholders.

The third factor is low capital costs. Capital cost is simply the total cost to put the mine into production. This is commonly found in the feasibility studies for the project.

The current challenging financial scene has made it difficult to access capital. This has been a barrier for the big, high-tonnage deposits. Recent high profile projects that have gone way over budget have poisoned the well of large-scale finance. While it was not that long ago that companies were being rewarded for big projects, this is not the case today and financiers are being far more selective.

The final factor is high margins. High grade equals high margin. And in this market, that’s crucial. The Holy Grail for many of the juniors is to be acquired by a senior. They must show that they have the high grade to offer or the takeover won’t happen. From my perspective the seniors have developed an inward-looking focus. They are attempting to develop low-grade ounces in a rising cost environment. Their older mines are getting deeper and more costly. This is known in the industry as “extend and pretend.” Production expansion is coming at a much higher price; at some point this will prove a losing battle. Going forward, high-return deposits will be key. The seniors have not spent money on exploration, leaving them with only one place to turn. . .the juniors.

These criteria form the “must haves” when choosing gold shares that will yield the best returns. Now more than ever they are crucial to the success of your investment. These criteria represent the tip of the iceberg. This is really just the beginning of your homework assignment in making your stock selection. Understand that the performance of this sector is really dependent on only a handful of stocks. The outstanding returns of the few derive benefit to the many.

The Pareto Principle is firmly at work here—80% of the gain is derived from 20% of the stocks. Finding that 20% is key.

There is real opportunity in this market to buy the all-stars of this industry at a discount. This is truly a wonderful set of circumstances for speculators—names like Ross Beaty, Bob Quartermain, Lukas Lundin, Robert Friedland—proven veterans of the mining sector who are now able to get their hands on some of the best projects they’ve ever seen.

Take advantage of this wonderfully miserable market we find ourselves in and find those fantastic opportunities that are out there.

This article was adapted from the talk Michael Kosowan gave at Cambridge House’s World Resource Investment Conference in Vancouver on May 27, 2013.

Michael Kosowan is an investment executive at Sprott Global Resource Investments Ltd. Prior to working for Global Resources, Kosowan was a project engineer at Placer Dome (now Barrick Gold) and the exploration manager for Atapa Minerals in Indonesia. Originally from Canada, Kosowan holds a master’s degree in mining engineering and is a licensed professional engineer. He is also a registered representative, having completed the Series 7, Series 24 and Series 63 in the U.S. and the Canadian Securities Commission course. He also holds a diploma in regulatory law. Kosowan will be speaking at the Agora Financial Tale of Two Americas Symposium in July.

DISCLOSURE:

1) Michael Kosowan: I was not paid by Streetwise Reports for this article. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the article for accuracy as of the date of the interview and am responsible for the content of the article.

2) Articles are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

3) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2013 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

For a while there it looked like Japan had the answer. A strong new leader comes in and cuts through all the indecision, orders the central bank to flood the system with cash to depreciate the currency now rather than later – and boom, the stock market soars, exports rise and the economy starts growing again.

The entire left-of-center world eyed this process hungrily, sensing both vindication of their views and the coming economic nirvana when their governments finally accepted the truth about debt (it doesn’t matter) and easy money (a free lunch that always creates wealth). If Japan’s success proved sustainable, within a matter of months the European Central Bank would have no choice but to join the money creation orgy. And with the euro and yen both falling like rocks, the US Fed would soon have to follow.

But Japan’s success, to put it mildly, didn’t turn out to be sustainable. Just as Austrian economists and common sense predicted, interest rates on Japanese bonds soared, as the global markets subtracted the 2% target inflation rate from the 1.5% or so yield on long bonds, and decided that a negative real interest rate probably wasn’t the best deal. They sold, bond prices plunged, yields rose, and Japan hit the wall that Kyle Bass and others have been predicting it would hit for, it seems, ever. Japan’s stock market, now unsure exactly what is going on, has sold off in huge, bloody chunks. (The following chart does not show today’s 518 point drop.)

Here in the US something similar is happening. Share prices are at record levels and real estate is booming, which is a recipe for instability, so the Fed has been making noises about easing back on the asset purchases. And the stock market, no surprise, has started doing what it always does when the Fed tries to siphon off the river of liquidity. It is tanking, down another 200 points on the Dow as this is written on June 5.

What does this mean? Well, the obituary of the supercycle credit bubble that began in the 1940s has been written so many times that it would be crazy to say anything that definite. But it is safe to say that the corner central banks have been painting themselves into has gotten a lot more cramped in the past few weeks. The global economy, led by Europe but with the US close behind, is slowing despite debt monetization that would have been labeled insanely inflationary by pretty much the entire economics profession two decades ago. But shifting the printing press into an even higher gear is very risky, based on the Japanese experience.

So our options appear to have narrowed to just two: Roll the dice on complete monetization in which the central bank buys up all the debt being issued — government, corporate, asset backed – and accept that an asset inflation might ensue (a global debt-for-equity swap, in other words). Or retrench, let interest rates rise to normal levels, and hope that that doesn’t send the leveraged speculating community (which includes the governments issuing and rolling over trillions of dollars of short term debt) into cardiac arrest.

Ed Note: Read Currency War Part 1 HERE

About

DollarCollapse.com is managed by John Rubino, co-author, with GoldMoney’s James Turk, of The Collapse of the Dollar and How to Profit From It (Doubleday, 2007), and author of Clean Money: Picking Winners in the Green-Tech Boom (Wiley, 2008), How to Profit from the Coming Real Estate Bust (Rodale, 2003) and Main Street, Not Wall Street (Morrow, 1998). After earning a Finance MBA from New York University, he spent the 1980s on Wall Street, as a Eurodollar trader, equity analyst and junk bond analyst. During the 1990s he was a featured columnist with TheStreet.com and a frequent contributor to Individual Investor, Online Investor, and Consumers Digest, among many other publications. He currently writes for CFA Magazine.

It all seems so surreal. After being mesmerized by the Fed’s hallucinogenic “Quantitative Easing,” (QE) drug, and seduced by the Fed’s Zero Interest Rate Policy (ZIRP), and rescued by the Fed’s clandestine intervention in the stock index futures market, for the past 4-½-years, it’s easy to forget that there was once a time when the Fed’s main policy tool was simply adjusting the federal funds rate. It’s even harder to recall that two decades ago, the Fed’s raison d’être was combating inflation, whereas today, the Fed’s main mission is rigging the stock market, and inflating the fortunes of the wealthiest 10% of Americans.

“The central bank’s purpose is to get ahead of the inflation curve,” declared Wayne Angell, one of the seven governors of the Federal Reserve on June 1st, 1993. Angell had a reputation as a Fed hawk, and he was pushing for a tighter monetary policy, even before an uptick in the inflation rate showed-up in the government’s statistics. “If we’re ahead of the curve, our credibility and the value of our money is maintained. Some of my economist friends tell me, ‘We don’t feel much inflation out there, but we feel better knowing that you’re worried about it.” Thus, there was a time when savers received a positive rate of return on their money.

Two decades ago, the Greenspan Fed was stacked with hawkish money men. And because their tenures lasted for 14-years, they felt immune to the winds of politics. Thus, if the Fed governors were to make unpopular decisions to hike interest rates, in order to bring inflation under control, or burst asset bubbles, so be it. Of course, it’s much different today – the Fed is stacked with addicted money printers that are beholden to the demands of their political masters at the Treasury and the White House. How did Fed policy swing so radically from Angell’s day – when Fed tightening meant lifting the federal funds rate and draining excess liquidity, to today’s markets, – where a small reduction in the size of the Fed’s massive QE injections is considered to be a tighter money policy?

The Treasury Bond Vigilantes, – is a nickname that was used to refer to a legendary band of renegade bond traders, who used to fire-off warning shots to Washington, by aggressively selling T-bonds in order to protest any monetary or fiscal policies they considered inflationary. The jargon refers to the bond market’s ability to serve as a brake on reckless government spending and borrowing. The last major sighting of the bond vigilantes was in Europe, as they wrecked havoc upon the debt markets of Greece, Ireland, Italy, Portugal, and Spain.

James Carville, a former political adviser to President Clinton famously remarked at the time that “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody,” he remarked. However, the so-called T-bond vigilantes appeared to be dead and buried over the past few years, as the US-Treasury was able to borrow trillions of dollars, largely financed by the Fed at the lowest interest rates in history. Keeping the T-bond vigilantes on ice, is a key linchpin of the Fed’s Ponzi scheme, that’s used to inflate the value of the US-stock market and keep it perched in the stratosphere.

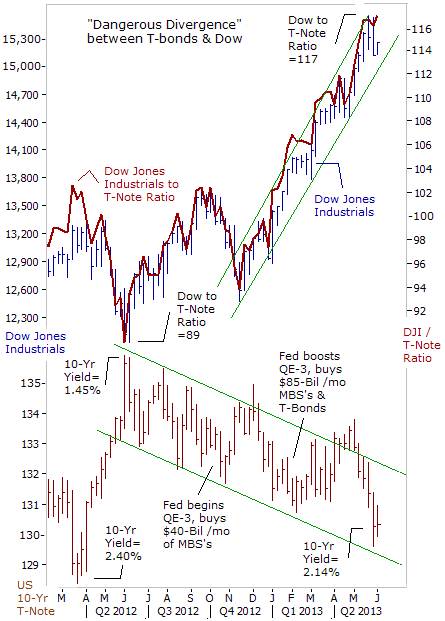

However, last month, (May ’13), something very strange began to happen. It looked as though the long dormant T-bond vigilantes were suddenly beginning to awaken from their slumber. Indeed, – the long-end of the US Treasury bond market suffered its worst monthly decline in 2-½-years, as yields jumped to their highest levels in 13-months. Ticker symbol TLT.N, – the iShares Barclays 20+ Year Treasury Bond fund lost -7% of its market value. It looked as though Wall Street’s bond dealers were whittling down their holdings of T-bonds, – acting upon insider information from the New York Fed, – that the biggest buyer in the T-bond market could soon reduce the size of its monthly purchases and thereby cause T-bond prices to fall. Interestingly enough, T-bond yields jumped +50-bps higher even though US-government apparatchiks said inflation was only +1% higher than a year ago.

During Greenspan’s tenure, the Fed would try to push T-bond yields higher, by lifting the overnight federal funds rate. But in today’s hallucinogenic world of QE, – near zero-percent short-term T-bill rates, and historically low bond yields, – if the Fed begins to reduce the monthly size of its T-bond purchases in the months ahead, – it could have the same effect as a quasi tightening. That’s because the Fed has so badly distorted and inflated market prices over the last few years. If the heavy hand of the Fed is gradually withdrawn from the marketplace, the big question is: what would it mean for the $21-trillion US-equity market?

The Bernanke Fed is coming under increasing criticism. On May 29th, the 85-year old icon of central banking, – the greatest warrior against inflation in US-history, – former Fed chief Paul Volcker waded into the debate over when the Fed should start unwinding its radical QE operation, arguing that the “benefits of bond-buying are limited and is like pushing on a string.” Volcker launched a scathing critique of the Bernanke Fed, inferring the central bank had become a serial bubble blower. “The Fed is effectively acting as the world’s largest financial inter-mediator. The risks of encouraging speculative distortions and the inflationary potential of the current approach plainly deserve attention,” he warned.

Volcker reminded the new breed of Fed lackeys that the central bank’s basic responsibility is to maintain a “stable currency,” and that it should unwind its reckless scheme of massively increasing the US-money supply and blowing bubbles in the stock market. “Credibility is an enormous asset. Once earned, it must not be frittered away by yielding to the notion that a little inflation right now is a good a thing, a good thing to release animal spirits and to pep up investment. The implicit assumption behind that siren call must be that the inflation rate can be manipulated to reach economic objectives. Up today, maybe a little more tomorrow and then pulled back on command. Good luck in that. All experience demonstrates that inflation, when fairly and deliberately started, is hard to control and reverse,” Volcker warned.

Last week, the Treasury’s 10-year yield climbed above the 2%-level, following Volcker’s remarks. The 85-year old Fed hawk still commands a lot of respect on Wall Street and his voice is not easy for the Fed’s rookies to tune out. The recent plunge in T-bond prices did trigger a knee-jerk sell-off in the stock market, that briefly knocked the Dow Industrials lower to the 15,100-level. But in a June 3rd note, Goldman Sachs (GS) released a message to the financial media, telling investors to remain calm amid the bond market sell-off. GS reiterated its Bullish stance on the US-stock market, – saying further gains lie ahead, and that S&P-500 companies have plenty of cash on hand, that can be deployed to offset the negative effect of higher interest rates, – by increase their dividends +11% this year and +10% in 2014. If correct, that would lift the S&P-500’s dividend yield to a meager 2.3-percent.

Still, yields on 10-year T-Notes increased by a half-percent in the month of May, including a jump of +16-bps on May 28th, – seen as a signal that the Fed’s would scale back its QE-injections. “A slowing in the pace of purchases could be viewed as applying less pressure to the gas pedal, rather than stepping on the brake,” said Kansas City Fed chief Esther George on June 4th. “It would importantly begin to lay the groundwork for a period when markets can prepare to function in a way that is far less dependent on central bank actions and allow them to resume their most essential roles of price discovery and resource allocation. I support slowing the pace of asset purchases as an appropriate next step for monetary policy. Waiting too long to prepare markets for more-normal policy settings carries no less risk than tightening too soon,” Ms George added. The Kansas City Fed chief cited signs of overheating markets, including margin loans at broker-dealers at a record $384-billion in April.

“We cannot live in fear that gee whiz the stock market is going to be unhappy that we are not giving them more monetary cocaine,” added Dallas Fed chief, Richard Fisher on June 4th. Still, many traders don’t believe that the Bernanke Fed could ever kick the QE-habit and act to tighten the money spigots. Since May ’12, traders have played the “Great Rotation” – shifting out of bonds and moving into stocks, seen as the best way to profit from the Fed’s radical schemes. However, there’s a good chance that going forward – the “Great Rotation” could morph into the “Dangerous Divergence.” If left unchecked, an extended slide in the T-bond market could trigger an upward spiral in the 10-year yield towards 3-percent, which in turn, would threaten to blow up the Fed’s Ponzi scheme.

Already, the ratio between the value of the Dow Industrials and 10-year T-note futures has reached the 116-level, – doubling from the 58-level – where it bottomed out in March ’09, and is within striking distance of its 2007 high. A last gasp rally in the US-stock market could be the catalyst that triggers a sharp sell-off in T-notes. At that point, the “Dangerous Divergence” could reach the breaking point, leaving the bond vigilantes to do their dirty work.

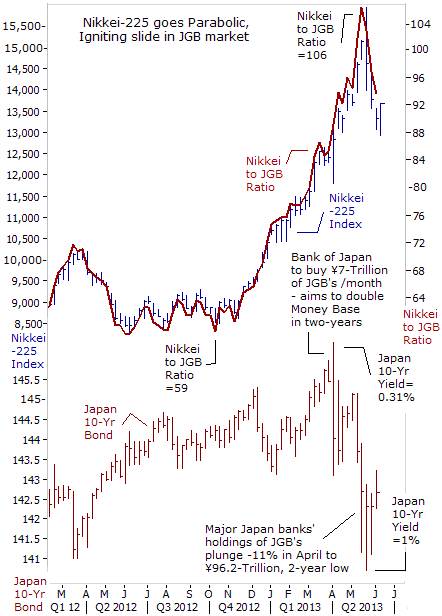

Minor Earthquake in Tokyo Bond market, – The recent sharp slide in US T-Notes was preceded by a tremor in the world’s second largest bond market in Tokyo. On April 4th, the Bank of Japan’s (BoJ) new governor, Haruhiko Kuroda, unveiled the most radical scheme ever, – designed to “shock and awe” Japanese bond traders into complete submission. The BoJ said it would double the amount of yen in circulation over the next two years, in order to whip-up inflation in the world’s third largest economy. The BoJ said it would trump the Fed, by printing ¥7-trillion each month, to be used to buy Japanese government bonds (JGB’s).

The BoJ was certain that it could continue to arm-wrestle Japanese banks and persuade its loyal citizens into buying 10-year JGB’s at yields of less than 1%, even as the BoJ says its aim is weaken the value of the Japanese yen, increase the costs of imports, and increase the consumer inflation rate to +2%. In other words, the BoJ expects investors to lock in negative yields for the next ten years. However, the gambit began to backfire, when yields on 10-year JGB’s rebounded from a historic low of 0.315% and surged to as high as 1% on May 23rd, – triggering a -7.3% crash in the Nikkei stock index. It was the Nikkei’s biggest one-day fall in 2-years, and kicked off an extended -17.5% slide to 13,050 by June 3rd.

It was later revealed on May 30th, that Japan’s biggest banks decided to slash their holdings of JGB’s to ¥96.3-Trillion, in the month of April, – a sign that their selling played a major role in pushing up yields to 1%. Japanese banks were unusually rebellious, and dumped 11% of their JGB’s holding onto the BoJ’s balance sheet, fearing a major rout in the future. For the BoJ, trying to force JGB yields lower, when its trying to weaken the value of the yen and whip-up inflation, – is like trying to submerge a helium balloon under water.

If this exodus from the JGB market continues, it could blow apart the BoJ’s Ponzi scheme. Japan’s outstanding debt is equivalent to 245% of its annual economic output, and 92% of the debt has been financed by domestic savings. But this may not continue. A government panel’s draft report has reportedly warned that there is “absolutely no guarantee” that domestic investors will keep financing government debt. The BoJ has calculated that a rise in JGB yields of just 1% would lead to market losses equivalent to 10% of the core capital for the top Japanese banks, and 20% losses for the smaller regional banks.

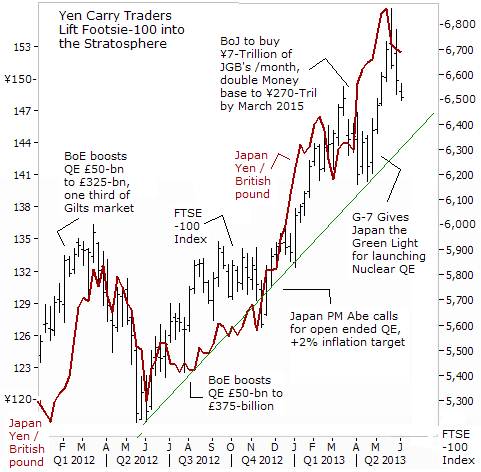

So far, the immediate impact of the BoJ’s Big-bang QE scheme has been a rapid and parabolic rise in Tokyo stock prices. These increases were fuelled by a frenzy of speculation by foreign traders. But rather than reflecting an economic recovery, the booming share markets are indicative of what the former-CEO of Citigroup, Chuck Prince, famously noted in July 2007, “As long as the music is playing, – you’ve got to get up and dance.” Nikkei Bulls are hopeful that the BoJ can keep the music playing, by boosting the size of its monthly JGB purchases if necessary. However, Tokyo cannot act in a vacuum – it would have to receive permission for an expanded QE scheme from its “Group-of-Seven” co-conspirators. And that’s unlikely.

“Stock markets are under the spell of QE,” In fact, both the BoJ and the Fed are in the crosshairs of the Bank for International Settlements (BIS), which warned on June 2nd, about the dangers of their ultra-cheap money policies that are driving up stock prices, despite worsening economic news. “Investors have ignored poor economic news as stocks have risen, leaving markets vulnerable to unsettling volatility and potential losses. Excessive monetary easing helped market participants to tune out signs of a global growth slowdown. But the rapid gains left equity valuations vulnerable to changes in sentiment, as witnessed in the recent bout of volatility in Japan,” the BIS warned.

“Yen Carry” Trade lifts London Stock Exchange, “With yields in core bond markets at record lows, investors turned to lower-rated European bonds, emerging market paper and corporate debt to obtain yield. Abundant liquidity and low volatility fostered an environment favoring risk-taking and yen carry trade activity,” the BIS noted. Whether by extraordinary good luck, or by clever design, the FTSE-100 index didn’t need the help of the Bank of England’s (BoE) money printing machine, in order to climb sharply higher to the 6,800-level this year. Instead, the Footsie hitched a ride to the rising tide of liquidity flowing from Tokyo, – via the “yen carry” trade. It was a smart move by the BoE to kick the QE-habit back in November. The maneuver provided a solid foundation for the British pound to rally strongly against the Japanese yen, thereby encouraging carry traders to borrow cheaply in yen, and plow the cash in high yielding Footsie blue chips.

In its report, the BIS went on to say that stock markets “are under the spell of monetary easing to the point where negative news such as downbeat economic data doesn’t stop stocks from going up. Every time an economic indicator disappointed, traders simply took that as confirmation that central banks would continue to provide stimulus,” such as near zero percent interest rates or QE schemes that increase the supply of money in the economy.

Such was the case on June 3rd – when the ISM’s index of US-factory activity fell to a reading of 49 in the month of May, down from 50.7 in April. That’s the lowest level in nearly four years and the reading under 50 indicates contraction. The unexpected drop in the headline figure reflected contractions in both the new orders index which fell to 48.8 in May from 52.3 in April, while the production index plunged to 48.6 from 53.5. Europe remains mired in recession and is buying fewer US-goods. In the first three months of this year, US- exports to Europe fell -8% compared with the same period a year ago. Despite the negative news, the Dow Jones Industrials soared to the 15,300-level, as traders reckoned the Fed would utilize it as an excuse to continue to print $85-billion per month of high octane liquidity.

BIS warns Bondholders – prepare for further losses, – However,Stephen Cecchetti, head of the BIS monetary and economic department, issued a warning to bankers and wealthy investors to prepare for an eventual normalization of interest rates that would cause additional losses for bond holders. “The losses, when they do occur, will be spread across banks, households and industrial firms.” He stressed it’s important that banks make sure their finances are strong enough before central banks end their QE programs and start raising interest rates. “Robust balance sheets with high capital buffers are the best ways to guard against the possible disruptions that this can bring,” he said.

On May 22nd, Bank of Korea Governor Kim Choong Soo also warned that when the Fed pullbacks from QE, it would spur risks worldwide from rising bond yields. “If the Fed begins to exit from quantitative easing policies, the world will be facing interest-rate risks, in terms of how much would bond yields rise,” he said. Also, IMF economists warned in May that a “potential sharp rise in long-term interest rates could prove difficult to control.”

Thus, while Goldman Sachs might be proven correct, and that another upward leg for the 51-month old Bull market still lies ahead, in the humble opinion of the Global Money Trends newsletter, it’s best to heed the advice of the legendary trader, Bernard Baruch, “I’ll give you the bottom 10% and the top 10% of any move, if I get to keep the middle 80%.” In other words, for “Buy-and-Hold” investors, it’s a better strategy is to take advantage of any possible rally in the US-stock market to lighten up on long positions, rather than to add any new long positions at the tail end of a bubble.

———————————————————————————

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Global Money Trends filters important news and information into (1) bullet-point, easy to understand reports, (2) featuring “Inter-Market Technical Analysis,” with lots of charts displaying the dynamic inter-relationships between foreign currencies, commodities, interest rates, and the stock markets from a dozen key countries around the world, (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, posted Monday and Wednesday evenings, with the latest news and analysis on global markets. To order a subscription to Global Money Trends, click on the hyperlink below,

http://www.sirchartsalot.com/newsletters.php

or call 561-391- 8008, to order, Sunday thru Thursday, 9-am to 9-pm EST, and on Friday 9-am to 5-pm.

This article may be re-printed on other internet sites for public viewing, with links to:

http://www.sirchartsalot.com/newsletters.php

Disclaimer: SirChartsAlot.com’s analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources. Copyright © 2005-2013 SirChartsAlot, Inc. All rights reserved.

LEASING is an integral part of the precious metals market, writes Miguel Perez-Santalla at BullionVault.

Why is it necessary? For a diverse number of reasons, the first is the need for industry to borrow instead of buying outright the metal. This enables them to avoid owning the metal at a fixed price if they have not yet contracted to sell their product.

Other companies want to borrow rather than buying gold or silver, to keep their cash consumption down. Leasing gives their business greater flexibility in money management. Still others choose to borrow to free up cash. Finally, there are those in a bridge lease, commonly used in the oil refining and pharmaceutical fields.

These companies already own all the precious metal that is needed, inside their pipeline. And as that platinum, palladium, gold or silver does its job, of cleaning out impurities from their end product (petroleum, drugs or other chemicals) it simply needs to be extracted from the waste byproduct and re-introduced to the process. But leasing gives the producer a little headroom while this goes on. They don’t need to own any more metal than they use, because it always comes back to them.

On the flip side there are financial, trading and metal refining companies who own gold, silver or platinum-group metals, or have metal on account, which they need to put to work. The metal which they have on account is held as a debt to their customers, rather than being physically allocated to the client. That is what enables them to turn their liability into an asset by putting it to good use, leasing gold out to earn them money.

The reason you want to know about precious metals leasing is to understand what this function represents, how it actually affects the market place, and its relationship to the price. This little exposé will in no way be exhaustive about all the different uses and functions of leasing. But it will serve as a primer for understanding a market product and service that seems to be a mystery for many commentators.

First, the pricing: Just as with anything you might pay to borrow, longer-term leases typically cost more – per annum – than short-term arrangements. See this table of indicative lease rates for instance.

Another very important point you should remember is that the ability to borrow gold or silver through leasing is not a simple process. In fact, most businesses involved have very stringent credit practices, and depending on the entity may entail quite lengthy processes and documentation at the front end before you can effectively become a user of this type of service. So moving forward, let’s assume for practical purposes that all parties to a transaction have met the highest credit standards.

We must also remember that the movement of valuables and precious metals is time consuming and expensive. Because of this, the marketplace created the ability to swap metals from one location – or from one period of time – with someone else that has it in another. Now, this is not something that is done for free. There is a charge which is determined by supply and demand for the specific location. Of course this is the kind of thing that can only be done if the two parties share the same interest. It is incumbent on anyone in the precious metals industry to establish trade relationships in the major markets that enable them to participate.

What does a swap have to do with leasing? If you are asking then I still have your interest! The reason is that location swap transactions happen to be a major part of the ability of institutions to lease or lend their metal to another party is because it increases the size of the available market.

So how does someone end up in the gold leasing business? For most, it’s because they have active business in the metal from the get go. In this case we can say a bank involved in precious metals, a trading company or precious metals refining business would have natural flow of business that would enable them to be in a position where they could offer leasing. In the first example we will call this primary entity Company A.

Company A has customers who hold metals on deposit. They’re not charged anything for this service, on the condition that Company A can use it in the meantime. Those clients have given their asset and accepted Company A’s good credit that they will deliver it back when needed. It is in reality no different that when you leave your money with a banking institution. The only difference is that the gold does not multiply through the banking system as money does. Because the sum total of physical metal does not change.

Let us make believe you are Company A and you have 10,000 ounces of gold deposited by your customers. Of those, you are able to lend out 8,000 ounces easily. But now you have an excess. So you calculate the earnings if you sell the gold outright in the market, and deposit or lend the cash to another borrower. To make sure you can give your clients the metal they’re owed, you also need to hedge yourself by buying gold back at a later date against a forward or gold futures contract (often referred to lately as paper gold) to avoid price risk.

In the current market environment, this could be profitable. Because the near term price is higher than the forward or future price (the market is in what’s called backwardation). You would pocket the premium for selling immediate gold, and buy the future delivery cheaper. Over that time period, you also lend the cash raised from the sale as well. It is a bonanza!

But it does not happen like this most of the time, and besides – Company A has multiple transactions and commitments in gold. So the picture I projected, though nice, is not always that simple

Let’s make believe the market is in full contango. This is the typical state of the gold and other precious metals markets. It means that the future or forward price is higher than the near term. So if you were Company A, then the spread would cost you money to hedge your position, and it would cost you more than you would earn, too.

What to do? You contact other people in the market place – outside your own circle of gold borrowing clients – and it happens that you can lend it to another party that has need for the gold in New York. He will pay you a premium, because he doesn’t have any there and needs to deliver to a manufacturer. But instead of just outright borrowing, he wants to give you gold in London – the most liquid physical gold market in the world – at the end of the term, which may be for 3 months. This sounds good. You can earn the premium for New York because he needs it there, and you have no price exposure. That is the simplest route from the point of view for company A.

Now let’s look at the different reasons to lease gold. Let’s take a jeweler. A jeweler needs to produce 10,000 gold rings for Macy’s (or whoever). But he does not want to buy the gold and take the price risk. Because the jewelry outlet does not want to price it until the goods are ready, especially if they expect the gold price to be lower.

The jeweler then borrows the gold from Company A and pays a percentage just like any loan for the term they are borrowing the metal based on the price of the day they borrow the gold. At the end of this lease they would then buy the gold from Company A at the same time they sell the metal to Macy’s.

Another possibility is the gold miner who needs to pay his employees and expenses. This company expects to have one thousand gold ounces from their recent production. The metal however will take 30 days to be available from the refiner, ready to sell in the market. So the miner leases the gold for one month from Company A, selling the gold for cash and paying its bills. They then deliver the refined gold to Company A at the end of that term.

There is also a manufacturer that uses precious metals as part of a catalyst. They already own what they need. But because the process to reclaim the metal from the catalyst is time consuming, and because they need a fresh catalyst immediately when they remove the old one, they need to lease some metal for that time period.

In leasing there are many other models and it can be used for other purposes, much like in the stock market. To sell short is one such use. It means to sell what you don’t have because you expect you will buy it back cheaper at a later date. But in the precious metals market, however, you don’t need to do that with physical metal if you have access to the futures market. Speculation using physical bullion – borrowed and then sold directly into the marketplace in the hope of buying back later at lower prices – just doesn’t make any commercial sense when the futures (aka paper gold) market enables you to do it much faster, without the need for long and involved credit checks like we saw earlier.

There you have the basics of precious metals and gold leasing. Just like anything in the world, what should always be simple is complicated by some to create some advantage in most cases. If you understand the basics you can work make your way through any other related concepts.

So what kind of effect can the leasing market have on pricing? It really all depends on liquidity. Unlike currency – where the Fed can come in and inject more money into the system – this is not possible in a truly finite market like precious metals. But thanks to the available supply above-ground, some precious metals markets are more susceptible to a liquidity crunch than others. For the next example I will use a true to life market occurrence.

In November 2006, I remember like it was yesterday, I walked into my office on a Monday morning and platinum was up $200. It had jumped from the $1200 level to over $1400 dollars. This was more than a 16% move from one day to the next. The chatter and market reports back then were that a bank trader was short a large amount of platinum, and was being forced to deliver on his short position on that Monday by other players who had got wind of his problems, and took the opportunity to profit from it.

Because his short position was so large, and because the platinum market is so small, his covering drove the price up. This happened because typically in the platinum market, much of the metal is out on leases. It would take some time to get all the metal back to make the delivery.

In this circumstance there were industrial users who knew their leases were coming due at that specific time period too. Because of this large short covering in platinum, the price shot up not just on the commodity but on the platinum lease rate as well. That day in fact, the industrial customer that was expecting to pay 3% to 4% for a 1-year lease was being offered at between 100% to 120% per annum! The consumer had no choice but either to return the platinum they’d leased, buy it outright, or accept the new rate.

In this instance, the best way to manage the situation was to lease day by day. As it worked out, the market calmed down and three days later the lease rates were essentially back to normal. But if the industrial consumer had decided to buy it at that elevated price level, he would have suffered a major – and unnecessary – rise to his costs. By the end of that week, the platinum price had also retreated.

Take note: the platinum market is far less liquid than gold or silver, meaning that there is less supply and demand. So its wild gyrations would not be probable in gold or silver markets. However, there is still a possibility of a similar circumstance. It’s just less likely that moves of that size would occur, because they are very much larger markets. And in the end it is not the lease rates that affect the market price, but immediate physical demand and price which affect the lease rates.

Leasing is a tool just like any other. It has its proper function, just like a knife for cooking, a rifle for hunting, or a gun for self-defense. That does not mean they are not misused, and often intentionally. But this does not negate their purpose and need in the market.

Some decry that the ability to lease metals enables the multiplication of the metal. However this is not true. It may multiply the commitments, but physical leasing is unlike money – which is multiplied by the ability of financial institutions to hold only a minimal part of the reserve as cash on hand.

With the precious metals market, in contrast, the commitments are for physical metal and delivery is always necessary at some point. Hence it is not a stroke of a pen, but the blood, sweat and tears of miners, refiners and logistics companies that produces or brings gold back into the market.

Yes, leasing might invite poor judgment on the part of a lender, or borrower. But the contrast that to the lack of metals industry failure with the repeated and increasingly common failure of financial and banking entities. Having to deliver rare, physical metals keeps errant trading to a minimum in a way which Fed-guaranteed bail outs of banking and financial brokerages does not.

Miguel Perez-Santalla

Miguel Perez-Santalla is vice president of business development for BullionVault, the physical gold and silver exchange founded a decade ago and now the world’s #1 provider of physical bullion ownership online. A fierce advocate for retail investors, and a regular speaker at industry and media events, Miguel has over 30 years’ experience in the precious metals business, previously working at the United States’ top coin dealerships, as well as international refining group Heraeus.

(c) BullionVault 2013

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair