Gold & Precious Metals

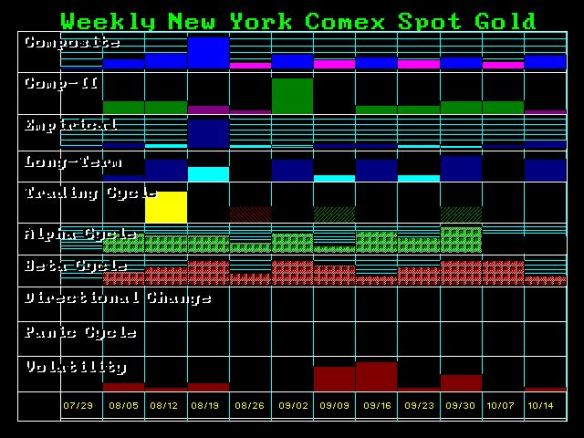

The diehard bulls are already proclaiming the low is in place so buy – buy – buy. Gold should press higher into next week, but the Weekly Bullish Reversal stands at 1423 and the year-end resistance will be 1435. The big turning point is still next January. So we are about $100 below major resistance. This diehard bullishness swearing every time this is it, is perhaps what has to break before we get the real bull market. Gold never got through the 1980 high adjusted for inflation $2300. It has been the worst performing asset with equity and, real estate advancing far more. The Dow stood at 1,000 in 1980 when gold was $875. The Dow has come close to 16,000 and gold could not break $2,000. It is all about time. You cannot have gold blasting up and everything else is not in line. But again, these people only look at gold and ignore the rest of the markets.

The time will be right. But patience is necessary. The problem with the Goldbugs is they are just always bullish and by constantly talking the same game no matter what, real unbiased investors get turned-off. This damages the credibility of the metals and makes a lot of people look at them as a joke rather than an asset class. It would be if a stock broker constantly said buy – buy – buy, even when the Dow declines.

It’s around 10:00 on a Friday night in early 2005. I’m shooting pool in a local bar with Hunter, a math professor at the local university who had just come into a big inheritance and was tossing it around like the found money that it was. He had recently paid cash for a house and taken his new girlfriend to Vietnam, and had (to get to the point of this post), after a few long talks with me, concluded that the housing bubble was about to burst and the banks and home builders were once-in-a-lifetime short candidates. He’d committed a fair chunk of change to put options on those companies in eager anticipation of their collapse.

But not only had the collapse not come but those stocks had risen, sending his options bets into freefall. On this night, he’d had enough. “Listen,” he said, “I can’t think about this anymore. Maybe it’ll happen, maybe it won’t but we’ve said everything there is to say, so let’s find something else to talk about.” We shifted focus to the game at hand, which also had money riding on it, and didn’t talk stocks for the rest of the night. Very discouraging. A friend had placed a big bet on my recommendation, had lost money and was pissed.

We didn’t know it at the time, but Hunter and I were experiencing something common among those who like to bet against bubbles: prediction fatigue, that (sometimes very long) stretch of purgatory that starts when you become certain that things are out of control and a crash is imminent – and runs until the crash actually takes place. Junk bonds, for instance, were clearly a bubble in 1988 but didn’t implode until late 1989. Tech stocks were classic short candidates in 1998 but doubled one more time before tanking in 2000. Housing stocks were garbage (along with most of the mortgages then being written) by 2004, but then they did this:

…..read more HERE

Stock Trader’s Almanac has been parsing equity market returns during the various years of the Presidential Cycle for decades; election years, pre- and post-election years, and mid-term years. The goal is to help equity investors to know when to expect highs and lows in the market based on what year of the cycle they happen to be interested in.

….see the chart & commentary HERE

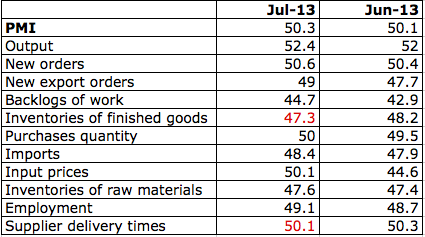

12-Month rise up 1.9% in July.

The Teranet–National Bank National Composite House Price Index™ rose to an all-time high in July, as did the indexes of four of the 11 metropolitan markets covered by the composite index: Hamilton, Toronto, Ottawa-Gatineau and Quebec City. However, the composite index was up only 1.9% from a year earlier. Though this was a slight acceleration from June, the 12-month gains of these two months were the smallest since November 2009.

By way of comparison, the Case-Shiller home price index of 20 U.S. metropolitan markets was up 12.1% from a year earlier in May (the latest available reading).

In Canada, the price rise over the 12 months ending in July exceeded the cross-country average in six of the 11 markets: Hamilton (6.7%), Calgary (5.9%), Quebec City (3.8%), Edmonton (3.5%), Toronto (3.4%) and Winnipeg (3.2%). It lagged the average in Halifax (1.5%), Montreal (1.1%) and Ottawa-Gatineau (0.9%).

Prices were down from a year earlier for a fifth straight month in Victoria (−4.0%) and for a 12th straight month in Vancouver (−2.0%).

…..read more HERE

Activist investor Victor Alboini has made a number of mistakes in his career. He has been on the wrong side of securities regulators and the investment industry’s regulatory body. But even his detractors on Bay Street should give the man some credit.

It was Mr. Alboini, the chief executive officer of Jaguar Financial Corp., who said in 2011 that BlackBerry Ltd. – then known as Research In Motion Ltd. – should put itself up for sale. He argued that the company would never shine brighter than when it was still promising to reinvent the smartphone, and that its prospects would likely fade once consumers and business users actually got to see its new devices. He was right. While the new BlackBerry 10 phones have received decent reviews in the specialized press, they have barely moved the needle for the Waterloo, Ont., company that bears its name.

Three busy open houses over Mother’s Day weekend and a steady stream of visitors with mid-week showings confirmed its popularity among buyers, four of which vied to produce the highest offer.

MORE RELATED TO THIS STORY

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair