Energy & Commodities

JPMorgan is exiting physical commodities trading, the bank said in a surprise statement on Friday, as Wall Street’s role in the trading of raw materials comes under unprecedented political and regulatory pressure.

JPMorgan is exiting physical commodities trading, the bank said in a surprise statement on Friday, as Wall Street’s role in the trading of raw materials comes under unprecedented political and regulatory pressure.

After spending billions of dollars and five years building the banking world’s biggest commodity desk, JPMorgan said it would pursue “strategic alternatives” for its trading assets that stretch from Baltimore to Johor, and a global team dealing in everything from African crude oil to Chilean copper.

……read more HERE

Capture upside in undervalued, underfollowed energy stocks

Capture upside in undervalued, underfollowed energy stocks

Big gains are rarely found by jumping on the bandwagon. Independent Analyst and founder of MockingJay Inc., Peter Epstein argues that market darlings won’t reward latecomers; that’s why he spends his time finding undervalued, underfollowed junior resource companies. In this interview with The Energy Report, Epstein shares his resource stock diamonds in the rough, including a uranium name commercializing a groundbreaking technology and a graphite company beating its competitors to market.

The Energy Report: You’ve written that “a great company doesn’t necessarily make a great investment.” Are you implying juniors are better bets?

Peter Epstein: Yes—juniors are highly risky in that they can move up or down by quite a large amount, but if, for example, a junior is trading at its cash value, how risky is it really? At some point the upside outweighs the risk. Make no mistake: You still need good projects, cash in the bank and a strong management team, but if you’re buying shares in a company that’s trading below its cash value, you’re basically getting its assets for free.

TER: What’s an example of a great company that’s not necessarily a great investment?

PE: Look at Cameco Corp. (CCO:TSX; CCJ:NYSE), a true leader in the uranium space and a great company. If underlying uranium prices rebound to $75 or $85 per pound ($85/lb), as many pundits expect, analyst price targets indicate that Cameco’s stock might increase by about 25%. However, select oversold juniors in the space could return multiples of the amount invested.

TER: Your portfolio really runs the gamut of resource sectors. How do you choose which commodities to focus on?

PE: I read a lot and I speak with many management teams and industry experts. It’s not necessarily difficult to pick the commodities that have strong core fundamentals. For example, iron ore fundamentals look challenging, as Rio Tinto (RIO:NYSE; RIO:LSE; RTPPF: OTCPK), BHP (BHP:NYSE; BHPLF:OTCPK), Vale (VALE:NYSE) and Fortescue Metals (FMG:ASX), together representing two-thirds of the iron ore industry, are ramping up production levels dramatically.

On the other hand, uranium fundamentals appear quite strong. Japan is restarting a number of nuclear reactors early next year and China and India are building new reactors as fast as they can. China has little choice. Its major cities are choked with coal-related air pollution, not to mention the millions of new cars on its roads. India’s coal market is hopelessly complicated and corrupt. Coal-fired electricity generation there can’t possibly keep up with demand. India’s stated goal is to get 25% of its power from nuclear energy, from which it currently gets just 3%. All of this suggests increasing demand for uranium.

TER: What are some oversold juniors you’re watching in the uranium space?

PE: Energy Fuels Inc. (EFR:TSX; EFRFF:OTCQX) is extremely well positioned in the U.S. It will have two of the top-five uranium development projects in the U.S. once it closes on its announced acquisition ofStrathmore Minerals Corp. (STM:TSX; STHJF:OTCQX).

Energy Fuels owns the only operating conventional uranium mill in the country. This mill has a replacement cost in the hundreds of millions, yet Energy Fuels’ fully diluted market cap is just $125 million ($125M). Energy Fuels trades at a very substantial discount to peer uranium producers. The last time there was a major bull market in uranium stocks, Energy Fuels’ stock was up by 400% within about nine months. This time around, the stars are aligning for big gains once again.

TER: How do you determine the top-five U.S. projects? Is it based solely on size?

PE: It’s largely based on the scale of the projects. The U.S. is home to a number of emerging in-situ recovery (ISR) projects that should produce 2–8 million pounds (2-8 Mlb) of resource over the next four to eight years. These are companies like Ur-Energy Inc. (URE:TSX; URG:NYSE.MKT), Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.MKT) and Uranium Energy Corp. (UEC:NYSE.MKT).

The difference with Energy Fuels is that its projects are conventional mining operations as opposed to ISR, which some believe is a lower-cost method. However, if you have a conventional mining project that’s three times as large as an ISR project, you’re still going to make strong returns at that scale, even if it’s at a lower margin. To be clear though, the economies of scale of Energy Fuels’ major projects could easily even out the margins as compared to proposed ISR projects.

TER: Black Range Minerals Ltd. (BLR:ASX) has an unusual uranium ore concentrating technology called ablation. How does that method measure up to an ISR or conventional mining project?

PE: The technology concentrates uranium mineralization at the mine site by 90% or more by separating waste from ore in a low-cost, green, purely mechanical process. Therefore, instead of shipping 100 tons of ore to a mill that could be hundreds of miles away, only 10 tons of concentrate need be shipped. This translates into immense savings at every step of the mining operation. Ore is cheaper to transport and process and there are 90% less tailings!

The unique thing about Black Range Minerals is that in addition to its Hansen/Taylor Ranch uranium project in Colorado, which, at 91 Mlb, makes Black Range a top-five resource holder in the U.S., the company also has a 50/50 joint venture (JV) with a private company named Ablation Technologies LLC. This JV has exclusive global rights to ablation technology, which could be a game-changer. The majors will be watching the deployment of a semi-commercial scale unit closely in coming months. This JV interest is a hidden asset that could be worth a multiple of Black Range’s entire market cap.

TER: You follow some potash stocks as well. Do you consider potash a way to play emerging economies? What are you projecting for that commodity?

PE: Potash has solid long-term fundamentals. Like uranium, it’s an essential commodity with few if any substitutes. It is a play on an emerging middle class in developing economies. But there’s a domestic angle as well: The U.S. imports 90% of the potash that it consumes. Passport Potash Inc. (PPI:TSX.V; PPRTF:OTCQX), located in Arizona, will be producing 2 million tons of potash per year, which could greatly help the U.S. reduce its dependency on foreign-sourced potash. Passport’s delivered costs will be untouchable west of the Mississippi, and Passport has easy access to both West Coast and Gulf of Mexico ports for exports to Asia.

Passport has one of the best potash projects in the world, yet the company’s market cap is a fraction of global junior peers, despite the fact that Passport released a preliminary economic assessment with a very robust, 27% after-tax internal rate of return. As Passport continues to derisk its project, its valuation could double or triple and still be just half that of junior potash peers like Karnalyte Resources Inc. (KRN:TSX) or Elemental Minerals Ltd. (ELM:TSX; ELM:ASX; EMINF:OTCPK). Passport is in active discussions with multiple strategic investors and offtake partners. Within the next six months, there’s a good chance that Passport will execute a strategic investment and/or offtake agreement, which will further derisk the story.

TER: Let’s move on to oil. The oil price is holding above $100 per barrel. Do you think that’s a sustainable price? What oil price do you use to evaluate an oil company’s worth or upside potential or downside risk?

PE: I never try to predict commodity prices. I just try to pick the companies with the best fundamentals. Commodity prices can rise and fall well beyond what known fundamentals would suggest. Who would’ve thought that oil prices would be up 19% year-to-date while silver is down 35%, gold down 23% and copper down 15%?

As for oil companies, I’m very excited about Zodiac Exploration Inc. (ZEX:TSX.V), which is an example of an oversold, underfollowed, misunderstood Venture Exchange-traded stock. It’s trading at $0.06 per share but it’s probably worth at least $0.20 per share. Zodiac has zero debt and $18M in cash, equal to about $0.05/share. The company controls 78,000 net acres of highly prospective oil properties in California. In late 2012, a private company named Aera Energy LLC executed a JV with Zodiac on about 20,000 acres of Zodiac’s holdings. Aera has committed to pay 100% of the cost of two vertical and two horizontal wells, which in total are expected to cost $50–60M, in order to earn a 50% interest in the 20,000 acres. This is a huge vote of confidence in Zodiac’s assets and implies a valuation for Zodiac that is far greater than what the market’s ascribing to it right now.

The icing on the cake is that Zodiac has tax pools that are conservatively worth $0.04 per share. Therefore, the per-share value of the company’s cash and tax pools are worth considerably more than the current stock price, and investors still get 78,000 highly prospective acres for free. The recent announcement that Western Energy Production LLC is pooling 10,000 acres with Zodiac is further evidence of increased activity and interest in Zodiac’s holdings. Majors in the region, including Exxon Mobil Corp. (XOM:NYSE), Royal Dutch Shell Plc (RDS.A:NYSE; RDS.B:NYSE), Chevron Corp. (CVX:NYSE) and Occidental Petroleum Corp. (OXY:NYSE) are well aware of Zodiac. Zodiac is in discussions with multiple parties regarding further development activities.

Pyramid Oil Co. (PDO:NYSE.MKT) is also located in California, which many people may not realize is one of the larger oil-producing states. Pyramid has $6M dollars in cash and no debt. It has fewer than 5M shares outstanding. This company is cash-flow positive and has been in existence for over 100 years—since 1909. The company is exploring multiple corporate initiatives right now to enhance shareholder value. Pyramid Oil is a well run, successful exploration and production play.

TER: You also follow the natural gas space. What companies are you keeping tabs on?

PE: CBM Asia Development Corp. (TCF:TSX.V) is a junior coalbed methane play in Indonesia. Some shareholders are suffering from investor fatigue, but the underlying fundamentals remain fantastic. CBM Asia is one of a few juniors surrounded by Exxon, Total (TOT:NYSE), BP Plc (BP:NYSE; BP:LSE), Chevron and others. Indonesia is perhaps the single best market for coalbed methane in the world. CBM’s land grab over the past several years could pay off big as soon as this year.

There’s a common perception that natural gas prices are low because in the U.S. and Canada they’re low, but in most places around the world, especially Europe and Asia, they’re actually two to four times higher. That makes CBM Asia a much more compelling play than a lot of domestic natural gas stocks. In Asia, prices are anywhere from $6–12 per thousand cubic feet ($6–12/Mcf) compared to the U.S., where they’re currently about $3.5/Mcf.

TER: There’s a lot of discussion about coal becoming less competitive as a U.S. fuel source compared to cheap domestic natural gas. In an article you wrote last December, you argued that the coal industry would probably never return to its 2011 highs. Has your outlook changed?

PE: Like it or not, coal will be with us for the next several decades. Some places around the world are increasing coal-fired electricity generation faster than other sources of energy. In the U.S., coal-fired power generation has fallen from about 50% of the total mix to about 40% over the past five years, largely due to low natural gas prices. But while coal use is in decline in the U.S., in China and India it’s still increasing at a fairly good clip. Coking coal is a bit different. It’s somewhat viewed as a necessarily evil because it’s used for making steel and there are few substitutes for coking coal in blast furnaces. But the amount of coking coal used globally is a small fraction of that of thermal coal that’s used to generate electricity.

TER: You cover Celsius Coal Ltd. (CLA:ASX), which has a coking coal project. What’s the story there?

PE: Celsius Coal is a junior that is in the right place at the right time with its Uzgen Basin coking coal project in the Kyrgyz Republic. Historical drilling shows the deposit hosts very high-quality coking coal, which is important because most coking coal around the world is lower quality and subject to greater price volatility. Because the project is located only a few hundred kilometers from the Chinese border, it has a captive regional market in western China.

Celsius will not be impacted by highly volatile seaborne coking coal prices. Its customers will benefit from stability, security of supply and reduced delivery times by choosing Celsius Coal versus other coking coal producers thousands of kilometers away. Celsius is lucky to have strong financial backing and a loyal shareholder base.

TER: Let’s conclude with your take on graphite. Last year was a rollercoaster ride for investors. What do you see as the demand drivers?

PE: It’s true that graphite has been a wild ride. The key to the story is that graphite prices have settled in well above historical levels. Demand drivers include the proliferation of electric vehicles. Tesla Motors, for example, uses batteries that contain up to 100 kilograms of graphite. Lithium-ion batteries will continue to be the main driver for graphite demand. Of course, Tesla’s current run rate of automobiles is not significant in a global context, but Tesla and many other electric car manufacturers popping up around the world will certainly move the needle in coming years.

TER: What companies are you following in that space?

PE: The lesson we learned last year is that the first few companies to get to market will enjoy strong pricing and strong demand. Dozens of graphite juniors are in the race, but less than half will finish. Big North Graphite Corp. (NRT:TSX.V) is not as big as its name suggests, but it should be cash-flow positive and selling graphite within six months. The company is aggressively pursuing an existing amorphous graphite region in Mexico. While better known, flake graphite plays could reach production within five years, Big North could be selling thousands of tons in Mexico and the U.S. next year. In fact, on July 19, Big North announced that it has already mined and stockpiled 190 tons. This is a highly speculative small-cap company, but one that could really take off once meaningful production begins.

TER: Do you have any final advice for investors in the energy space?

PE: Patience will be rewarded. While many global stock markets are at near-term highs, true contrarians should be happy to walk away from those markets and hold a basket of juniors. If one picks a diversified basket of well-positioned juniors, returns should dramatically outperform indexes like the S&P 500. It’s just a matter of time.

TER: Thank you for taking the time to speak with us today.

PE: Of course, thank you for having me.

In 2011, Peter Epstein, CFA, left his senior analyst position at a $3B hedge fund and formed MockingJay Inc., a consultancy for companies in the natural resources space and an informal investment advisor to high net worth investors, family offices and funds. Epstein’s areas of expertise include uranium, coal, potash, gold and oil & gas. He has published hundreds of articles on investment sites such as Seeking Alpha, The Motley Fool and Au-Wire.com.

“It’s difficult to be Mindful when you are immersed”

“It’s difficult to be Mindful when you are immersed”

Welcome to July 2013 edition of Views from the Crows Nest. Calgary summers are short, and so this edition will be, too.

Too much of almost anything is bad for us, including essential elements of a healthy lifestyle. Food, drink, sunshine, and exercise in moderation are excellent, but in excess they can be destructive.

The same holds true of information consumption. In respect of our investment portfolio, the mainstream financial industry would have us believe that more information is always better. The typical hooks that broader media use include: conflict (very polarized market opinions), celebrity (what the richest and famous Wall Street types are saying), fear of missing out on gains (greed), and fear of losing capital.

This is all designed to get the viewer addicted to the powerful narcotic of “sensationalist stimulation,” so they can charge more to the advertisers whose commercials you see – many of them disguised as interviews. It’s about the network’s and the advertisers’ profitability, not the viewers’ investment performance. Viewers are unwitting pawns in their chess game. To be frank, mainstream financial journalism is an elaborately designed, ego-based manipulation of human weakness. Yes, that’s how I really feel, and it feels good to say it so directly.

From my view up here in the Crowsnest, it’s painfully obvious that mainstream financial media offers exactly 0% of the Daily Recommended Allowance of the nutrients that lead to health, happiness and prosperity. In addition to lowering stress and enhancing numerous positive things in our lives, Mindfulness also happens to lead to better decision-making.

It’s difficult to be Mindful when you are immersed in the minutiae – whether it’s markets or anything else. Even the scientific community is starting to figure out what the great wisdom traditions have known for millennia. Click here for a TED talk on the subject:

As this is written, equity market participants are once again euphoric, fundamental valuations are stretched, and big picture technicals are flashing warning signs. Markets don’t care if you bought recently, only you do. So, if you are still invested in long positions, please be Mindful of the risk you are assuming if you choose to do nothing. Are you more concerned about “being right” about when and what you bought, or are you laser-focused on “getting it right” by managing your downside risk?

There is a time to buy, a time to sell, and a time to do nothing at all. My suggestion is that you mindfully consider your personal priorities again, take specific actions that are consistent with your priorities, then sit back and let things unfold while you enjoy the rest of our brief but unusual summer weather.

Patience and Discipline are accretive to your wealth, health and happiness; Fear and Greed are destructive.

Cheers,

Andrew H. Ruhland, CFP, CIM

President, Integrated Wealth Management

Portfolio Strategist, ETF Capital Management

The French government plans to pump billions more in aid desperately trying to save the Peugeot factory in Aulay. Hollande refuses to realize that raising taxes causes economic decline and a greater proportion of money goes to government. The Peugeot production facility is unprofitable and the operation is functioning more like a communist organization rather than an efficient productive entity. These people just cannot grasp the idea that their economic theories are simply antiquated and as unsustainable as Communism.

The French government plans to pump billions more in aid desperately trying to save the Peugeot factory in Aulay. Hollande refuses to realize that raising taxes causes economic decline and a greater proportion of money goes to government. The Peugeot production facility is unprofitable and the operation is functioning more like a communist organization rather than an efficient productive entity. These people just cannot grasp the idea that their economic theories are simply antiquated and as unsustainable as Communism.

…..read more HERE

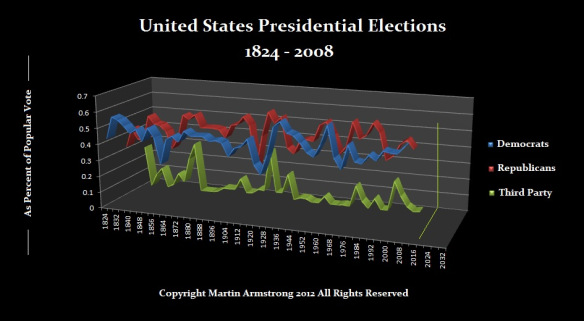

Throw the Bums Out

The Disapproval Rating of Congress has reached an all time high 83%. This is a historical high and is moving into what our computer has been forecasting that 2016 will be a rise in 3rd Party Activity. It is a shame, but politics has lost all touch with the people. The White House is actually arguing that the NSA needs to collect every phone call. This demonstrates that there is nobody left to defend the constitution.

Both Democrats & Republicans are fighting old theories that have proven to be complete disasters. Even in France, on July 18th, 2013 they passed the new Bail-In legislation and took the same position I stated the Fed was going around telling the banks that they willNOT cover losses in proprietary trading – only deposits and loans.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair